Essential and Orphan Drugs in Panama: Perception of Competition and Implications of Pricing Policy*

Medicamentos esenciales y huérfanos en Panamá: percepción de la competencia e implicaciones de la política de precios

Medicamentos essenciais e órfãos no Panamá: percepção da concorrência e implicações da política de preços

Essential and Orphan Drugs in Panama: Perception of Competition and Implications of Pricing Policy*

Revista de Economía del Rosario, vol. 23, no. 2, 2020

Universidad del Rosario

Received: 28 october 2019

Accepted: 10 february 2020

Additional information

To quote this article:: Herrera Ballesteros, V. H., Moreno Velásquez, I., Conte, E. I., Hall, C. N., & Gómez, B. (2020). Essential and Orphan Drugs in Panama: Perception of Competition and Implications of Pricing Policy. Revista de Economía del Rosario, 23(2), 1-20. https://doi.org/10.12804/revistas.urosario.edu.co/economia/a.9179

Abstract:

We measured the perception of competition in the market for essential and orphan drugs. The inflation rate for original products was 0.002 annually, whereas that for generic drugs was 0.005. The province of Panama, containing 46.5 % of private pharmacies, has the lowest index in the perception of competition; 18 % of the respondents to the out-ofpocket expenditure survey did not have drugs available, and 55 % could not afford them. The Gini coefficients were 0.40 (2014) and 0.76 (2017). The increase in prices, the relative independence of retailers to establish prices, and low access to social/private insurance increase the out-of-pocket expenses. JEL classification: H5 National Government Expenditures and Related Policies: H51, H53, H55.

Keywords: Economic competition, generic drug policy, orphan drug, pharmacy, therapeutic equivalency.

Resumen:

Medimos la percepción de competencia en el mercado de medicamentos esenciales y huérfanos. La tasa de inflación de los productos originales fue de 0.002 anuales, mientras que la de los medicamentos genéricos fue de 0.005. La provincia de Panamá, que contiene el 46.5 % de las farmacias privadas, tiene el índice más bajo en la percepción de competencia. El 18 % de los encuestados en la encuesta de gastos de bolsillo no tenía medicamentos disponibles y el 55 % no podía pagarlos. Los coeficientes de Gini fueron 0.40 (2014) y 0.76 (2017). El aumento de los precios, la relativa independencia de los minoristas para establecer los precios y el bajo acceso al seguro social/privado aumentan los gastos de bolsillo. Clasificación JEL: H5 National Government Expenditures and Related Policies: H51, H53, H55.

Palabras clave: competencia económica, política de medicamentos genéricos, medicamentos huérfanos, farmacia, equivalencia terapéutica.

Resumo:

Medimos a percepção de concorrência no mercado de medicamentos essenciais e órfãos. A taxa de inflação dos produtos originais foi de 0.002 anuais, enquanto a dos medicamentos genéricos foi de 0.005. A província do Panamá, que contém o 46.5 % das farmácias privadas, tem o índice mais baixo na percepção de concorrência. O 18 % dos inqueridos na enquete de despesas de bolso não tinha medicamentos disponíveis e o 55 % não podia pagá-los. Os coeficientes de Gini foram 0.40 (2014) e 0.76 (2017). O aumento dos preços, a relativa independência dos retalhistas para estabelecer os preços e o baixo acesso à segurança social / privada aumentam as despesas de bolso. Classificação JEL: H5 National Government Expenditures and Related Policies: H51, H53, H55.

Palavras-chave: concorrência económica, política de medicamentos genéricos, medicamentos órfãos, farmácia, equivalência terapêutica.

Introduction

The upward price increase in both generic and original products after the release of cap prices in 2004, whereby the market was left to free supply and demand, has left reasonable doubts as to the effectiveness of this measure. So the importance of addressing this problem goes beyond the structural characteristics of the Panamanian market, making it necessary to investigate aspects related to the conduct of economic operators along the marketing channel, as well as how the perceived competition environment, in addition to the degree of independent pricing in the retail segment.

Concerning orphan drugs sold in hospitals in general, there is no clear idea of whether there are policies regarding the management of lists in pharmacies, distributor companies, and manufacturers. These drugs are essential for the treatment of rare diseases. This aspect has been a great conflict between patients and the public health system in Panama, and even in other countries of the Americas, regarding their supply.

Given these facts, it is necessary to carry out a comprehensive analysis of public policies, regarding the functioning of the drug market, in the context of social inefficiency. Panama is one of the countries of the Americas with one of the worst distributions, drug supply problems, and access to out-of-pocket spending in the private sector, which is a complex problem to consider in the forthcoming reform of the public health and social security system, under a model common to that of many countries in the Americas, such as Chile, which makes it necessary to open up the debate on national drug policy in the current circumstances.

