Duty Drawbacks, Imported Inputs Duties and Exports: Evidence from Firm-Level Data from Colombia

Exenciones de tarifas aduaneras a los insumos importados y exportaciones: evidencia para Colombia según datos a nivel de firma

Reembolsos tarifários, tarifas sobre insumos importados e exportações: evidências de dados na empresa colombiana

Duty Drawbacks, Imported Inputs Duties and Exports: Evidence from Firm-Level Data from Colombia

Revista de Economía del Rosario, vol. 25, no. 2, 2022

Universidad del Rosario

Received: 04 august 2022

Accepted: 04 december 2022

Additional information

To cite this article: López-Valenzuela, D. C. (2022). Duty drawbacks, imported inputs duties and exports: evidence from firm-level data from Colombia. Revista de Economía del Rosario, 25(2), 1-59. https://doi.org/10.12804/revistas.urosario.edu.co/economia/a.12868

Abstract:

Using a generalized difference-in-differences approach, this study draws on a firmcountry-product-year level database covering imports and exports from Colombia to study how duty exemptions on imported goods affect export performance. The impact was estimated depending on the intensity exposure using the Colombian duty drawback policy —Plan Vallejo. Results suggest that input-duty reduction leads to rises in the export quantities and number of varieties, especially for products not benefited by the policy; however, the scheme allows firms to accentuate the negative impact of customs duty increases. The estimated tariff revenue leakage of the duty exemptions is non-negligible in terms of the country’s gdp.

jel classification: F10, F13, F14

Keywords: Duty drawbacks, imported inputs, exports, import duties.

Resumen:

Usando un modelo de diferencias en las diferencias y una base de exportaciones e importaciones a nivel de firma-país-producto-año, este trabajo estimó cómo el desempeño exportador colombiano se ha visto afectado por las exenciones de pagos de impuestos (arancel e iva) a los productos intermedios importados a través del Plan Vallejo. Los resultados indican que las reducciones de las tarifas a los insumos incrementan las cantidades y variedades exportadas, especialmente de aquellos no beneficiados por las exenciones, pero el esquema permite atenuar el impacto negativo de un aumento de tarifas aduaneras. El costo asociado a la política no es despreciable en términos del producto interno bruto (pib).

Clasificación jel: F10, F13, F14

Palabras clave: devoluciones de impuestos, insumos importados, exportaciones, tarifas a las importaciones.

Resumo:

Usando um modelo de diferenças em diferenças e uma base de exportação e importação no nível empresa-país-produto-ano, este artigo estima como o desempenho do exportador colombiano foi afetado por isenções de pagamentos de impostos (tarifa alfandegária e iva) para produtos intermediários importados por meio do Plano Vallejo. Os resultados indicam que as reduções nas tarifas de insumos aumentam as quantidades e variedades exportadas, especialmente aquelas que não se beneficiam das isenções, mas o esquema mitiga o impacto negativo de um aumento nas tarifas alfandegárias. O custo associado à política não é negligenciável em termos de pib.

Classificação jel: F10, F13, F14

Palavras-chave: reembolso de impostos, insumos importados, exportações, tarifas de importações.

Introduction

Industrial policies in developing countries have played a vital role in accelerating industrialization and development (Kaldor, 1960; McMillan & Rodrik, 2011). While some Asian countries have succeeded in this goal, in other countries —mainly from Latin America and Africa— resources such as labor have moved in the wrong direction: from more productive to less productive activities. Particular attention has been paid to the role of trade in this process. Countries whose governments have supported export activities and moved from traditional import substitution to more export-oriented and outward-looking policies have reached rapid and sustained economic growth. Thus, in these countries, trade plays a crucial role as a financing source and investment in infrastructure, the dissemination of information, and the accumulation of human capital by promoting better institutions (wto, 2003). In this context, giving exporters access to inputs at duty- and tax-free international prices may be effective in boosting manufactured exports. One method to do so is to have no tariffs or restrictions on imports, such as in Hong Kong and Singapore, but where import protection remains, the bias against exports needs to be reduced through schemes that lower import costs.

Historically, countries have put in place duty drawbacks (or rebates) schemes to permit exporters of manufactured goods to buy imported inputs at international prices in order to increase their profitability and competitiveness, without using direct export subsidies, prohibited by the World Trade Organization (wto) (Ianchovichina, 2004, 2005). The literature has paid little attention to the assessment of duty drawbacks schemes, contrary to other forms of public intervention such as subsidies and trade protection (tariffs and non-tariff measures). There is no consensus on whether countries should embrace these programs and, if adopted, whether they are effective. This paper aims to help close this gap.

Since 1959, the Colombian Government established a system for input duty exemptions applicable to exported goods (Melendez & Perry, 2010). This mechanism is called Plan Vallejo and is part of the Special Imports/Exports Programme (siep), which enables producers to ask for duty exemptions on imported inputs used in manufacturing exported goods. This duty exemption covers both tariffs and value added taxes (vat) —important cost sources for producers— which might alleviate plausible cash and credit constraints that some manufacturing firms may have to source before exporting their foreign inputs (Manova, 2008; Rajan & Zingales, 1998).

Evaluating these types of export-promotion policies is fundamental for several reasons. First, implementing duty drawbacks presents serious fiscal challenges to many developing countries where import duties, relatively easy to collect, often constitute an important source of Government revenue. Second, assessing the effectiveness and impact of the program on exporting firm performance is crucial to have an estimate of its benefits. This cost‐effectiveness analysis is a valuable input for policymakers to know if the policy works as expected. Third, as the duty drawback scheme is based on a special trade regime structure, it can be a source of rent-seeking and ineffective allocation of resources which might lead to welfare losses. Finally, since tariffs have substantially declined due to liberalization processes and preferential trade agreements, it is important to evaluate whether special imports/exports regimes are still worth the hassle. This study addresses some of these issues, contributing to the existing body of research.

Furthermore, this study contributes to current trade literature in important ways. First, by using a firm-product-country-year level database, the study provides direct and new empirical evidence about the duty drawback scheme in Colombia, a fact that, to my knowledge, has not been previously shown. Second, besides examining the impact of the policy on firms’ export outcomes, it also estimates the foregone program’s fiscal cost or tax revenue. Finally, the paper provides evidence of the impact of import duty rates on manufacturing exports through the intensive (quantities and prices) and extensive (number of varieties) margins and how this impact is shaped by firms’ experience. Therefore, the undertaken research also adds to the literature about the channel of intermediate goods on exporting firms’ performance.

Due to plausible endogeneity concerns as a result of reverse causality and omitted variables, the empirical strategy is based on two corrections. First, the estimates account for fixed effects at the firm-product and country-year level and control time-varying characteristics of the industry through sector-year dummies. Second, I exploit variations both in the import duties rates —which are tested to be exogenous to initial sectoral performance indicators— and in the intensity (exposure), using the duty drawback system at the firm-country-product-year level. This strategy is conceptually similar to a difference in differences estimate, where the treatment (duty exemptions) affects the treated group over time. The methodology also ensures that the control group is like the treated group by guaranteeing that for each beneficiary firm, there is at least one non-beneficiary firm exporting the same product to the same destination in the same year. The present paper takes advantage of disaggregated imports and exports data at the firm-product-country-year level over the period 2010-2019.

Overall, the findings suggest that 34 % of the value of Colombian manufacturing exports have been channeled through the siep over that period. Nonetheless, beneficiary firms constitute a small share of the total exporting firms, indicating the program is highly concentrated in a few companies. The administrative and economic costs associated with the compliance of several requirements, as well as the tariff reductions due to preferential trade agreements, have discouraged producers from importing and exporting through this special regime. Results suggest that the scheme works as an effective mechanism to smooth the impact of changes in imported input duties. Hence, in times when customs taxes increase, the benefited exports are shielded from the negative effect of tariff or vat raises, bringing gains in terms of exported quantities and varieties for treated observations relative to the control group. However, if an input-duty cut takes place, the marginal and positive impact that these reductions might have on boosting exports is lower for exports benefiting from the program. Besides, the impact of the siep on export outcomes increases as firm experience rises and is driven mainly by exports to low and middle-income destinations. Finally, the results allow concluding the revenue forgone from duty exemptions of the siep represents 1.73 % of the gdp, which seems to be high in comparison with other tax revenues collected by the Government.

The paper’s organization is as follows. The first section presents a short review of the literature about duty drawbacks and duty exemption policies worldwide. The second and third sections intend to describe some stylized facts about the siep scheme in Colombia and the data used. The fourth section shows the procedures carried out to choose the firms and the observations to be considered in the empirical strategy, presented in the fifth section. This is followed by the results, along with some robustness tests and estimates of the fiscal cost of the program. Lastly, it presents some conclusions and final considerations.

1. Duty Drawbacks Schemes and Duty Exemption/Deductions

Nowadays, many governments pursue export promotion policies to support economic growth in their countries. Export promotion’s vast array of policy options includes public good provisions, exchange rate policies, financial and credit assistance, and non-financial services, such as marketing and advertising services. Besides, these export promotion measures have also included duty drawbacks and duty exemptions (or deductions) on imported goods.

Export performance can be delayed not only by existing barriers in the country of destination but because of a country’s own pattern of import protection; its tariff structure that acts as a tax on its export sector may also frustrate its goal of increasing export profits (Costinot & Werning, 2019; Lerner, 1936; Tokarick, 2006). There are several channels through which tariffs act as a tax on exports. They create a disincentive to export by directly reducing the cost of exports relative to imports and altering indirectly the price of exports relative to the rates of nontraded or home goods —relative prices channel— (Clements & Sjaastad, 1984). Additionally, tariffs and other import barriers discourage exports by raising the price of imported and domestic intermediate inputs used by exporters —the cost of inputs channel.

Henceforth, tariffs on inputs act like a tax on exports, thereby damaging the competitiveness of the export sector in world markets. To compensate for this anti-export bias, drawbacks schemes are one of the instruments mostly used to enable exporting firms to recover duties paid on imported inputs utilized in export production while maintaining the protection of the rest of the economy. However, duty drawbacks often do not remove the bias against exports completely since they are costly to administer, reduce the government’s revenue, which would lead to the increase of other distorting taxes that might discourage exports, and do not reverse the impact of tariffs on relative prices (Tokarick, 2006).

Duty drawback schemes involve a combination of duty rebates (ex-post of exporting) and exemptions (ex-ante of exporting) and depend on each country’s trade regime. In the Latin American region, as shown by Melo (2001), these export-promoting policies have been widely put in place. Sixteen out of the twenty-six countries analyzed have some type of drawback scheme, and some of them, like Colombia and Mexico, have gone beyond the traditional reimbursement mechanism to an exemption scheme where, instead of refunding duties ex-post, an outright exemption allows exporters to avoid paying duties in the first place. For the present study, the term duty drawbacks (ex-post) and duty exemptions (ex-ante) will be used interchangeably.

Despite the administration difficulty of an exemption system (ex-ante) and its requirements for a well-developed and efficient customs administration, it is more attractive to exporters than drawbacks (ex-post) because no resources are used for paying import duties, and there are no refund problems. Uncertainty about repayments acts as a disincentive to exporters, leading them to factor the delays and uncertainties into their cost and price calculations (Corfmat & Goorman, 2003). Another disadvantage for manufacturers is that the firm must pay the duties and taxes and often wait a considerable period before the refund is made, thereby reducing the company’s working capital. However, the exemption approach (ex-ante) could be less practical for small producers since it may represent higher costs due to the administrative burden and paperwork compliance with the customs authority.

While duty drawback schemes are quite diffused worldwide, empirical analyses about users’ evaluation and their effects are few. Nevertheless, the descriptive literature on countries’ experience with tariff reforms, duty drawbacks, and export processing zones (epzs) has been growing rapidly in recent years. Herander (1986) was one of the first authors who studied the implications of duty drawbacks, but he emphasized its impact on the structure of protection. He found that although duty drawbacks achieve their export expansion goal, it is obtained at the expense of either domestic component producers —whose protection is reduced— or domestic consumers of the final good, who pay a higher price. Later on, in a major study of trade reforms in developing countries carried out by the World Bank, Thomas et al. (1990) made a strong case in favor of duty drawbacks and duty exemption as instruments of export promotion.

Panagariya’s (1992) study was the first paper to introduce a theoretical model to study the welfare implications of trade reform in a small and open economy with duty drawbacks. His main message was that, in a regime that protects final importable increases in tariffs on intermediate inputs complemented by duty, drawbacks on exports improve welfare up to a point. The latter will depend on whether the final import and the export good using the input are substitutes in consumption and production and on the distortions in the economy.

More recently, the literature has relied on general and computable equilibrium models to analyze the welfare impacts of duty drawbacks reforms in the presence of domestic distortions (Fan & Li, 2000; Ianchovichina, 2004, 2005) and its impact on exporter incentives to lobby against protection on imported intermediate goods (Cadot et al., 2001). Authors using the Common Market of the Southern Cone (Mercosur) as a case study and an agency model of endogenous protection with intermediate goods —where duty-drawback schemes are jointly determined with tariffs— show that under a full duty-drawback regime, tariffs on intermediates are irrelevant to exporters. The above is due to the fact that they are fully rebated and reduce exporter incentives to lobby against protection on imported intermediate goods, which can lead to higher tariff rates on them and penalizing users of such goods that do not-export.

The work undertaken by Ianchovichina (2004, 2005) evaluates the importance of duty exemptions by assessing the impact of China’s wto accession on the country’s output, trade, and welfare. As a result, it states that import concessions (such as duty exemptions) that override existing protection play a remarkable role and have been an important element of the gradual trade liberalization process that has boosted growth in China. Furthermore, her research shows that the trade orientation of the firms will imply differentiated effects of any policy reform done by the Government.

On the other hand, acknowledging the importance of duty drawbacks for the export processing system in developing countries, mainly in Asia, the topic of concessional import arrangements has been considered in various papers (Aggarwal, 2004, 2005; Chandra & Long, 2013; Gourdon et al., 2019; Lemoine & Ünal-Kesenci, 2004; Madani, 1999). They conclude that duty exemptions/rebates have had positive effects because they improve competitiveness, technological upgrading, export diversification, and firms’ efficiency, thus, boosting trade growth.

In addition to duty drawbacks and duty exemption schemes on imported goods, the export processing zones (epzs) have also provided various incentives for both the processing of raw materials for export and the assembly of imported parts and components to produce finished goods for export. The epzs are an arrangement whereby exporting firms locate their manufacturing plants inside an in-bond, common physical space and receive a set of fiscal incentives in exchange for the commitment to produce, transform, or both goods for the external market (Engman et al., 2007; Melo, 2001). Gruen (1999) illustrates the similarities and differences between traditional and the socalled new trade liberalization instruments such as epzs and duty drawback schemes and concludes that both can bring about a flexible liberalization path and speed up the opening of protected economies.

Since the beginning of the 1990s, epzs have been one of the most used strategies to increase exports in Latin American and Asian countries. epzs have proliferated in the last two decades by providing benefits and exemptions to local-producing domestic and foreign firms. This scheme provides duty-free imports as duty drawback (exemption), system and additional fiscal incentives, preferential land use, investment facilitation and protection, trade facilitation, and other broader set of objectives and rules (Frick et al., 2019; Lu et al., 2019). All these tools to attract investments would make epzs even more advantageous for export-oriented firms than the traditional drawback. Although the aim of the study is not to detail epzs, it is important to stress that processing firms located in these special economic zones can be an extension of duty drawbacks and duty exemption regimes.

In many countries, duty drawbacks have not been implemented successfully due to administrative weaknesses. It is a relatively high-transaction cost system; hence, in practice, it is mostly used by large firms in sectors that are intensive in either imported capital goods or intermediate inputs (Ianchovichina, 2005; Melendez & Perry, 2010). Experience shows that several countries have had great difficulty in administering and monitoring these regimes, which has resulted in abuse, fraud, and significant revenue leakage. Where customs controls are weak, revenue may be lost if exempt materials are used in the production of goods sold in the local market, thus, evading the duties and taxes due (Corfmat & Goorman, 2003). If the system is largely abused, the tax revenue loss may be significant.

Nevertheless, in other countries, such as China and Korea, these schemes have been very effective in opening export-oriented sectors by overriding existing protection. Due to this, a large part of the literature has paid special attention to these economies (Chao et al., 2001; Mah, 2007a, 2007b), overlooking other middle-income countries’ experiences. Asian countries are characterized by very specific features that make them successful case studies. Besides the Government’s agenda, which entails exports as a crucial factor in the economic growth strategy, the endowment of resources (cheap labor cost, availability of capital, etc.) gives them an outstanding economic advantage. Unlike Chinese or Korean contexts, the experience of Colombian export-promoting policies might be more easily applied and replicated in other Latin American and African countries with similar socio-economic and political contexts. Another fundamental difference lies in the stringent constrain applied to Chinese firms. While Chinese processing firms that benefit from duty-free trade are not allowed to sell their products within China, in Colombia, the regime allows manufacturers to export only occasionally or a small part of their production.

2. Description of the siep and its Relevance on Colombian Trade Flows

Since 1959, the Colombian government established a system for input duty exemptions applicable to all export sectors (Melendez & Perry, 2010).1 This mechanism is called Plan Vallejo and is part of the siep, which enables producer firms to ask for duty exemptions on imported inputs used for manufacturing exported goods. This system was initially set up to mitigate the anti-export bias of tariffs by ensuring tariffs were not paid on intermediate inputs used in the production of exported goods, thus, improving the country’s export competitiveness. Like any export subsidy, the drawback (or exemption) creates an incentive to sell abroad rather than at home. However, it differs because it is in compliance with wto rules since it provides for a refund of duties and import charges levied on the imported inputs used in the production of exported merchandise.

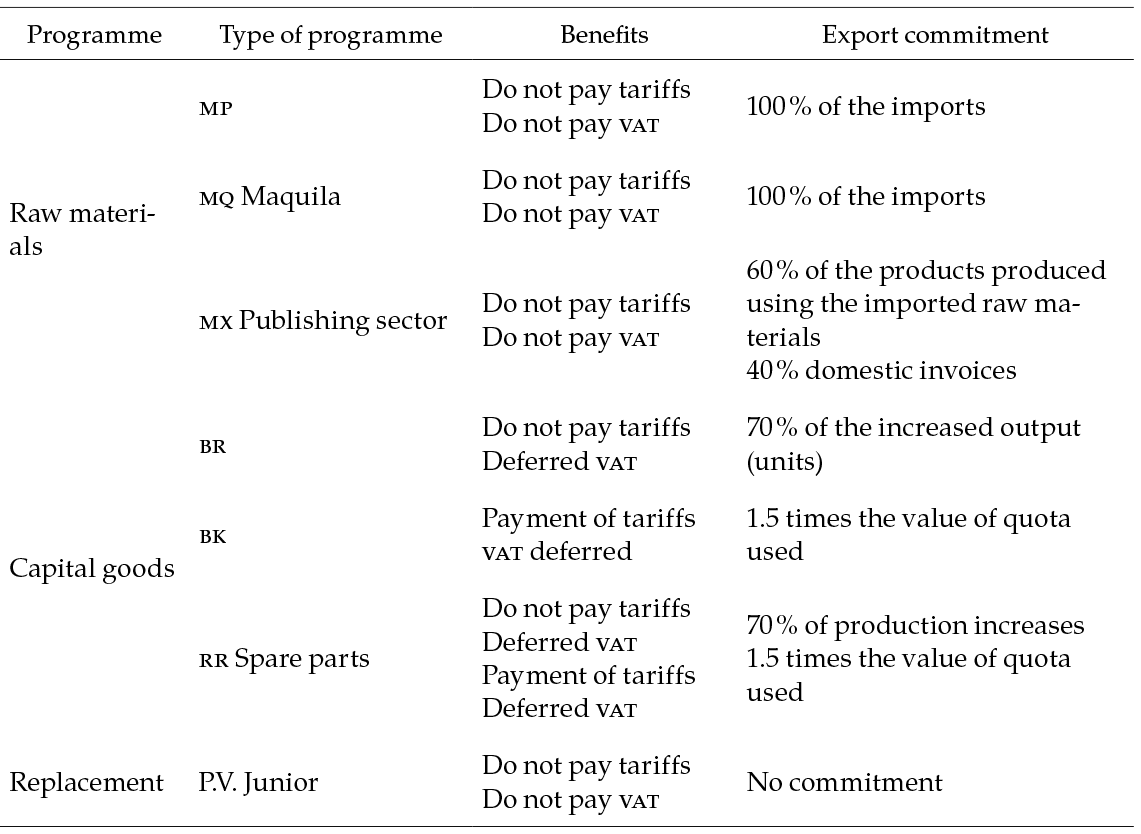

The siep covers imports of inputs, raw materials, intermediate goods, capital goods, and spare parts used in the production of goods for export or for the provision of services directly linked to the production or export of such goods or for the export of services. Currently, the siep in Colombia eliminates the taxes paid on imported intermediate goods or raw materials used in the production of exports, encompassing both tariffs and vat paid. Intermediate goods and inputs are completely free of tariffs and vat charges, while the imports of some capital goods and spare parts are only exempt from tariff duties, whereas vat payments can be deferred (see Appendix A for further details).

Access is available to importers of raw materials or intermediate goods, who produce and export the end product, importers and producers of intermediate products sold to an exporter, and providers of services linked with the production of goods for export (wto, 2018). Besides, to be eligible, firms must meet various administrative requirements and control procedures with the customs authority and the Ministry of Commerce. These include general (application form, certificate of existence and legal representation, and financial statements as of December of the year immediately preceding the application) and specific requirements (operating contract, leasing contract in the case of capital goods, an input-output table containing detailed information about imported inputs and their technical characteristics, as well as about the production processes, waste and final destination of them, export units produced, etc.). It is also a requirement to have a clean record with the competent authority without any violation or sanction regarding the special import and export systems. The products manufactured using raw materials and inputs imported under the siep must be exported, and the prove of the export must be shown (see Appendix A) within eighteen months from the clearance authorization date of the first customs declaration. In the case of the agricultural sector, the time limit may be 24 or 36 months (wto, 2018).

For the period 2011-2019, the cif value of goods imported under the siep scheme totaled usd 30 226 million (m), oscillating annually between usd 2000 m (in 2016) and usd 4200 m (in 2014), with a decreasing trend in recent years (Figure 1a). During the last decade, these imports, mostly totally exempt from customs payments, have represented, on average, 6.2 % of Colombia’s total imports.

Note: Millions of dollars (left axis) and percentage % (right axis).

Since these duty exemptions will take place under the commitment that imports are used to manufacture and export finished goods, it is possible to identify the Colombian goods exported that benefited from the siep scheme.2 According to Figure 1b, in the last ten years, annual exports associated with the siep program have averaged around usd 12 000 m, of which about 58 % (usd 6960 m) correspond to non-manufactured products (agricultural and mining); the remaining 42 % (usd 5040 m) correspond to manufactured goods.3 In the case of agricultural and mining exports, it is interesting seeing their extreme concentration in a few products, such as coal, coffee, bananas and flowers. Therefore, given the high concentration of these commodities and their unique features, the present work will focus on manufacturing exports.

3. Data

Customs data on exports and imports at the transaction level were used. Both data were available monthly, and, for the present study, exports and imports were aggregated at the annual level. The data covers the period 2011-2019 and draws on the disaggregated-level data from the Customs agency (dian) and the Colombian National Administrative Department of Statistics (dane). These data include information on the universe of Colombian exporters and importers, the trading firm’s tax identification number, the HS10-digit product code (according to the Nandina classification, based on the Harmonized System), fob and cif values (both in U.S. dollars and Colombian peso) and volumes (net kilograms), the country of destination (for exports) and origin (for imports), and a variable for when the export and import were served under siep, among other details.

Data on imports are collected for several purposes. First, to identify those exporting firms that are using imported goods and, thereby, to have a more homogenous group of comparison in the empirical strategy. Second, to compute the import and vat duty rate paid by exporting firms. Third, to identity tax-exempt imports due to the siep and, thus, estimate how much they would have paid in the absence of the program.

The identification strategy focuses only on manufacturing exports according to isic classification (Rev. 4), excluding exports of coke (isic 1910), refined petroleum products and nuclear fuel (isic 1921 and isic 1922) and basic metals, which include gold, silver, platinum, and nickel (isic 2410 and isic 2421). These products are excluded since their dynamics are more associated with commodities producers rather than other manufacturing firms. In addition, following Balance of Payments (bop) recommendations about residency, those transactions between residents (customs territory and free zones) are excluded, and thereby only exports from Colombia to the rest of the world are considered.

3.1. Some descriptive statistics

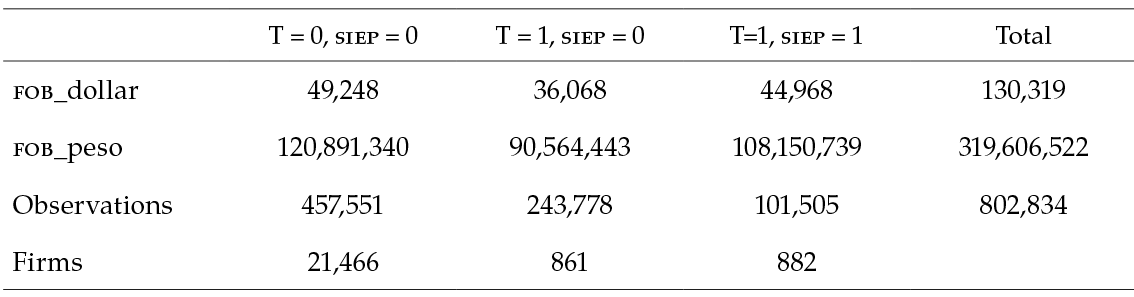

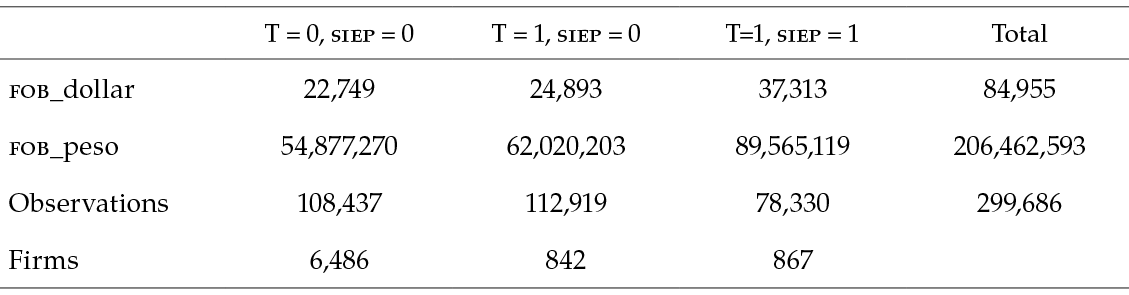

First of all, it is important to stress the relevance of siep in the total manufacturing exports in Colombia. From Table 1, some key points on this matter can be highlighted. Between 2011 and 2019, the exported value of Colombian manufactured products (fob_dollar) was around usd 130 318 m, of which usd 49 284 m (38 %) correspond to 21 466 non-beneficiary firms (T = 0) that never benefited from the duty drawback scheme (siep = 0).