While there are publications on the drug market in different parts of the world, they do not generally address certain particular aspects of countries that, as in the case of Panama, are importers of medicines, and small economies such as those of Central America, which share common realities in the face of this problem. In general, many countries in the Americas continue to face health services’ inequality in the health sector; alternatives to this problem have been sought, focused on comprehensive reforms supported by international organisations such as the World Bank, the World Health Organization (who) or Pan American Health Organization (PAho) (Vargas et al., 2008).

Drug marketing is complicated due to its implications for social equity in health and its strong influence on the budgets of public health systems (Abdel Rida & Ibrahim, 2018; Martín-Conde, Tévar Alfonso, & García García, 2011; Gorgas, 2014). Since 2004, Panama has had a policy of prices established for free supply and demand in the medicines market, in which it is expected that generic medicines will generate greater price competition than innovative medicines (Gorgas, 2014).

The use of this competitive scheme continues to generate debate, regarding its efficacy for prices and medications’ access, particularly for those living in low-income regions, in which the approaches of market regulation and competition policy are contrasted under imperfect market structures (Lobo, 2014; Oliva, 2015). Furthermore, the current situation with orphan drugs is challeging; the low incidence of rare diseases results in very high prices in the private market, increasing the budget pressures on the public health systems. In general, orphan drugs are for hospital use, they acquire them directly from the distributors for their internal use, and few of these medications are sold directly to the public.

Panama has not escaped from this reality, and in the last three decades, the country has followed a scheme that has shifted from regulated prices to, in 2004, prices set for free supply and demand. In 1969, a system of price regulation, by means of the Decree No. 60, was launched, and it ended with the Law 29 of 1996 (repealed by Law 45 of 2007), moving to a system of regulation by exception when merited by the specific case (Asamblea Nacional de Panamá, 1969, 1996, 2007). Law 1 of 2001 established the previous and subsequent control of medicines as well as the bioequivalence, surveillance, and safety of medicines (Ley 1 de Medicamentos, 2001). Its article 102 established a price ceiling system for two years, leaving only the obligation of communicating increases by distributors as well as manufacturers, this mechanism ended in 2004, when Panama moved to a system of prices with free supply and demand. However, the main problem in the marketing of medicines to both the public and private sectors is exclusive distribution agreements between manufacturing laboratories and authorized distributors that do not allow the use of the parallel import mechanism established in Law 1, which would provide an alternative for import at lower prices. Meanwhile, the free trade agreements of medicines, especially those with developed countries, have been limited to the protection of intellectual property without technology transfer, which is an important issue to raise in most developing countries (Gamba, 2017).

This debate is highlighted by the escalating prices in recent years, which has had economic and social impacts on public and out-of-pocket expenditures on health (Herrera-Ballesteros, Castro & Gómez, 2018). In Panama, little is known about the functioning and organization of the medicine market and the competitive environment. Panama is characterized as an importer of most medications and currently has two complex public systems for purchase, the Ministry of Health and the Panamanian Social Security Institution, that act separately. Nevertheless, the private sector establishes the prices. At the time of the study, there were nine manufacturing plants in Panama producing generic medicines at a low scale. Overall, Panama imports most of its medicines and is dominated by the distribution segment.

As shown in a study of 2011 conducted by Diego Petrecolla, Panama had a moderate degree of concentration, based on a Herfindahl-Hirschmann index of 932 for the five largest distributors and a C4 index of 56 % for the market share of the four main distributors. In accordance with the Panamanian guidelines for the analysis of vertical behaviours, a C4 index equal to or above 60 is considered a relevant collective market power, and, in this case, we can conceive it likely to capture an oligopoly structure in addition to allowing control of prices. Examining other countries of Central America, the C4 index is 85 % in Costa Rica and 67 % in Nicaragua (Resolución A-30, 2009; Petrecolla, 2011; Shy, 1995). The retail segment for drugs consists of a large chain of pharmacies (N = 152), a small chain of pharmacies (N = 107), and community pharmacies or independent pharmacies (N = 439) (Ministerio de Salud, 2016). There are drugs for hospital use and those sold in the community. Overall, the private market sales the drugs, and patients can purchase medicines in community pharmacies and hospital pharmacies. Distributors do not have pharmacies because vertical integration is prohibited in Panama. Nevertheless, there are pharmacy chains, some of which belong to the main supermarket chains in the country and have greater market control over independent pharmacies.

We aim to measure the perception of competition and the population’s access in the market to essential and orphan drugs in Panama under the current context of a pricing policy based on free competition. The data were obtained from three surveys: the market for essential medicines and orphans to collect perceptions, of 8.5 % (N = 59) from private pharmacies, 12 % (N = 17) of distributors, and nine existing laboratories; the 2014 and 2017 Out-of-Pocket Essential Drug Surveys (N = 2721), and, finally, the Basic Drug Basket Database (CABAMED N = 50 Private Pharmacies). The monthly price increase was calculated by linear regression. The competitive perception index was calculated using factor analysis, and the Gini coefficients were estimated for 2014 and 2017.