The remaining 62 % corresponds to exports served by beneficiary firms (T = 1) which have used the duty drawback regime (T = 1, siep = 1) but also the ordinary regime (T = 1, siep = 0). Thus, the siep beneficiaries account for 882 manufacturing firms who have reported having exported at least once under the siep during 2011-2019 (usd 44 968 m accounting for 34 % of the total). Of these firms, 861 serve exports both with and without siep (siep = 1 and siep = 0, respectively); only 21 (difference between 882-861) have been able to serve exports exclusively under the siep regime.

Despite the siep’s contribution to a large share of total exports value in the last decade (34 %). Unfortunately, only 882 firms have taken advantage of it, showing that the policy is highly concentrated in a few firms. This may be explained by two reasons: i) misinformation from the firms about how the scheme works or ii) that the high administrative costs of complying with the requirements more than outweigh the benefits associated with customs exemptions, which tend to decrease due to the trade agreements that have lowered tariffs.

3.1.1. Intensity Using the siep

The siep beneficiaries account for 882 manufacturing firms who have reported having exported at least once under siep during 2011-2019. As shown in Table 1, this group of firms contributed 62 % (usd 81 035 m) of the total Colombian manufacturing exports over the period considered and 43 % (345 283) of the total observations.

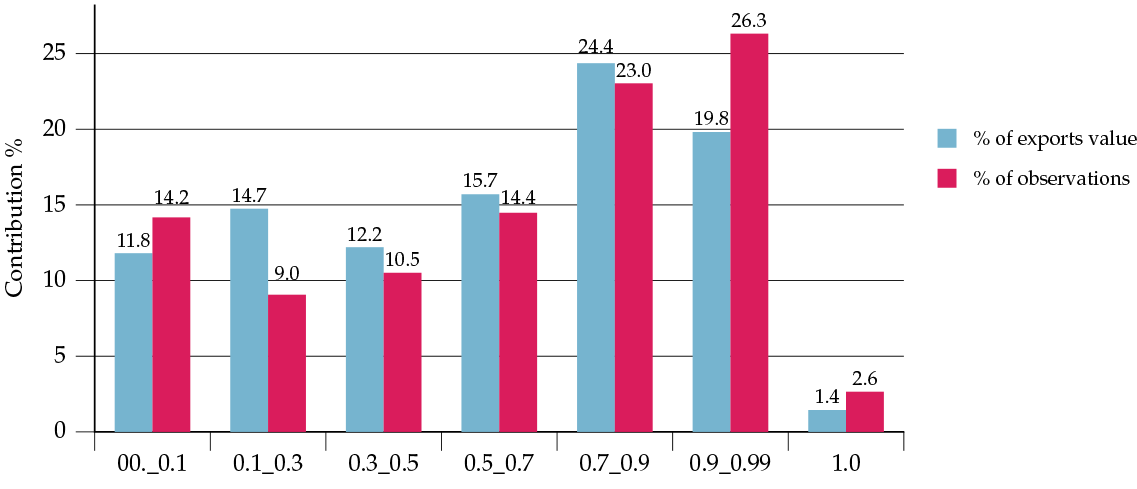

Figure 2 classifies the 882 firms according to their intensity using the siep scheme. This intensity indicator (called siep share), shown in the horizontal axis, is the share of observations (weighted by export value) using siep during the period 2011-2019 and goes from zero to one. If 100 % of a firm’s export is channeled through the siep scheme, this firm will be part of the last pair of columns. On the contrary, if only 5 % of a firm’s export was served using the siep, they will be in the first group or interval. The vertical axis represents the contribution of each group to the total export value and total observations. For instance, the last two bars (0.9-0.99 and 1.0) represent the contribution of the 200 firms that have (or almost) fully benefited from the duty drawback, which as a whole contribute with the 29 % and 21 % of 882 firms’ export values and observations, respectively. On the contrary, the [0.0_0.1) interval accounts for those firms whose export under the siep represents less than 10 %, contributing 12 % and 14 % of total exports and observations.

In short, out of the 882 beneficiary firms, 682 have benefited partially from the siep (less than 90 % of the exports were done under the siep), accounting for the 71 % and 79 % of exports value and observations of the total 882 firms, whereas the remaining 200 firms have fully benefited from this program (exports under siep is greater or equal to 90 %), representing the 29 % and 21 % in terms of value and observations.

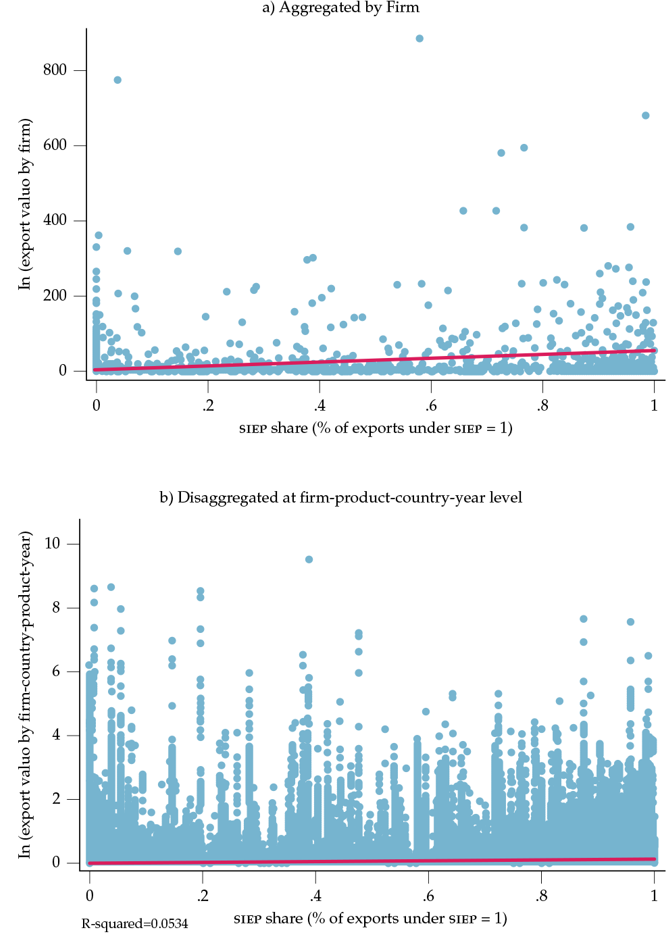

Figure 2 gives an overview of the contribution of each group of beneficiary firms, classified according to the intensity of the use of the siep during the period. However, this measure is aggregate and does not show the variability between firms. Therefore, in Figure 3, two indicators are plotted for each individual firm, including beneficiary and non-beneficiary firms.

In both graphs, the horizontal axis represents the intensity of the policy, which is distributed between 0 (non-beneficiary) and 1 (fully beneficiary), and the vertical axis is the corresponding export value. The main difference is the level at which these measures are computed. While each dot in Figure 3a represents one specific firm during the whole period (most aggregated level), in Figure 3b, this stands for the most disaggregated transaction level (firm-product-country-year).

A value of 1 indicates that 100 % percent of the export has been served under the siep regime, while a value of 0.2 means that only 20 % was served under this system. For non-beneficiary firms (Figure 3a) and non-beneficiary transactions (Figure 3b), this variable will be zero. The red line represents the fitted values between the siep share and export value (in natural logarithms), showing a very slightly positive relationship between both variables at the aggregated level (panel A, R-squared: 0.1457) but no apparent relationship at the transaction level (panel B, R-squared: 0.0534). This would suggest that large export values are not necessarily associated with higher intensity using the program. The empirical approach shown in section 5 will take advantage of this heterogeneity in the treatment exposure —distributed on [0,1]— by including the measure at the most disaggregated level.

3.1.2. Imported input duties and the siep

Since the siep allows producers to ask for duty exemptions on imported products used in manufacturing exported goods, it is relevant to decode the two components of the import duties: the tariffs and the vat. Using the imports database allowed computing the effective import duty rate paid by each manufacturing exporting firm f at year t (DutyRatef, t), using constant initial weights (ωf, p, c, t0) as follows:

Note: In figure 3a, the export values by firms (vertical axis) and the siep shares (horizontal axis) represent the accumulated export value and percentage of exports served under the siep between 2011 and 2019, respectively. In the graph on the right, export value and siep share are measured at the firm-productcountry-year level observation.

(1)

(1)Where τf, p, c, t is the effective import duty rate paid by the firm f for a specific product-origin country pair (p, c) at year t, and it is calculated as the customs duties in local currency as the percentage of the import cif value in local currency:

(2)

(2)Since firms import a broad basket of products (HS10) from several countries, these duty rates (τf, p, c, t) were averaged considering the initial weight of each specific product-country import value (ωf, p, c, t0); thus, obtaining the weighted average duty rate paid by each exporting firm every year, DutyRatef, t. These calculations were computed excluding consumer goods from the imports database following cepal (1972) classification for Latin America and the Caribbean. Using a constant initial weight to compute firm level input duties had some advantages, like reducing potential reverse causality concerns between changes in firm-product export prices (and quantities) and variations in the imported input mix over time (Bas & Strauss-Kahn, 2015).

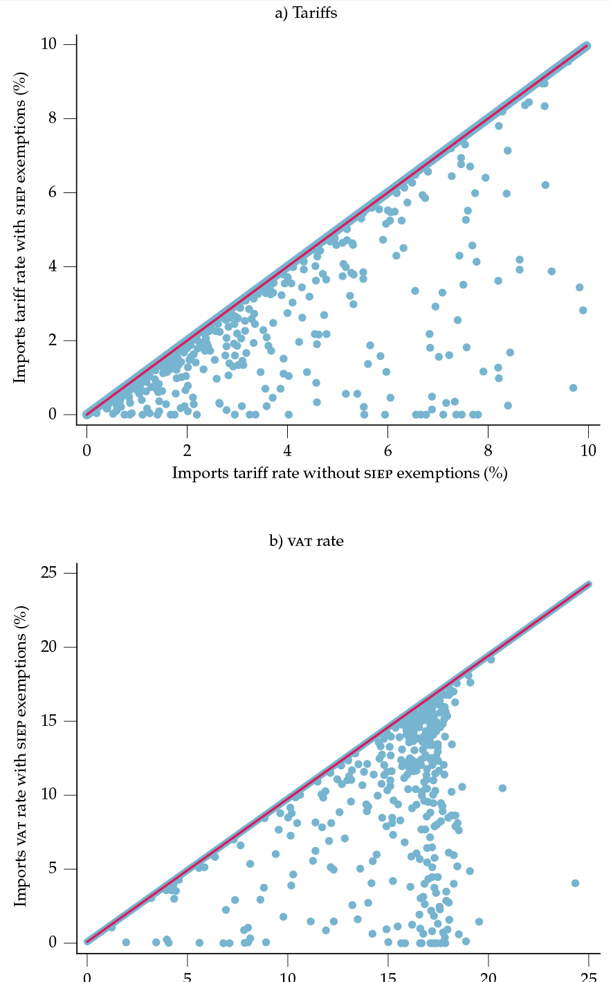

To consider the customs duties exemptions on imports due to the siep, two types of duty rates by firm-year were calculated: DutyRatef, t with and withoutsiep exemptions. Since most of the program beneficiaries also i mport under an ordinary regime without siep’s benefits, the duty rate for these firms was estimated as the weighted average of both regimes, using a constant share for each type of regime (according to the regimes’ accumulated import value during 2011-2019). This latter point is crucial because exporting firms are able, through the ordinary and special regime (siep), to import intermediate and capital goods to be used in the production of one specific product to be exported. For the sake of better understanding, the following hypothetical example is used. Suppose that a shirt producer firm that imports buttons, under the customs siep-free duty payments, the same year imported fabric and parts for its weaving machine, paying an import duty rate (tariff and vat) of 19 % and 16 %, respectively. The overall import duty rate of this firm will take into account all the taxes paid for the products used in the shirts’ production process: 0% for buttons, 19% for fabric, and 16% for parts.

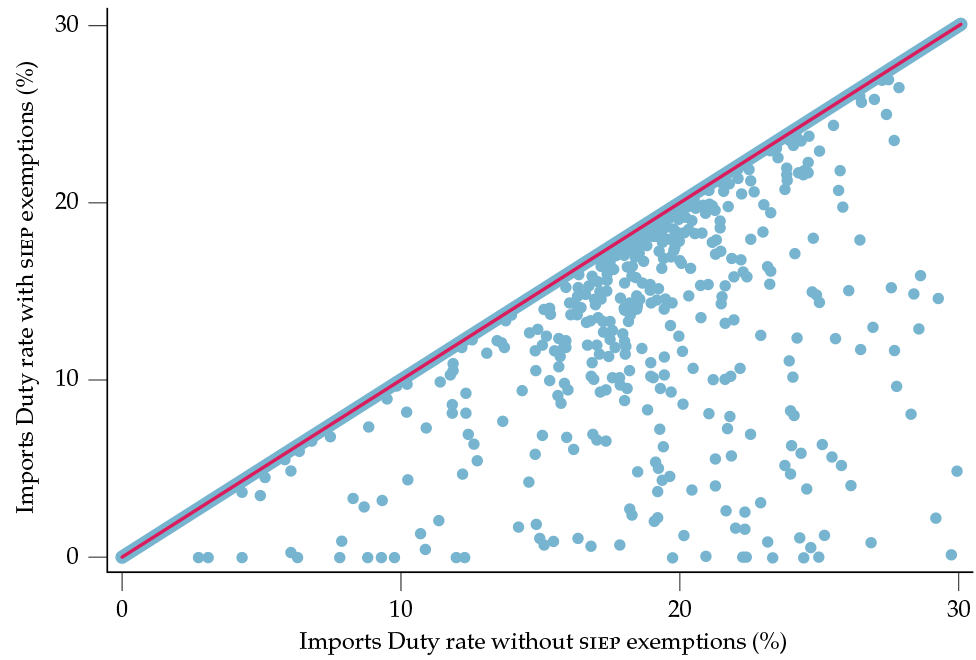

The results in Figure 4, for simplicity, were averaged by firms between 2011 and 2019 (DutyRatef). Each dot represents a firm, 22 348 firms in total according to the entire universe of manufacturing exporters (see Table 1). Thus, non-beneficiary firms that have never benefited from the siep (siep share = 0) will lie on the 45 % line; there is no difference between the duty rate with and without siep exemptions since they are not taking advantage of them. Below the 45 % line, we see beneficiary firms (siep share > 0). As most of them have used the ordinary and siep regimes to serve exports and imports, there is a difference between the duty rate with and without siep. The larger the horizontal distance with respect to the 45 % line, the higher the duty benefit a firm has taken since, for all beneficiary firms, the condition DutyRate with siep f < DutyRate without siep f is always satisfied. The results for tariffs and vat are shown separately in Appendix B.

4. Eligible Sample of Firms and Final Sample

One of the main challenges of evaluating a policy that has been in place for so long, not randomly allocated, is the self-selection treatment. Estimating the treatment effect implies that one needs to determine how exports would have been in the absence of this support, which is essentially a counterfactual analysis. Constructing a valid control group to get a proper counterfactual may turn out to be a challenging task, as differences among beneficiary and non-beneficiary firms may not be random to potentially different export outcomes. For instance, relatively larger and more experienced firms may be more likely to be aware of and use export promotion services (Ahmed et al., 2002; Kedia & Chhokar, 1986; Reid, 1984). In other words, this implies that for each firm that accesses the siep, we need to find a comparison firm that is subject to the same shocks and characteristics as the treated firm but did not participate in the siep program.

At the firm level, as shown in Figure 5, there were several types of exporting firms in the initial sample. Those that did not benefit at all from the duty drawback program because they do not use imported goods (Group 1) and if they did, they did not wish to comply with the required administrative procedures and ask for the exemption (Group 2). Within those firms that exported under the siep program (Group 3), there are firms that fully benefited from this scheme (Group 4) and others that partially benefited because some exports were done with and without the duty drawback scheme (Group 5).

Using customs data allowed identifying exporting firms that are also serving imports (intermediates and capital goods, consumption goods are excluded), thereby having a more homogeneous population of firms to focus on. Hence, the identification strategy considered the transactions made by those exporters that also served imports but were not benefiting from the duty drawback (Group 2) and the exporters which were benefiting from it in any degree (Group 3).

Furthermore, the methodology also ensures that the control group is similar to the treated group by guaranteeing that for each beneficiary firm, there is at least one non-beneficiary firm exporting the same variety to the same market in the same year.4 Likewise, non-beneficiary transactions at the product-country-year dimension without common support in the beneficiary group were also excluded. By this mean, we attempted to make both types of firms as similar as possible in their production processes and input requirements, as well as subject to the same foreign shocks (e. g., demand shocks).

Finally, as part of data cleaning to obtain the baseline sample used in the estimations, some observations were identified as outliers and deleted according to the import taxes paid relative to the cif import value, following blocked adaptive computationally efficient outlier nominators (bacon) algorithm proposed by Billor et al. (2000), which is a simple modification of the methodology proposed by Hadi (1992, 1994). These extreme values account for 1 004 observations that represent 0.12 % of total observations (802 834) and 0.07 % (usd 88 m) of total export value (usd 130,319 m).

After completing all the procedures just mentioned, the final sample was composed of 6486 non-beneficiary firms and 867 beneficiary firms (Table 2) instead of 21 466 and 882 from the initial sample. Although the matching and other procedures reduced the sample, the estimated one is highly representative of the full sample in terms of the total manufacturing exported value shown in Table 1. Thus, the selected final sample of observations accounts for usd 84 955 m (Table 2), which represents 65 % of the total value, and for usd 37 313 m associated with the siep regime (T = 1, siep = 1) contributing with 83 % of the original sample. Lastly, it is important to stress that 842 firms out of the 867 selected beneficiary firms served exports both with and without siep (siep = 1 and siep = 0, respectively), and only 25 (difference between 867-842) were able to serve exports exclusively under siep scheme.

5. Empirical strategy

In order to estimate the effect of duty exemptions associated with the siep on export outcomes within firm-product-destination, variation over time is exploited. This corresponds to estimating a treatment on the treated effect, where average gains in the outcome variable on the treated versus non-treated are compared. As stated before, the empirical approach will consider the transactions made by those exporting firms benefiting from duty exemption associated with the siep system (treatment group) in any degree —fully or partially— and those exporters that are also serving imports but are not benefiting from the siep (control group). In other words, in order to test the effects of duty drawback (exemption) policy on exports, the identification strategy exploits the variation and heterogeneity in imported input duties combined with the siep share over time and across firms. Furthermore, to reduce any concern of selection bias, the eligible population of observations was largely narrowed down.

The baseline specification to be used is a generalized difference-indifference approach where the treatment (duty rate with and without exemption) affects the treated group over time. Besides, instead of using a dichotomous variable of 0 or 1 to identify the treated and control group, a yearly measurement of the treatment intensity (percentage of exports served under the siep) is computed. This is because a remarkable group of firms is exporting the same product (HS10) to the same destination country in the same year, with and without the siep benefits (as it was presented in Figure 3).

Clearly, factors other than duty drawbacks may affect firms’ foreign sales. A possible strategy to isolate these potential confounders consists of using more disaggregated export data and including appropriate sets of fixed effects in the equation estimated. The present paper adopted that approach. In particular, the following fixed-effects model of exports was considered:

(3)

(3)Where Yfpct corresponds to the export quantities (kilograms) of product p by firm f to country of destination c in year t. Product p stands for products at the Harmonized System-10-digit level, and f for yearly data between 2011-2019. To make up for the potential circularity and simultaneity problems, all right-hand side variables in equation (3) were one year lagged, except for the treatment intensity indicator (siep share) since it is firm-product-destination-year specific.

The focus on quantities was motivated by the evidence of under-reporting practices of export values by exporters to avoid paying taxes based on export values (Ferrantino et al., 2012). Besides, quantities are more easily observable by customs authorities and, hence, might be less subject to such misreporting practices (Gourdon et al., 2014). However, results using export values are also estimated and reported.

Dealing with disaggregated data allows us to identify the different transactions of each firm, both those with and without siep and, thus, for the same firm f, product p, to country destination c in t time t, we might have observations with siep = 1 and siep = 0. Therefore, siep sharefpct stands for the percentage of observations (weighted by export value) that benefited from tariffs and vat exemption under the siep. Hence, the variable siep sharefpct takes the value of 0 if the firm-product-destination observation in that year does not benefit from the siep, the value of 1 if it fully benefited, and continuous values between 0 and 1 if it benefited partially. Results shown graphically in Figure 3 (panel B) are now included as the measurement of treatment degree.

DutyRatef, t – 1 corresponds to the average import duties rate effectively paid by firm f in year t-1. This rate is estimated following equations (1) and (2), previously presented in Figure 4, exploiting the disaggregated nature of the database. Since we are interested in estimating the impact of duty exemptions associated with the siep policy, it is necessary to estimate the duty rate for both plausible scenarios: with and without siep exemptions for each firm, depending on if the specific firm-product-destination-year observation is benefiting from it or not. Thus, if siep sharef, p, c, t = 0, the DutyRatef, t – 1 to be considered will be without siep exemptions. On the contrary, if siep sharef, p, c, t > 0, which means that is benefiting from the duty exemption in a positive degree, the duty rate will correspond to the one with siep exemptions. This allows us to distinguish where the duties variation comes from. Since the tariffs and vat refer to a specific input used by the firm, using input duties computed at the firm level is more precise than aggregated Input-Output (io) data.

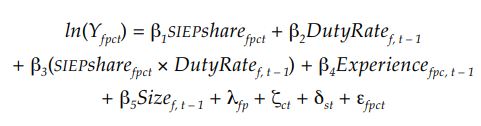

Coefficient β2 measures the impact of imported input duties on export quantities and is expected to be negative, as has been supported by literature regarding trade policy and export performance in Colombia (Echavarría et al., 2019; Giraldo, 2015). β3 is, accordingly, our main parameter of interest, and it would be capturing the marginal and additional impact of changes in tariffs and vat for siep beneficiaries. Therefore, the effect of import duties on the exported volumes of firms that use the siep program will depend on both β2 and β3 coefficients and the exposure to treatment as follows: (β2 + β3 × siep share). On the other hand, the impact of imported input duties on exports not benefited by the policy (siep share = 0) is measured solely by β2.

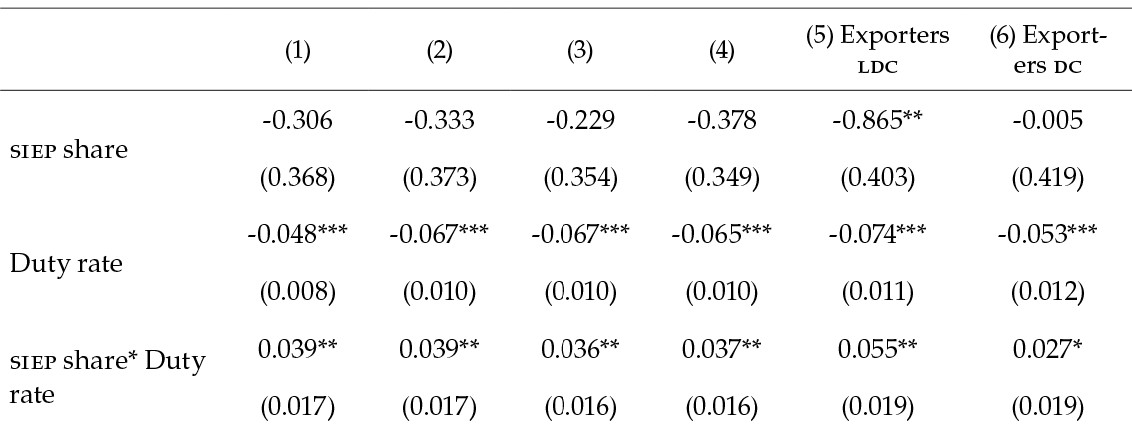

Later on, additional control variables one-year lagged (t-1) were added, such as a proxy of the firm size and the experience of the firm f exporting a specific product p to a market c. The experience variable is defined as the natural logarithm of the number of years a firm f has been sourcing a product p to a country c since the start of the sampling period. Previous export experience can be an important determinant of the ability to enter new countries and product export markets (Love et al., 2016; Volpe Martincus & Carballo, 2010b; Yeoh, 2004). As a proxy of firm size and productivity, the one-year lag of the natural logarithm of the number of countries the firm exports to was considered. The above follows the findings in the literature regarding the positive correlation between a firm’s productivity and the number of products and countries traded: the so-called multi-product and multi-destination firms (Bernard et al., 2011; H. Fan et al., 2015; Helpman et al., 2004; Iacovone & Javorcik, 2010; Wagner, 2012; Yeaple, 2009). Including these covariates as a proxy of a firm’s experience and size allowed us to control for time-variant confounders that could potentially affect both usage of export promotion programs and export outcomes and, therefore, untreated and treated firms of similar size and experience are compared.5

The remaining terms of equation (3) correspond to fixed effects to control for unobservables. Thus, λfp is a set of firm-HS10 product-fixed effects that captures the firm’s knowledge of the market for a given product and other firms’ characteristics such as performance (e. g., productivity in that specific product), as well as the companies’ changing abilities to comply with customs regulations. ζct is a set of country destination-year fixed effects that controls for time-variant country destination shocks, such as fluctuations in demand for goods across markets and for time-varying trade costs (e. g., tariffs and non-tariff measures) associated with customs and other administrative procedures in the country destination. We further add sector-year dummies δst to control for time-varying sector specificities at 4digit-isic classification (supply and demand shifts common to products of a given sector). Finally, εfpct is the error term. Nevertheless, despite these corrections to control for unobservable factors and concerns about the endogeneity of participation in the siep, some time-varying unobserved policies and firms’ features might have been omitted.