The main findings of this research include that the average annual price increase for original products was 2.4 %, and for generics, 6 %. In general, economic operators (laboratories, distributors, and retailers) agree that the overall price increase was 5 %, and the principal cause was the increment in the price of the raw material. For distributors and laboratories, they generally do not have lists of orphan drugs as well as in pharmacies, so they still have no clear idea of the market situation for these medicines; 85 % of retailers, 64.7 % of distributors, and 55.5 % of laboratories consider the market competitive.

However, in the province of Panama, despite having 46.5 % of private pharmacies, the lowest perception rate of competition was obtained with 1.7971, with the overall index being 22751. Concerning out-of-pocket expenditure on medicines, by 2017, 55 % of respondents reported not having sufficient resources to buy their medicines, while the Gini ratio rose from 0.40 to 0.76 between 2014 and 2017 compared to that survey. These results make clear the problem of access to medicines and highlight the need to revise the pricing policy in addition to the rest of the regulations in this area.

This analysis has been organised into four sections, namely: materials and methods that address sources of information and statistical analysis; the results, which describe the main findings; the discussion, in which the results are contrasted with the most recent scientific evidence, and, finally, the conclusions, which put the results in context against the current environment.

Materials and Methods

Given the integrity of the proposed analysis, we combined the elements of competition policy such as the analysis of the structure, conduct, and performance of economic operators; the evolution of prices, and the condition of population’s access to out-of-pocket expenditure to construct the perception of competition rate based on the criteria affecting price determination, the construction of price indices of generic and original or brand-branded medicines, in addition to the Gini coefficients, with the 2014 and 2017 out-of-pocket surveys to analyse how the social gap has evolved, among other aspects.

We utilised data from three sources. The survey of the market of essential and orphan drugs was performed in the capitals of Panama’s ten provinces in 2016 (Ministerio de Salud, 2016). Out of the 698 private pharmacies existing in the country in 2016, 59 private pharmacies were randomly chosen at the national level. A survey was performed in each establishment by direct interview. A total of 140 distributors were registered in the country, and of those, 17 were chosen by simple random sampling selected in consensus with a panel of experts considering the principal distributors and to the widest medicines marketed variety.

Regarding the laboratories, the existing nine were selected, of which five are national. The survey was sent to the laboratories via email. The same survey was administered to the pharmacies, the laboratories, and the distributors. The questionnaire was composed of 21 questions and included three variables: 1) the criteria to determine prices —for instance, does the price truly correspond to the product? Is the price established independently? Is the price suggested by the distributor, the manufacturer, or their headquarters? Is the price fixed according to the environment’s competitiveness?—; 2) the characteristics of the business —e.g., the company’s years of operation, the number of employees, incentive policies for sales or handling of orphan products—, and 3) the perception of competition —e.g., trends for prices in the last six months, the percentage increase in perceived competition in the market rated as competitive, very competitive, or uncompetitive—.

The second source of information is the survey of out-of-pocket expenditures performed in 2014 and 2017. Briefly, the aim of the survey was to measure access to and availability of medicines and their rational use. The study population was composed of 2721 individuals aged 18 years or more who were the head of the family randomly selected from urban, rural, and indigenous areas and distributed across six districts: Panama and San Miguelito (province of Panama), Colon (Colon Province), David (Chiriquí Province) and the indigenous areas of Madungandí and Besikó (Gorgas, 2014; 2017). This study was conducted by the Gorgas Memorial Institute for Health Studies and the Ministry of Health.

The third source of information is data from the monthly price index of essential drugs, derived from the essential drugs list —CABAMED— (Resolución A-30). Cabamed was elaborated using 40 generic products and their corresponding originals. The survey was performed in the District of Panama and included a total of 50 private pharmacies. This survey was carried out by the Authority of Consumer Protection and Defence of Competition (Autoridad de Protección al Consumidor y Defensa de la Competencia, 2015-2019).

Statistical Analysis

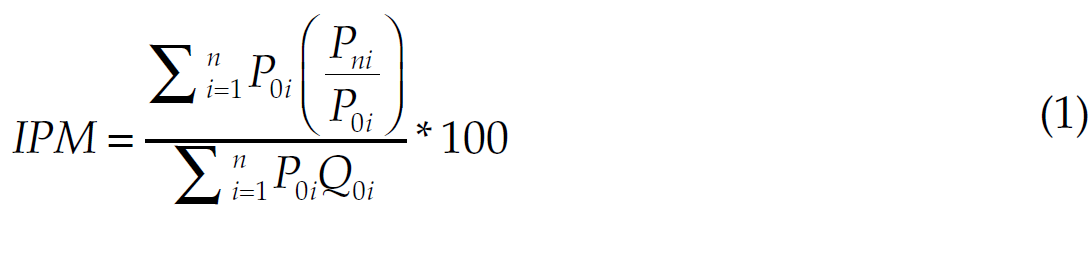

Three indicators were developed for the analysis. The first indicator was the average inflation rate from the monthly price index of the Cabamed, calculated using the Laspeyres formula (Gujarati, Guerrero, & Medina, 2004). The time frame analysed was from October 2014 to October 2015. It is a weighted index considering August 2013 as the base month and calculated for both the original reference (innovators) products and generic products (See equation 1). This indicator allows us to observe the recent price behaviour of the medicines and contextualize the perception of competition.