To control for potential heteroscedasticity and correlation between errors across observations, results are reported with robust (white) standard errors clustered at the firm level, which tends to give further (more conservative) estimates for standard errors (Abadie et al., 2017; White, 1980).

6. Results

6.1. Benchmark Results

6.1.1. Export Quantities

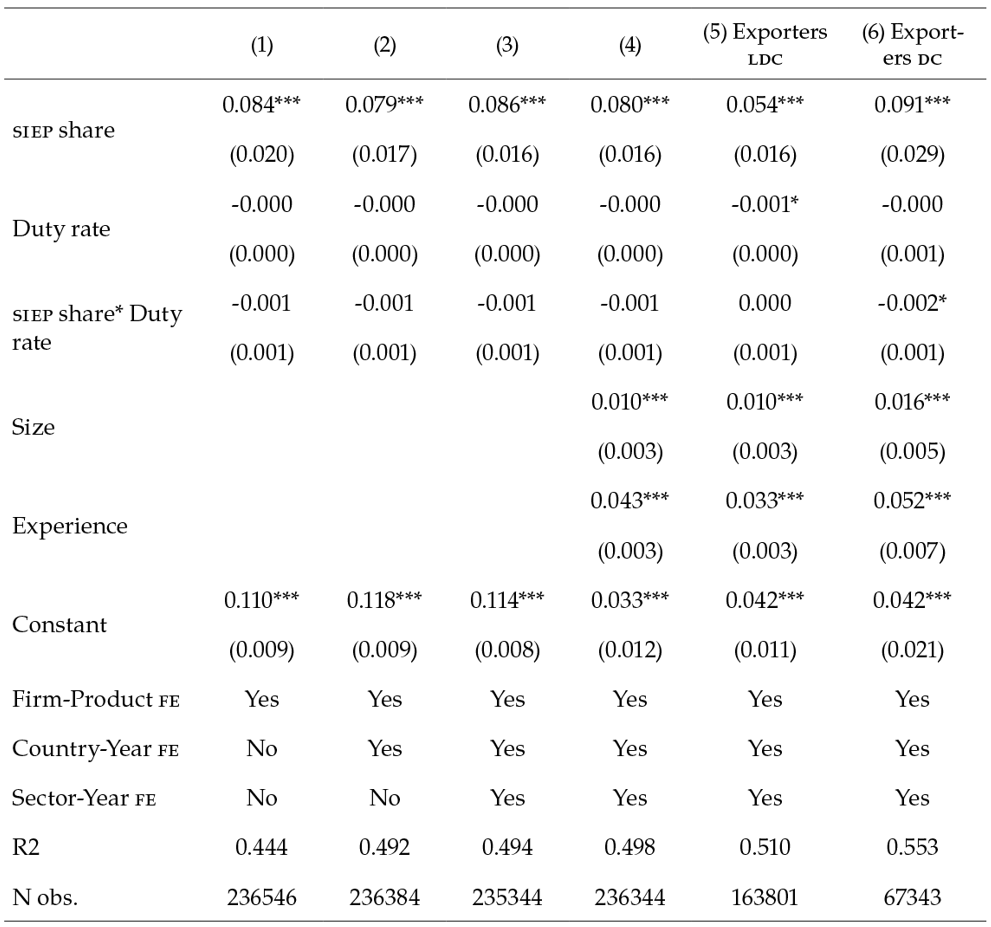

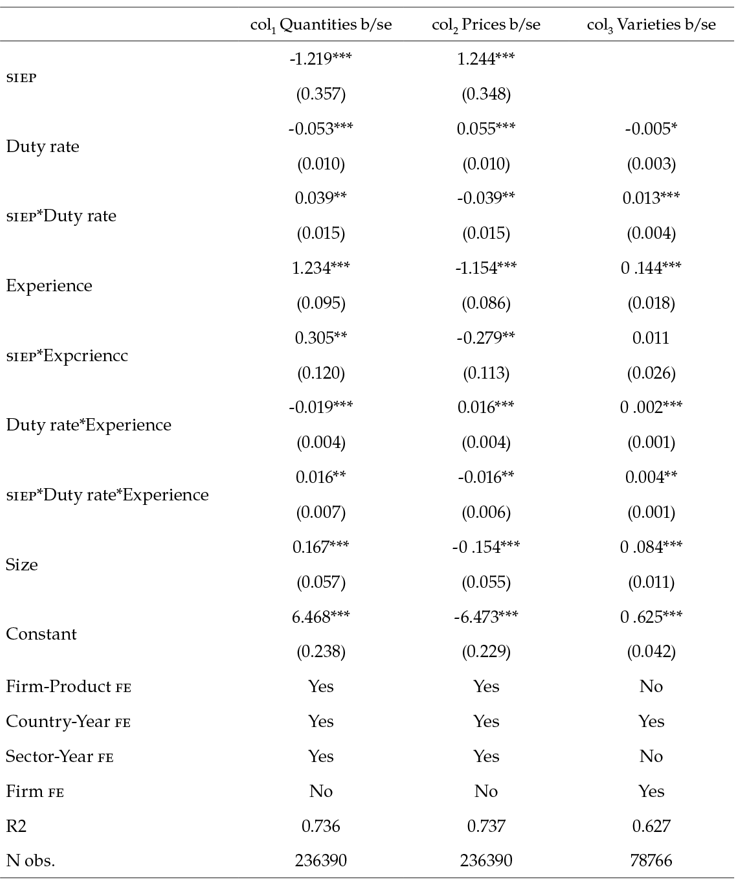

Table 3 presents the results of regressing firm-product-destination-time export quantities on import duty rates interacted with siep share for several specifications. The fixed effects in equation (3) are sequentially included from columns 1 to 3; column 4 shows estimates including additional control variables —Size and Experience.

Relying on column 4 —the most robust specification—, the duty rate coefficient shows the impact of intermediate input duties on export quantities for non-treated observations ( siepshare = 0) is significantly unfavorable. A one percentage point (pp) raise (decline) in the import duty rate decreases (increases) manufacturing export quantities by 6.5 %. Almost half of this impact is compensated if the export benefits from any siep exemption, measured by the interaction term coefficient (3.7 %), which captures the marginal and additional impact of changes in tariffs and vat paid by the treated group due to the siep scheme. The interaction term shows a positive and significant impact (5 % level of significance) on export quantities for siep beneficiaries. This impact increases as siep share rises.

The above indicates the duty drawback policy partially compensates for the effect changes in input duty rates have on exported volumes. For instance, assuming the siep share equals 1 (the group most exposed to treatment), meaning that firm-product-destination-time observation fully benefits from the program, a one pp rise (fall) in import duty rate would decline (raise) export quantities by 2.8 (-0.065 + 0.037*1), much lower to 6.5 % of non-beneficiary exports (control group). It would indicate remarkable gains of the scheme in periods of input duty increases since it would “shield” the benefited firms from the negative effect of a tariff or vat raise. However, if an input tariff cut policy is taking place, the marginal and positive impact that these reductions might have on boosting exports is lower for firms that benefit from the regime compared to those that do not. That is because a share of their imports (already duty exempt), and, hence, of their exports, will not be affected by additional tariff cuts.

These results also suggest that the scheme would act as an insurance or smoothing mechanism to soften the impact of shocks in imported input duties, which could translate into less uncertainty for the exporting firms using siep, thereby improving their export performance. Higher uncertainty about tariffs dampens investment and gdp by reducing firm entry into the export market and triggering upward pricing bias, which increases markups and reduces hours worked and outputs (Caldara et al., 2019).

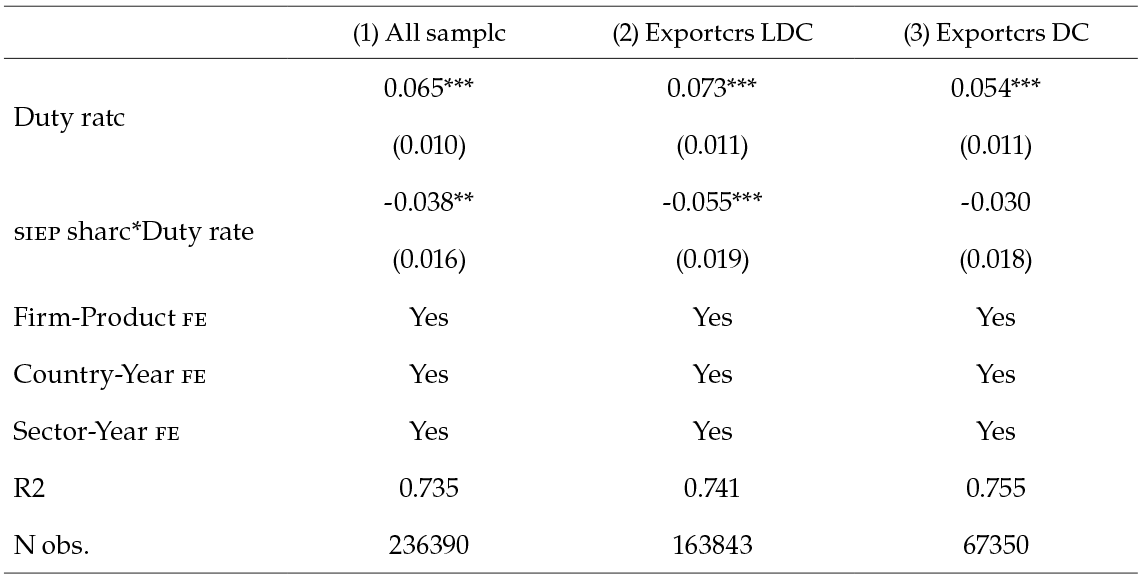

Column (5) considers only the subsample of manufactured goods exported to low and middle-income countries (ldc), whereas column (6) focuses on products exported to high-income countries (dc).6 The results suggest that the gains for exports that benefited from the siep exemptions are specific to products exported to non-high-income countries. As shown in columns (5) and (6) the coefficient associated with the interaction term remains positive and statistically significant (even at the level of 1 %) for products that are sold in ldc, and it has no significant effect on goods exported to dc. Thus, there is a link between duty drawbacks and destination countries’ level of development.

6.1.2. Export values

Table 4 reproduces the results when focusing on the value of exports in dollars as dependent variables (in natural logarithm). Contrary to the export volume scenario, neither β2 nor β3 are statically significant, which indicates no gains in terms of export values given a change in import duty rates. As described in section 6.3, once the export prices (proxied by unit values) are considered, results suggest evidence that access to cheaper intermediate inputs may lead to lower production costs and export prices cuts (in dollars) for siep beneficiaries, which translates into a quantity increase. The decline in prices offsets the rise in quantities, and the export value in dollars remains constant.

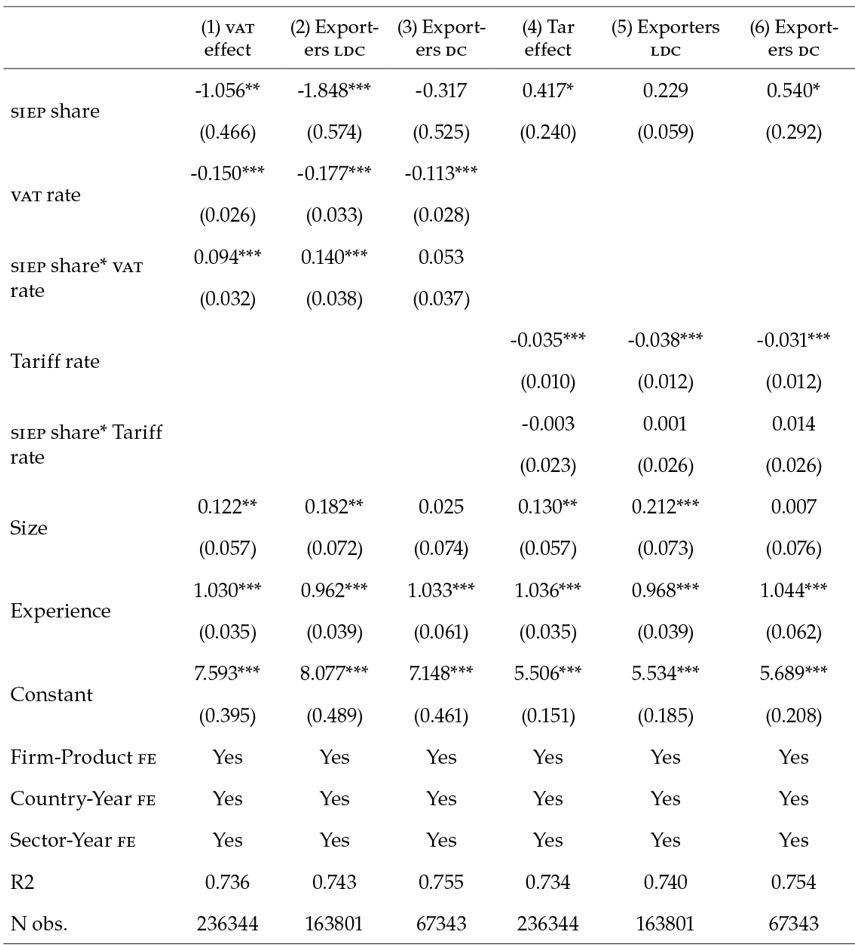

6.2. vat and tariffs effect

Since the total duty rate includes the tariff and vat paid by the exporting firm, it is relevant to estimate the effect of both duties separately. The imports database allows us to compute the effective tariff and vat rate paid by each manufacturing exporting firm f at year t, with and without siep exemption, calculated using equations (1) and (2).

Following the most robust specification that controls size and experience and includes all fixed effects (corresponding to columns 4, 5, and 6 in Table 3), equation (3) was estimated, including vat and tariff rates separately. Export quantities were used as the dependent variable; results are shown in Table 5 for the whole sample and the subsamples of manufactured goods exported to ldc and dc. From columns 1 to 3, the impact of vat is highlighted, whereas columns 4 to 6 report the tariff effects. Both vat and tariff rate coefficients show a significant negative impact on exported volumes for non-treated observations (siep share = 0), which in the vat case is compensated if the export benefits from the siep exemption, measured by the interaction term coefficient (0.094, column 1). The presumable role of the siep in Colombia is that it provides an outright exemption rather than requiring the firm to go through the refund (drawback) process, thus, alleviating plausible constraints in sourcing their imported inputs before exporting. Given the lack of detailed information, it is impossible to examine the effect of vat exemption vs. the standard refunding process which would be of considerable interest in how vat refunds affect exports.

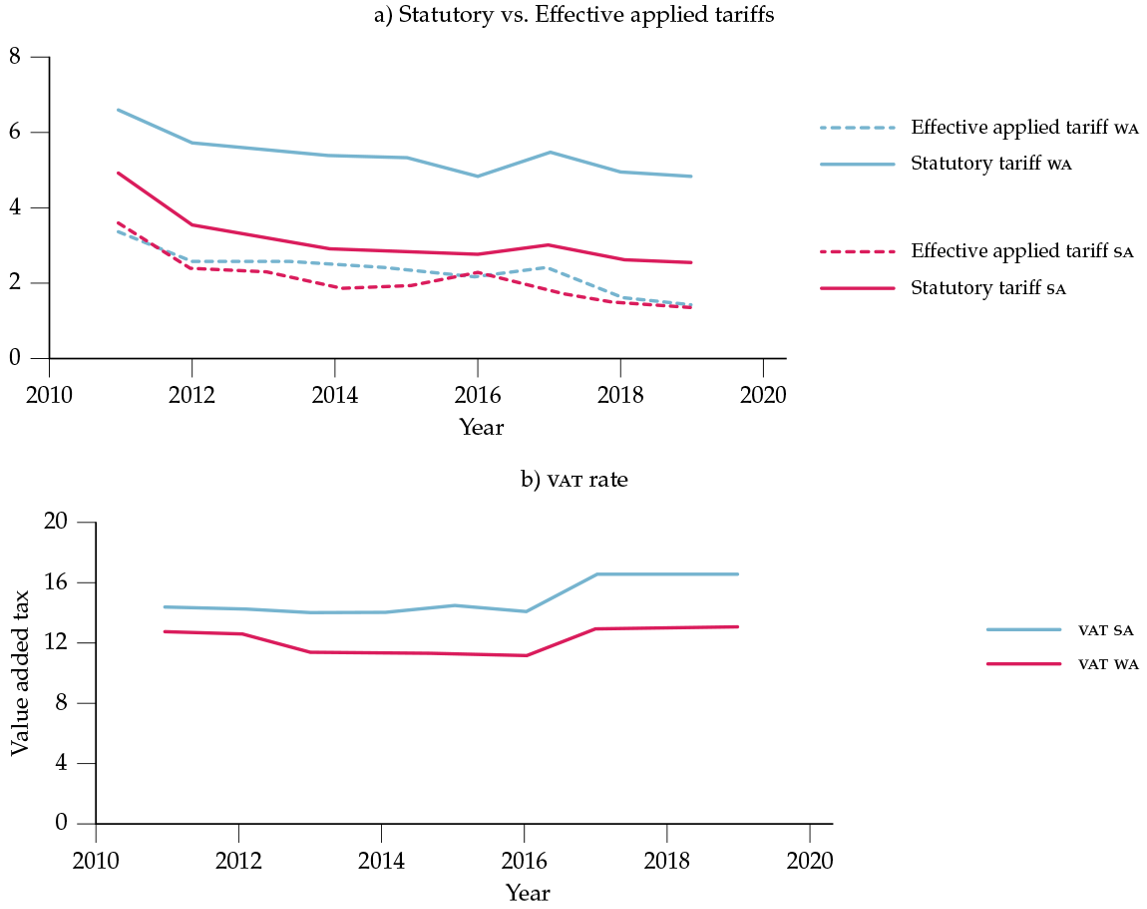

As highlighted later in section 8, there is a sizeable difference between the vat and tariff rates paid on imported intermediate goods. Depending on the average measure —simple or weighted— for the period 2010-2019, the statutory tariffs reached 3.16 % and 5.41 %, respectively (see Figure 8), whereas the effective tariff rate was 2.11 % and 2.33 %. Since the early 2000s, tariffs have declined on average because of unilateral decisions but also due to duty-free preferential access related mainly to the free trade agreements signed in the last few decades. On the contrary, the effective vat rates are substantially larger varying around 16 % in the previous decade (see Figure 8). Even though firms can subtract their input vat payments from their overall vat in liabilities, the results suggest that vat exemptions on imported inputs used to produce exports are a way to reduce costs and lead to exported quantities expansion.

6.3. Plausible Mechanisms and Results on Other Export Outcomes

6.3.1. Export Prices

Since the duty exemption scheme in Colombia aims to provide exporters of manufactured goods with imported inputs at international prices, the results must be analyzed through the channel of intermediate goods. A growing body of evidence shows that lower input tariffs can lead to increased productivity through access to more varieties and higher quality of intermediate inputs and learning effects (Grossman & Helpman, 1991; Markusen, 1989). There are essential sources of gains from trade by facilitating access to cheaper and more varied inputs. Increasing the type and quality of inputs available may improve the quality and variety of domestic firms’ products. Reducing tariffs on intermediate inputs can also boost competition between domestic and foreign suppliers (foreign input competition channel) and, thus, decrease the cost of inputs. Besides, providing easier access to new technologies available abroad facilitates their adoption by domestic firms, making them more competitive and efficient.

Assuming these mechanisms affect productivity, they will likely also impact the firms’ export performance. Gaining access to more varied and cheaper imported inputs can increase the probability of entering the export market (extensive margin) and make incumbent exporting firms more competitive, as a result, they will export more (intensive margin) (Bas, 2012; Lileeva & Trefler, 2010; Melitz & Trefler, 2012). Evidence shows that the productivity gains arising from lower tariffs on intermediate inputs are substantial, and these are much more relevant than pro‐competitive effects due to reductions of tariffs on final goods (Amiti & Konings, 2007; Goldberg et al., 2010; Topalova & Khandelwal, 2011). Other studies that considered the effect of imported inputs on productivity are Feenstra et al. (1992), Halpern et al. (2005), and Muendler (2004).

Furthermore, the duty drawbacks scheme reduces the costs of imported intermediate inputs and allows firms to decrease their marginal costs. Hence, ceteris paribus, a firm taking advantage of duty exemptions on imported goods will have a lower marginal cost compared to a non-beneficiary firm and, therefore will be able to set a lower output price (cost-efficiency effect), produce more output, and earn higher profits. Thus, they can adapt to the increased competition by lowering their markup (hence, their price) and gaining additional market shares (Melitz & Trefler, 2012).

Considering the theoretical mechanisms just mentioned regarding the ‘access to imported inputs’ channel, the effect of lowering input duties on output export prices (and markups) might be ambiguous. Whereas quality upgrading mechanisms prevail, a rise in export prices will be observed (Bas & Strauss-Kahn, 2015; Fan et al., 2015). On the contrary, productivity gains and reduced marginal cost (pass-through to clients) channels will push the prices down (De Loecker et al., 2016; Melitz & Trefler, 2012). This makes it difficult to identify the sources of the price response, whether it is driven by changes in marginal costs, qualities, markups, or compositional effects, such as heterogeneous price responses at the firm level or the reallocation of market shares between firms with different prices.

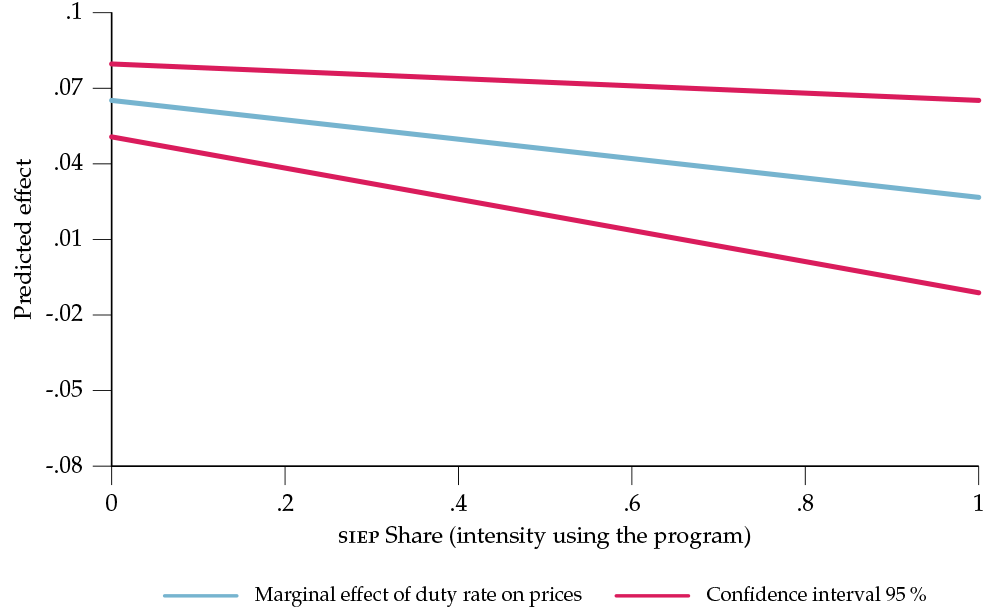

For addressing the impact on export prices, the same baseline specification in equation (3) at the firm-product-country-year level is regressed using unit values as the dependent variable.7 Although these estimates did not allow us to distinguish the source of the response, it allowed us to find out the overall change in prices, henceforth knowing which mechanism might be dominating.

The results for the variables of interest are summarized in Appendix C, and the estimated marginal effects of duty rate on export prices considering the whole sample are illustrated in Figure 6. These predicted effects (vertical axis) are computed along different intensity levels using the program (horizontal axis), going from 0 for non-treated observations to 1 for fully benefited exports. Values in the open interval (0,1) mean that the export partially benefits from the siep scheme; the higher the siep share, the higher the exposure to the siep exemptions, and vice versa. The blue line in the graph shows a positive and significant effect of import duty rates on export prices, and this coefficient decreases (remaining positive) as siep share increases. The coefficients are also more robust than a full passthrough effect of decreased tariffs on export prices (and hence on markups) since prices drop by more than 10 % for a tariff cut of 10 %. In addition, keeping constant the duty rate, the interaction term suggests that the higher the siep share (or the exposure to treatment), the lower the export prices (see Appendix C).

This is evidence that improved access to cheaper and more variety of imported inputs results in large price declines, hence, the channels of productivity gains, reduced marginal cost, or both would seem to dominate over quality upgrading mechanisms. In other words, the pass-through of a tariff cut to lower output prices would be the main plausible explanation to support the positive response of exported volumes to falls in import duty rates presented in Table 3.

6.3.2. Export Varieties

According to Melitz and Trefler (2012), trade expands product variety in final goods and specialized production inputs. This greater variety leads to more competition, which forces firms to lower their markups and prices. Balistreri et al. (2011) show that worldwide elimination of all trade barriers would raise the varieties available by about 3 %, lower manufacturing prices by a similar amount, and raise world welfare by 2 %. Furthermore, a duty drawback policy might affect a firm’s decision to introduce a new product. Input tariff exemptions lower the prices of existing imported inputs, and the resulting increase in variable profits raises the likelihood that a firm can manufacture previously unprofitable products (Goldberg et al., 2010). Also, there is a robust and positive correlation between productivity measures and products produced (De Loecker, 2006). Using us data, Bernard et al. (2006) found that trading a significant number of products is associated with higher levels of efficiency and productivity.