(1)

(1)where

P0i = Average price during the base period of product “i”.

Pni = Current average price of product “i”

Q0i = Quantity of the base period used for product “i”, depending on the type of treatment.

The inflation rate was estimated with a semi-logarithmic function, as shown in equation 2.

(2)

(2)lnipm is the natural logarithm of the price index of medicines, t is the linear trend of the time series of real numbers, ranked sequentially from 1 to the nth observation (n = 13), and, finally, u is the stochastic error term (Gujarati, 2009). Mathematically, it can be demonstrated that the derivative of lnipm with respect to t is β, the rate of inflation, as shown in equations 3 and 4.

(3)

(3)

(4)

(4)The second indicator is the index of perception of competition in private pharmacies. As the data obtained from the laboratories and distributors encompassed a small sample size, the indicator could not be estimated due to the small sample, particularly the Keyser-Meyer-Olkin.

Therefore, to complement our statistical analysis, we performed a descriptive analysis. Thus, we performed a factor analysis of the principal components with a polychoric correlations matrix (Mangin & Varela-Mallou, 1991). The variables used were “Perception of competition in the market” categorized as 1) very competitive, 2) new strategies, 3) uncompetitive, and 4) bureaucratic bundle; “Price suggested by the Distributor” categorized as 1) yes, 2) no, and 3) do not know; “Percentage rise in prices” categorized as 1) up to 5 %, 2) between 6 % and 10 %, 3) between 11 % and 20 %, and 4) more than 21 %, and “Criteria for establishing the price” categorized as 1) considers the competition, 2) is the price that corresponds to the product, and 3) both.

Because we have politomic variables, a polychoric correlation matrix was first constructed, and then a principal component analysis was performed with two factors at the maximum. The first principal component was utilized. We estimated the index for every pharmacy by means of linear regression models and obtained a national and per province average indicator. Because factor 1 is a latent variable, we named it “perception of competition in the segment index retail” (pcSIr). The analysis of the pcSIr will be supplemented with the results of the surveys of distributors and laboratories.

The third indicator is the Gini coefficient, which is calculated based on the individual incomes of participants in the survey of out-of-pocket expenditures in 2014 and 2017. This indicator estimates the social gap and, complemented by the Lorenz curve, will contextualize social inequality in relation to economic access to the purchase of medicines under the current free competition system (Sen, Foster, & Galindo, 2001).

All calculations were performed with the software Stata 14.0 (StataCorp LP).