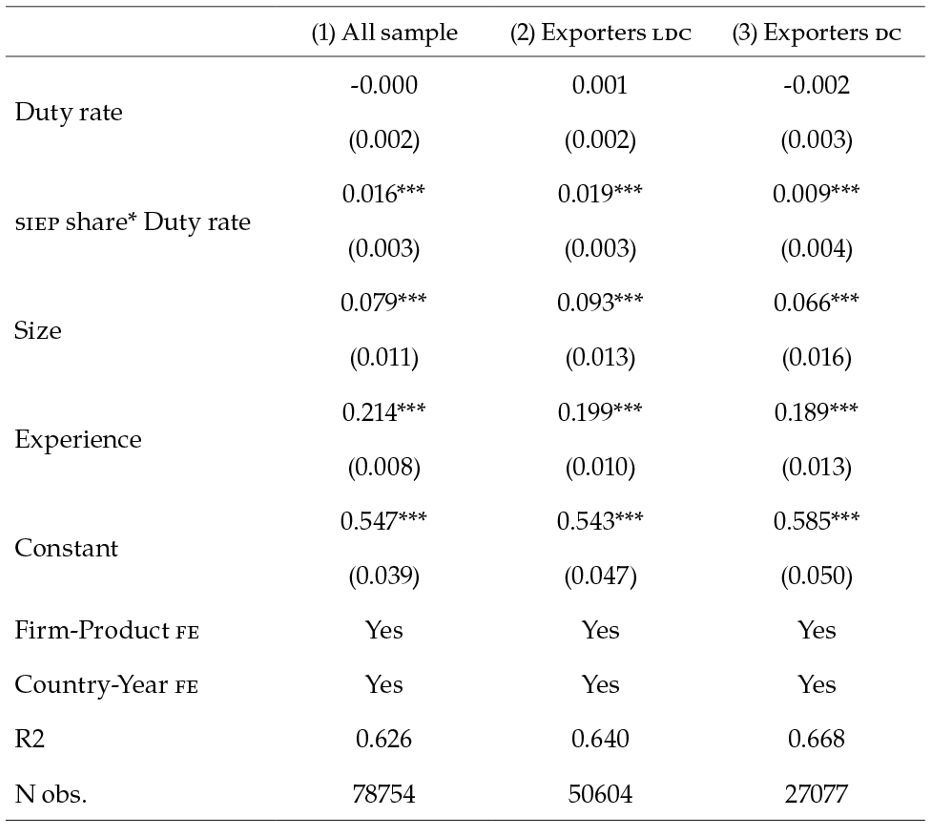

In other words, it is expected that firms exposed to larger imported-input duties cuts expand relatively faster in terms of export varieties. The following specification refers to the extensive margin regarding varieties within the firm-country-year —equation (4). The outcome of interest, Yfct, is the natural logarithm of the number of different products as the proxy of varieties (at 10-digit HS classification) exported by the firm f to country c in time t. Equation (4) follows a similar approach to equation (3) with two main differences. First, for simplicity, instead of using the siep share, the siep is a dichotomous variable that takes the value of 1 if the firm f has been beneficiary from the duty drawback scheme during the period of analysis (2011-2019) and 0 if otherwise. Second, due to the dependent variable specificity, the sample is collapsed at the firm-country-year level, and the product dimension is dropped. Due to this, the number of observations will be substantially smaller.

(4)

(4)Duty rate corresponds to the import duty rate paid by the exporting firm f at year t. The experience variable is the years a firm f has been exporting to country c at time t, and size represents the number of countries the firm exports to over time. Both variables are measured in natural logarithms, one-year lagged (see section 5 for details). The remaining terms of equation (4), λf and ζct, are a set of firm-fixed and country destination-year fixed effects, respectively. The variable of interest is the interaction term siep f× DutyRatef, t – 1), and the coefficient β3 provides the effect of imported-input duty rates for treated firms relative to the control group. Note that the dummy variable siep f does not vary within firms over time. Because of its collinearity with firm-fixed effect, it will drop from the estimation.

Table 6 shows the results using the preferred specification, including all the corresponding fixed effects and proxies of firm size and experience as time-variant control variables. As before, column (1) indicates results for the whole sample, and columns (2) and (3) account for less developed and high-income countries subsamples, respectively. Results show a positive and statistically significant sign for the interaction term of duty rate and treatment group: A rise in import duty rates is associated with an increase within firm export varieties over time and across countries of destination. Relying on column (1), a 1 pp increase in imported-input duty rates raises export varieties by 1.6 % for those firms exposed to siep policy relative to those not benefiting from the treatment. However, if a duty cut takes place, firms not exposed to siep will expand relatively faster in terms of export varieties. The effect is statistically significant at 1 % of confidence and becomes stronger once the subsample of firms exporting to ldc is considered.

6.3.3. Heterogenous effects by firm experience

In general, firms that have traded with more countries and accordingly have faced entry processes in more markets are more likely to be users of the export promotion policies (Volpe Martincus & Carballo, 2010b). Unlike the services provided by export promoting agencies (epas),8 which mainly focus on reducing information costs and have a greater impact on exports through the extensive margin (e. g., becoming an exporter penetrating a new market or starting exporting a new product) rather than through intensive margin (e. g., share of exports over total sales) (Lederman et al., 2015), the beneficiaries of the siep scheme must have a vast knowledge of the international market to sell not only their products but also previous experience sourcing their imported inputs.

Hence, besides evaluating the impact on export outcomes, another central policy question related to export-promoting policies is the type of firms that these programs are mainly benefiting. The aim to answer whether duty drawback schemes have had heterogeneous effects over the distribution of the relevant export outcome variables and what kind of firms (newly or with more experience) benefit most from these programs.

These differences across firm experience might be related to heterogeneity in access to information (e. g., through market studies) and the ability to cope with high entry fixed costs (Melitz, 2003). To explore this hypothesis, the measured experience, already included in the previous results, is now interacted with the variable of interest: the DiD coefficient (the interaction term of Duty rate and siep indicator), taking into account all the export outcomes (and their corresponding specifications) analyzed along this section: quantities (Table 3) and prices and varieties (Table 4). For simplicity, all the sample is considered without distinguishing between countries of income destination.

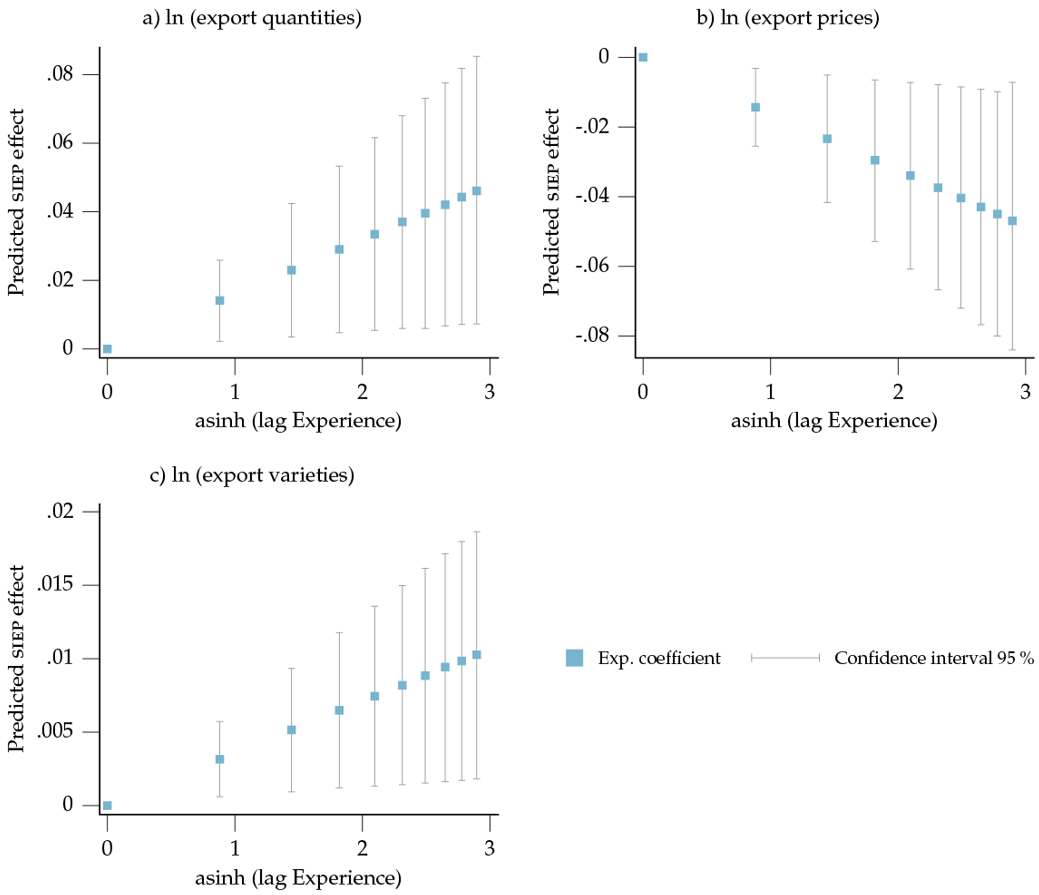

The results for the estimated parameters are presented in Appendix D, and the corresponding estimated marginal effects of duty exemptions due to siep depending on the level of firm experience (siep * Duty rate * Experience) are illustrated in Figure 7. Three dependent variables of interest are considered for firms’ exports, measured in natural logarithms: quantities (Figure 7a), prices (Figure 7b) and varieties (Figure 7c). As can be seen on the horizontal axis, the firm-experience variable (lagged one year) takes ten different variables, ranging from zero to 2.89, with larger values indicating a higher experience.9

Results on panel Figures 7a and 7c point out that the impact of siep on export quantities and varieties increases as the firm experience rises. The coefficient is statistically different from zero (with a confidence interval of 95 %). In both cases, the predicted siep effect for firms with the highest experience sourcing a product in a market (asinh(lag Experience) = 2.89) is more than twice those less experienced firms (asinh(lag Experience) = 0.88). In addition, access to a cheaper variety of imported inputs due to siep results in export price declines, which become prominent as the firms’ experience improves (Figure 7b). Thus, the effects of siep program on volumes, prices and varieties seem to be stronger for firms that have more export experience.

Note: All estimations control for firm size and experience and for firm-product, country-year and sectoryear fixed effects (see Appendix D).

7. Robustness checks

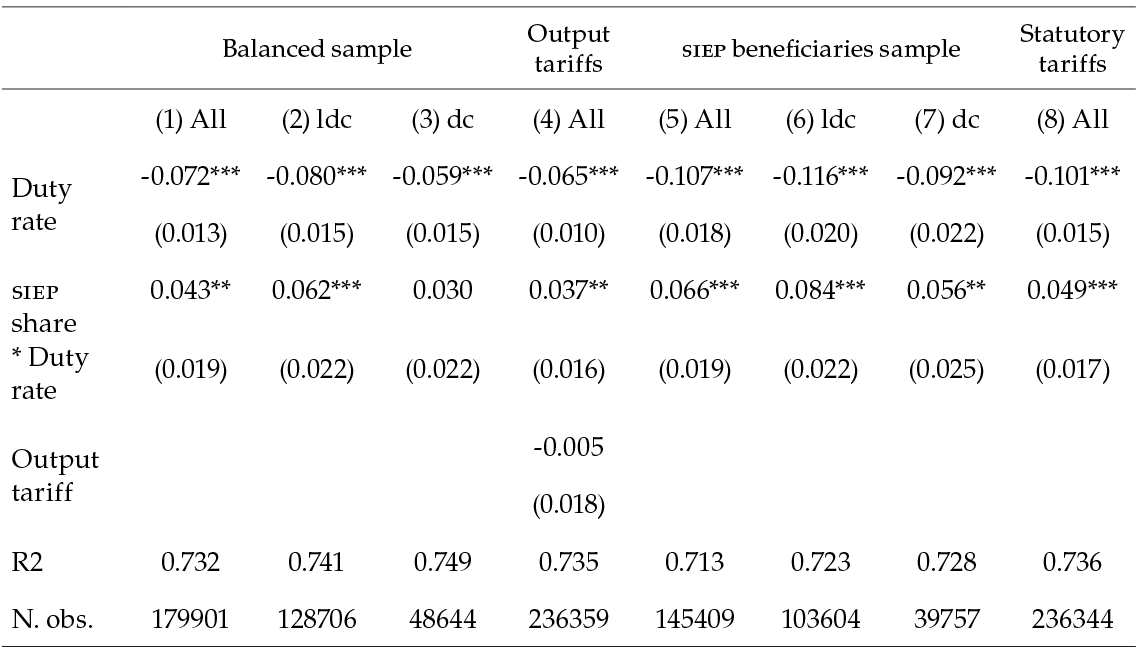

As a first robustness check, the benchmark specification is regressed on the subset of firms present over the entire period from 2011 to 2019. Results found with this balanced sample are reported in columns (1) to (3) of Table 7, considering the entire sample and the disaggregated countries’ subsamples (ldc, dc). Although the number of observations is substantially reduced, excluding non-surviving firms does not qualitatively change the findings. The coefficients on export volumes are not statistically different from coefficients of the main specification in columns (4) to (6) of Table 3.

In addition, it was also verified that output tariffs do not drive the results. Several studies have found that lower output tariffs have boosted the productivity and export growth of firms competing with imports due to the ‘import competition’ channel (Pavcnik, 2002; Trefler, 2004; Tybout et al., 1991). Lower output tariffs bring foreign competition and can induce domestic firms to improve performance. However, as Amiti & Konings (2007) points out, the largest productivity gains arise from reducing input tariffs rather than output tariffs. For this study, output tariff refers to domestic legislated import tariffs on the sector (at HS6-digit) of the product exported by the firm. Results in column (4) of Table 7 suggest that including this variable in the benchmark specification does not change the magnitude of the variables of interest.

Regarding endogeneity related to the identification strategy, there are two main concerns. The first one refers to the self-selection bias in the treatment. The beneficiary firms of the siep may differ from non-beneficiary firms concerning the observed characteristics. The identifying assumption is that all the relevant variables that affect the selection process for duty exemptions due to siep and outcomes of interest are known. This is the so-called conditional independence assumption. Several procedures were carried out to reduce this bias and ensure that estimates are not driven by unobserved information and self-selection. These comprised choosing carefully the eligible sample of observations and firms to be included —those subject to the same shocks and characteristics as the treated firm but did not participate in the siep— controlling for firm experience and size (measured by proxies stated in the literature), and including fixed effects to control for unobservables across firm-product-country-year dimensions. However, there may still be differences in characteristics between the control and treatment groups not observed by the econometrician.

The concern mentioned above is addressed by considering only the subsample of firms that have benefited from siep exemptions at least once over the period (see Table 2, section 4). This selected group of firms comprises 867 beneficiary firms, most of which have served exports with (siep share > 0) and without siep (siep share = 0). The baseline specification using export quantities as the dependent variable is regressed on this subset. Columns (5) to (7) in Table 7 report the estimates for the variables of interest. Although the sample size is largely reduced (from 236,390 to 145,409 observations), the coefficients on the impact of duty import rates on export quantities have the same sign as before: negative for non-treated exports (siep share = 0) and positive for treated ones (siep share > 0) and are significant at a 99 percent level. Note, however, that the estimated coefficients are larger than those in the benchmark results presented in Table 3. This might be due to the difference in sample size and the likelihood of siep beneficiary firms being more intensive in either imported capital goods or intermediate inputs.

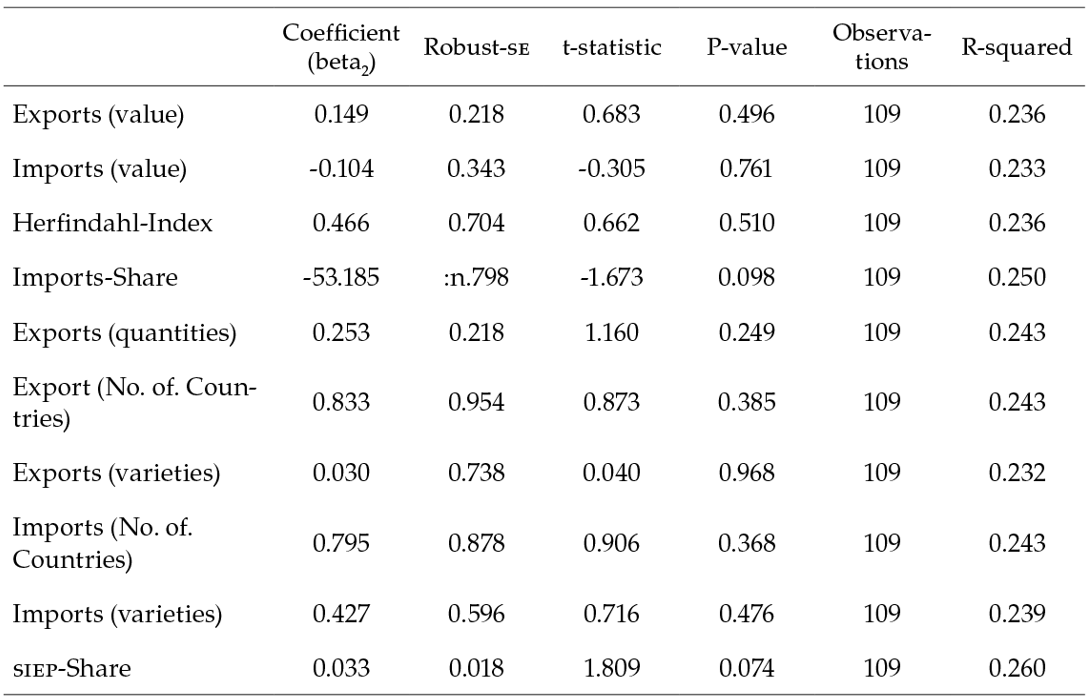

The second concern is reverse causality because some industries or particular firms might be more likely to lobby for lower input tariffs. The empirical approach could run into serious causality issues if policy makers lower tariffs based on sectoral trade performance. Higher tariff reduction might be granted for sectors with the best performance on export markets, sectors that require large amounts of imported goods or use siep scheme intensively. As a test of the exogeneity of input tariffs, it was examined the correlation of tariff changes with initial industry performance, following Bas and Strauss-Kahn (2015), Goldberg et al. (2010), and Topalova and Khandelwal (2011).

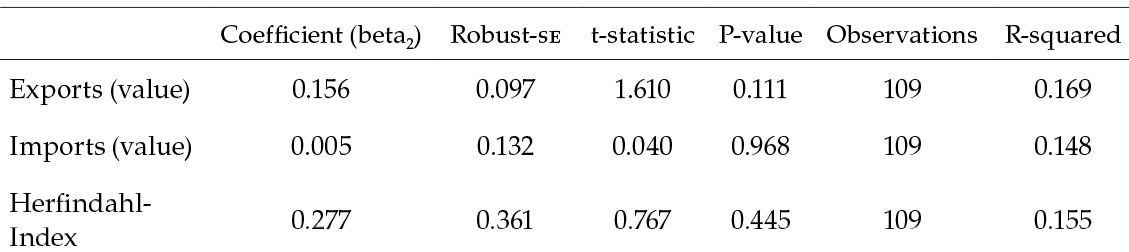

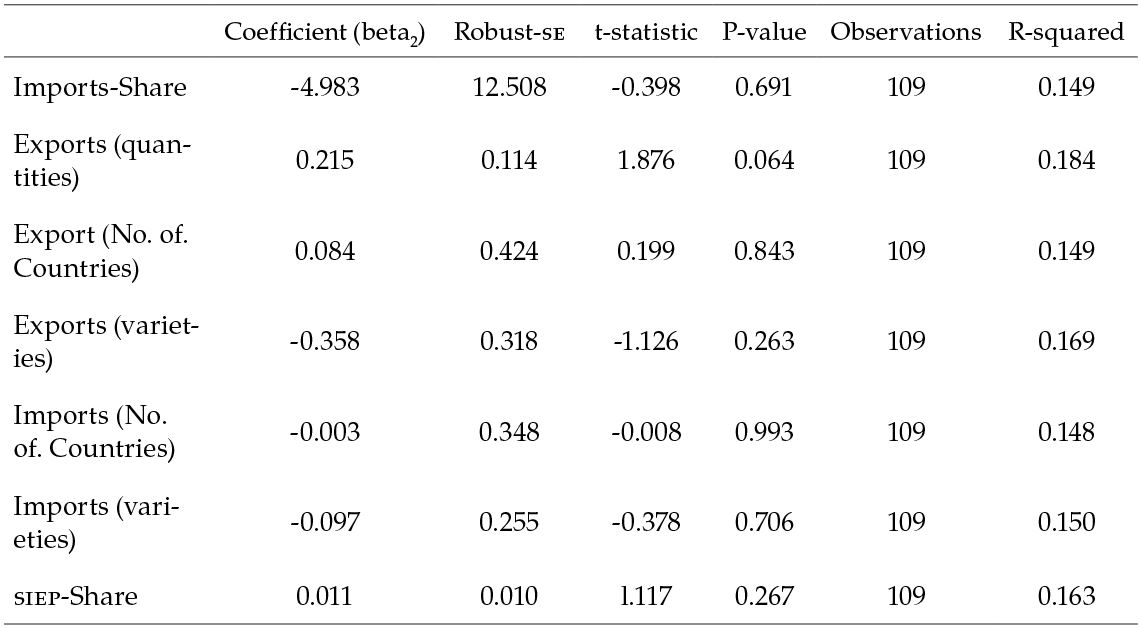

Data for 2011 is used to capture initial sectoral performances, and changes in import tariffs are regressed on several industry characteristics (at 4-digit-isic industries) computed as the weighted average (by trade value) of manufacturing exporting firms’ attributes for the first year. I test for changes in tariffs at the industry level between 2011 and 2019 (), using equation 5:

(5)

(5)Industry characteristics measured in 2011 include exports (in value and quantities), number of varieties exported and imported, number of countries to which it exports and from which it imports, imports (in value and share), an export-based Herfindahl index measuring industry concentration, and the percentage of exports using the siep scheme (siep-Share). Table 8 shows the coefficients on these initial industry characteristics (in 2011) from industrylevel regressions of tariff changes on these sectoral variables and 2-digit industry fixed effects (λs). There is no statistically significant correlation between the industry’s initial characteristics and the tariff decline. This is consistent with an exogenous input tariff reduction. In other words, if the government and trade agreement negotiators had targeted specific firms or industries via trade policies, it would be expected tariff changes correlate with initial sectoral performance. In addition, since the import duty rate also encompasses vat payments, the exogeneity test is also performed on the total duty rate (tariffs + vat) that is included in the empirical strategy. Results indicate no significant correlation between initial sectoral characteristics and changes in the import duties paid (see Appendix E).

Finally, in order to ensure that results are not driven by the tariff specification, measured as the effectively applied tariff estimated through the imports customs database, I propose an alternative test using statutory tariffs that come from the National Planning Department at the product level (HS10) by year, which follow the evolution and magnitude of mfn tariffs closely. As will be mentioned in section 8, there is a discrepancy between statutory (de facto) tariffs and actual applied tariff rates due mostly to the ftas and ptas. For simplicity, it is assumed that the measured vat rate remains unchanged. Now, the DutyRatef, t is computed as ∑pτf, p, t × ωf, p, t0, where τf, p, t is the sum of the statutory tariff and vat rate paid by the firm f for a specific product p at year t; and ωf, p, t0 corresponds to the initial (constant) weights of each imported product (HS10). It is important to note that, despite this new tariff measure does not consider the tariff cut associated with trade agreements since it does not distinguish where imports come from, it does allow us to isolate differences between firms when choosing where to source their imported inputs. Results are reported in column (8) of Table 7, suggesting that the findings are relatively robust to this alternative measure of tariffs.

8. Fiscal Cost of the Program

Since the duty drawback policy allows producers to request duty exemptions on imported products used for manufacturing exported goods, it is determinant to know the magnitude of the exemptions from the tariffs and the vat to know their fiscal cost. Over the last 25 years, the relative size of the loss has changed, with the share accounted for tariff exemptions falling as a result of a policy of general reduction in import tariffs and reductions tied to trade agreements (ftas and ptas) with different regions and countries, such as Mexico (since 1995), Mercosur (2005), the United States (2012), the European Union (2013), and Korea and Costa Rica (2016), among others. The source for calculating the losses is the customs database for imports, which has information for each good at the HS10 level on the value of duties paid for tariff and vat and the cif value of imports in pesos.

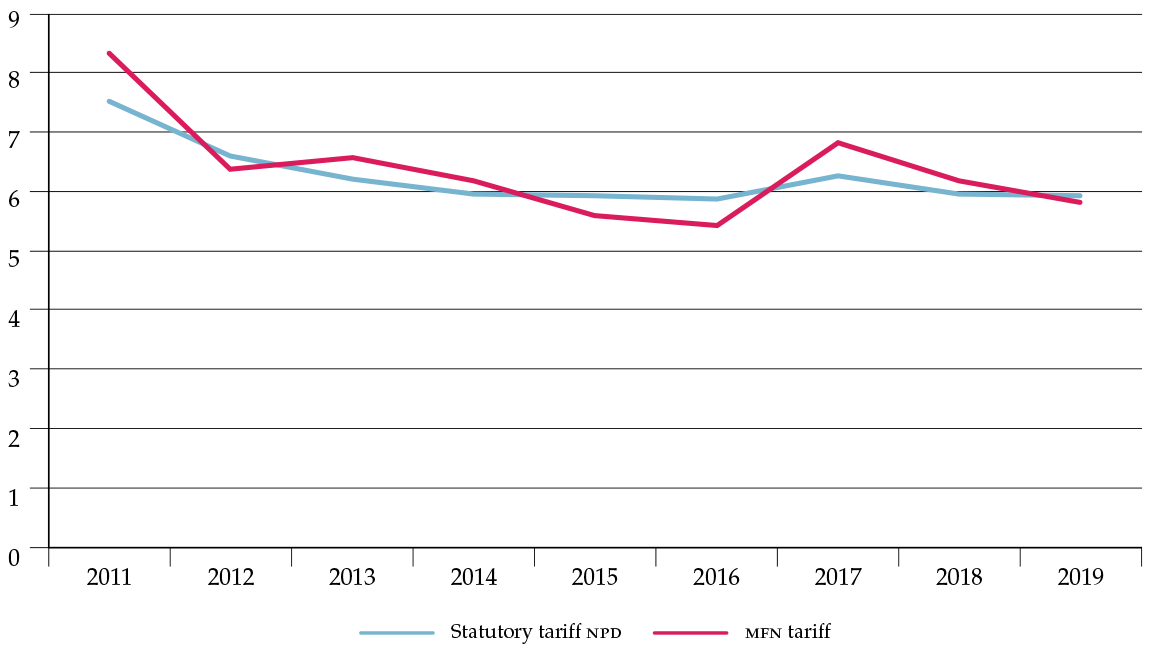

The evolution of tariffs for the last ten years is shown in Figure 8. Figure 8a shows the statutory tariffs (in solid lines) and actual (effective) tariff collection rates (in dashed lines) for capital and intermediate goods between 2011 and 2019.10 The former comes from the National Planning Department (npd) and is available yearly at the product level (HS10).11 In practice, these statutory tariffs are what Colombia promises to impose on imports from the rest of the world and closely follow the Most-Favored Nation tariffs (see Appendix F). On the contrary, the actual effective tariff rates, estimated using the imports customs database, are also disaggregated at 10-digit by year, excluding imports channeled through the siep regime.12 In contrast to the statutory tariffs, the effective rates consider the preferential agreements associated with free-trade areas or customs unions.