Results

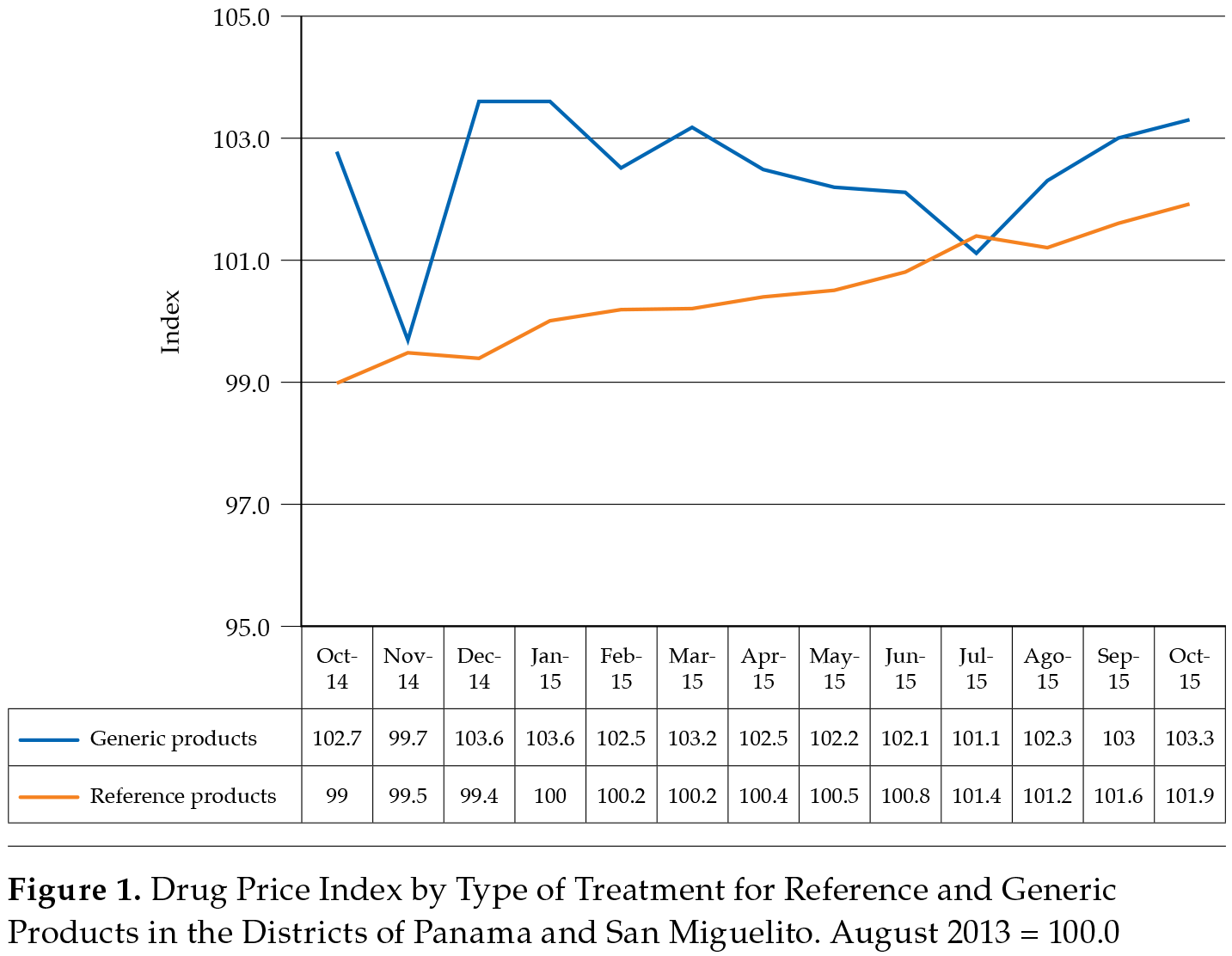

Price Index Based on Reference and Generic Drugs in the Districts of Panama and San Miguelito

The beta coefficient for the original products was 0.002 (t x 4.906, p < 0.05), with an average monthly increase per month of 0.2 % or 2.4 % per year. For generic products, the beta coefficient was 0.005 (t x 7.904, p < 0.05), which represents a monthly increase rate of 0.5 % or 6.0 % per year. Although generic products are relatively less expensive compared to the reference, they experienced a rapid increase based on changing trends in August 2015, as shown in figure 1 (Autoridad de Protección al Consumidor y Defensa de la Competencia, 2015-2019).

Index of Perception of Competitiveness in Pharmacies

According to the survey of the market of drugs, 85 % of the pharmacies responded that the market is very competitive, and 41 % perceived that prices had risen between 5 % and 36 % in the last six months. Of these establishments, 90 % perceived that prices had increased. The most frequent reason used to explain these increases was the rise in the cost of raw material —42 %— (Ministerio de Salud, 2016). Considering the criteria for establishing prices, only 20 % mentioned that the price is set based on prices at the surrounding pharmacies, and only 5 % said having a list of orphan drugs (Ministerio de Salud, 2016).

In relation to distributors, 11 of the 17 stated that the market is very competitive, 12 that prices were on the rise, seven that prices were rising by 5 %, and another 7 observed an increase from 6 % to 11 %. A total of 16 of the distributors mentioned that the cause was the cost of the raw material. However, 6 of the 17 stated that they had received recommendations to increase the price from the laboratories, and 15 of 17 expressed that the laboratories required them to respect the suggested price. Finally, only 4 of the 17 distributors described having a policy for managing orphan medicinal products (Ministerio de Salud, 2016).

With respect to the laboratories, all stated that the market was very competitive, and seven noted that prices had increased by 5 %. Similarly, eight stated that the reason for the increase was incremental cost increases in the raw material, and one explained that the increment was price inflation. Four of the nine laboratories mentioned that they instructed the distributors to raise prices, and only two described having the policy to manage orphan drugs (Ministerio de Salud, 2016). It is obvious that the price increases are aligned throughout the marketing channel.

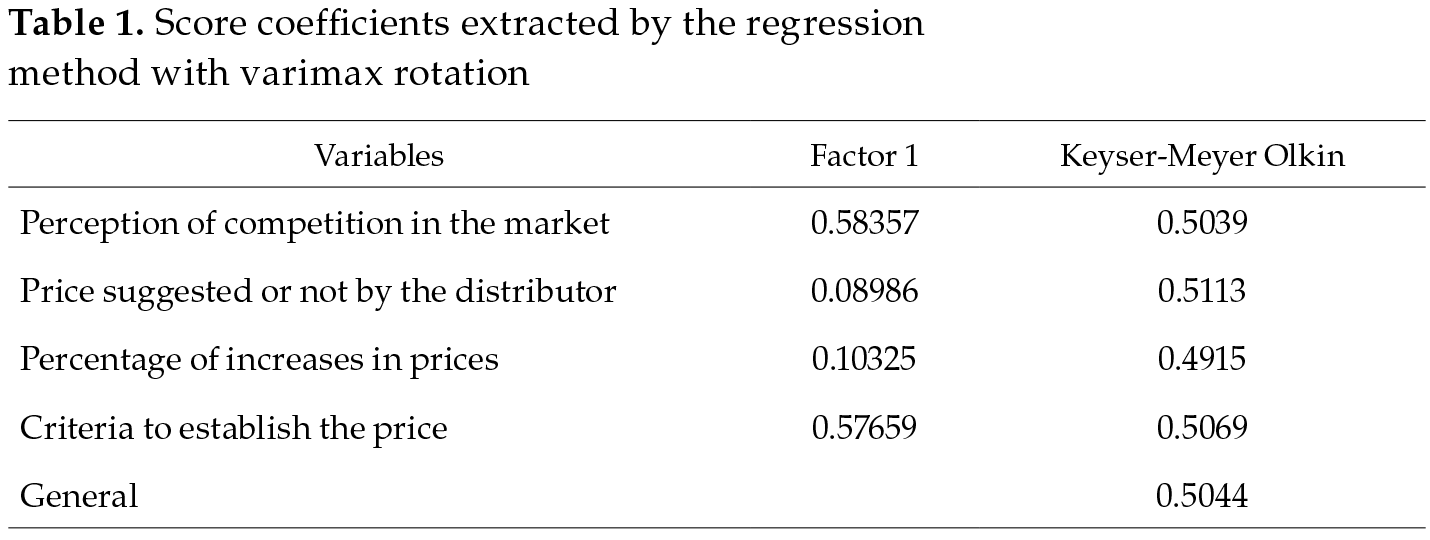

The calculations for the index of perception of competitiveness in pharmacies are presented in table 1. The reason for constructing a perception index was not to measure the degree of competition from a structural point of view, given that Diego Petrecolla’s study of 2010 is already available and that market structures rarely change in Panama, and it is a small market and an importer par excellence. In contrast, the index was constructed to measure the perception of the competitive environment and its possible relationship with the pricing decisions in the retail segment, in the sense of whether or not they truly have the freedom to establish prices, given that they represent the last link of the marketing chain and come into direct contact with the consumer. The variables with higher scores were perception of competition in the market (0.58357) and the criteria to establish the price (0.57659). The coefficient of Keyser-Meyer-Olkin global of 0.5044 is still within the minimum range of independence among factors (Ministerio de Salud, 2016).

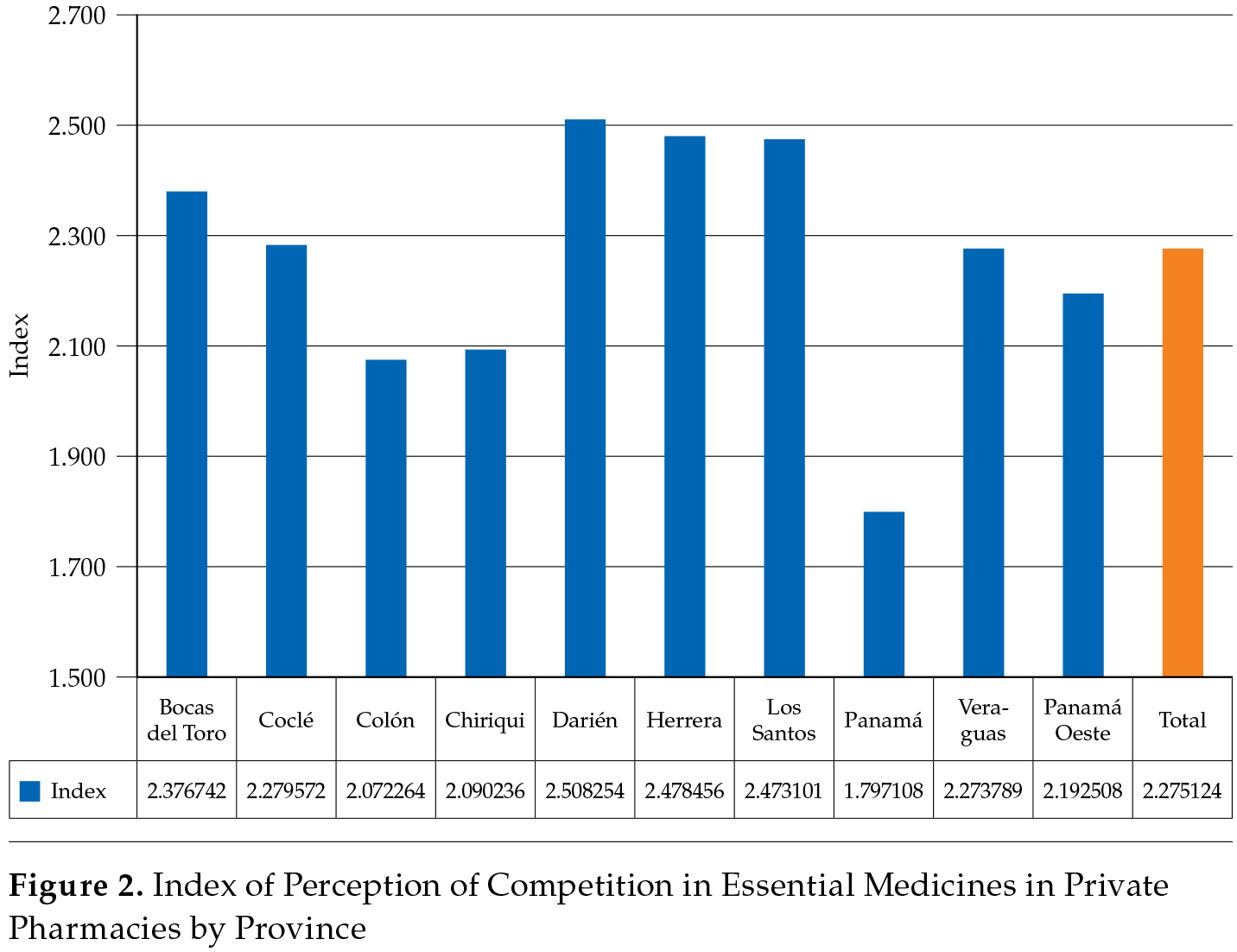

Figure 2 shows a graphical representation of the index estimates. The national average (total) was 2.2751, and we classify provinces according to a higher or lower perception of competition compared to the national average. The provinces with a more rural setting, such as Bocas del Toro, Darién, Herrera, and Los Santos, had a higher perception of competition compared to the remaining provinces with a more urban environment, especially Panama, which held 46.5 % of all establishments (Ministerio de Salud, 2016).

Social Gap and Gini Coefficient

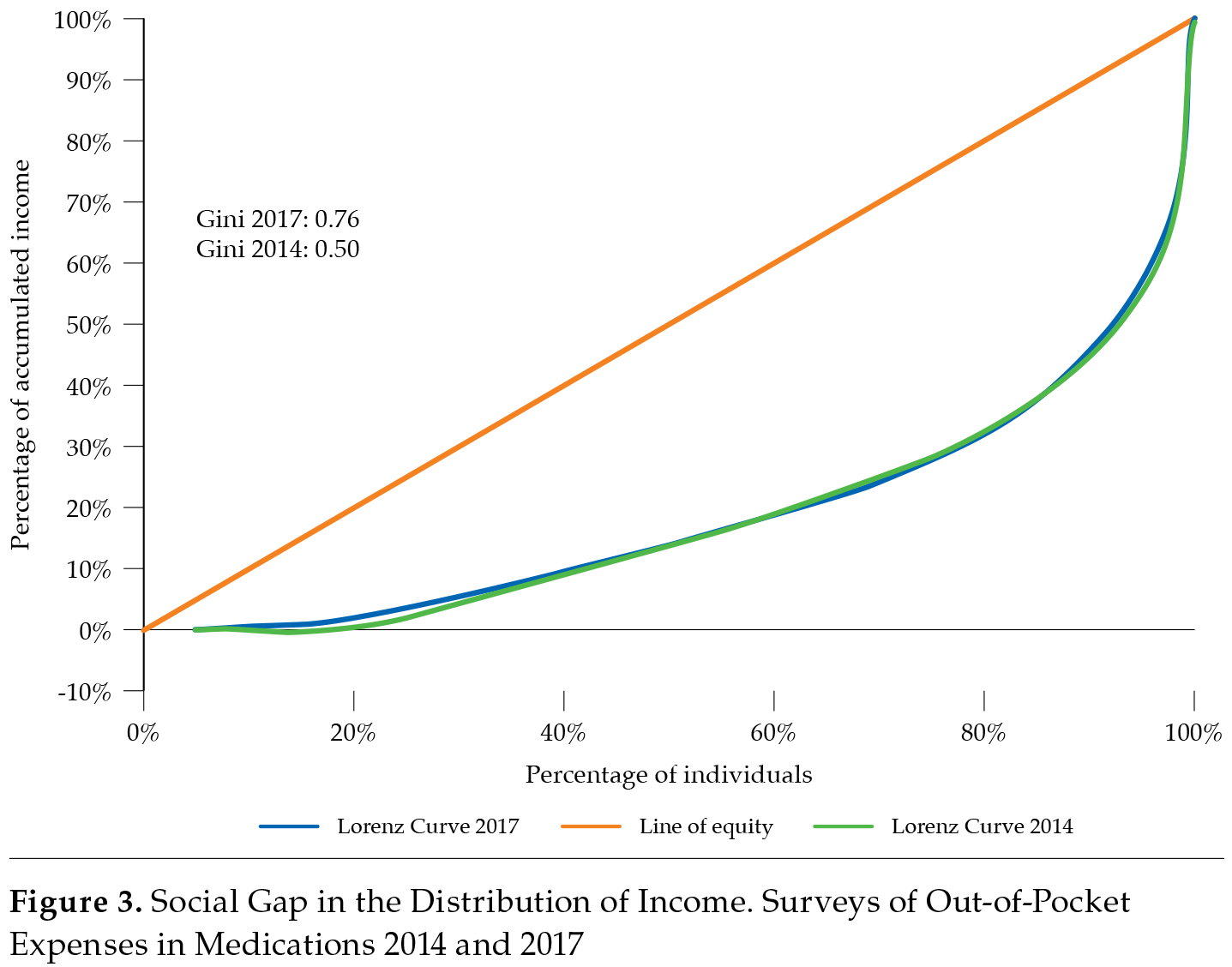

As shown in figure 3, the social gap has widened, as reflected in the Lorenz curves for 2014 and 2017. The Gini coefficient increased from 0.50 to 0.76 (Gorgas, 2014; 2017). Notably, according to the World Bank, the Gini coefficient was 0.51 in 2015 in Panama, suggesting that much of the population was excluded regarding access to medicines (Banco Mundial, 2014).

According to the results of both surveys, the annual average out-of-pocket expenditure was USD 86.25 in 2014 and USD 159.34 in 2017. In that same year, 46 % of the participants did not have social security, and 89 % did not have private insurance (Gorgas, 2017). According to the data from the National Institute of Statistics and Census (INEC) of Panama, informal employment in the country was 40.2 % in 2016, while it was 77.9 % in the Ngäbe-Buglé, an indigenous area (Censo, 2016).

In 2017, 18 % of the study participants mentioned that drugs were not available, whereas, in 2014, it was 16.5 %. In 2017, 28% bought medicines without a prescription, while in 2014, it was 21 %. In that same year, 17 % said they had to borrow to buy their drugs, while that number in 2014 was 15 %. Finally, in 2017, 55 % stated that drug prices were not affordable (Gorgas, 2014; 2017).

Discussion

These results make it clear that the decisions regarding the retail prices are influenced by the laboratories, manufacturers, and distributors. Therefore, the perception that the market is very competitive is contradictory in light of these results. This finding raises questions about the expected effect of the current pricing policy based on free supply and demand. However, despite studies of interchangeability between innovative and generic products, some mechanisms of Law 1 have not been applied, such as parallel imports. This might be due to agreements regarding commercial exclusivity and the pricing policies of economic agents (Caja de Seguro Social, 2012).

We would expect that where there is a higher density of establishments, there will be a stronger perception of competition. In principle, the “perception of competition” variable is neutralized by the variable “criteria to establish the price”, given that their scores are equivalent, making clear that retailers have little real independence to establish prices given the influence of chain pharmacies due to the oligopolistic structure of the latter, in that most are integrated into five major supermarket chains as well as into the segment of distributors and laboratories. This situation has had a negative impact on consumers, who have few options regarding prices. It also has generated access problems, particularly because Panama is among the countries in the Americas with the much unequal income distribution, as the Gini coefficient showed, which exacerbates the inequity with respect to out-of-pocket expenses. The results make clear the high social vulnerability with regard to the precarious nature of the labour market, which may lead many individuals to incur a social risk of catastrophic expenses, in addition to the distributive inequality demonstrated by the Gini coefficient.

Our findings suggest that despite a system of free competition in prices, the upward trend in prices contradicts the perceptions that the market is very competitive in Panama. Moreover, our results suggest that there are limitations in access to the consumer segment and increases in prices in recent years, as reflected in the price index of medicines with CABAMED data. Although, the market works under free competition in price, generic and innovative products have shown a trend of increased prices.

Regulation opposing competition policies sparks a controversial debate, particularly within the particularities of each country. Spain, for instance, has a much more strict regulatory policy compared to other European countries, and it proposes to encourage competition by lowering the prices of generic products, with funding and reimbursement schemes that require competitive bidding (Puig-Junoy, 2010). Spain aims to remove barriers to entry once the patent rights are ended; in the case of developing countries, these barriers become real obstacles to competition.

Even when 64 % of the pharmacies receive a bonus for minimum purchases of products, there is no evidence that such benefits are transferred to consumers, especially for generic products. Less well known is the situation of orphan drugs, whose use is restricted primarily to hospitals and in many cases requires subsidy and risk-sharing policies that are cost-effective (Drummond et al., 2007; Owen et al. 2008).

However, in some countries of the Americas region, such as in Colombia, the efficiency of the pharmaceutical sector is being refocused based on the design of the quality of the processes, which results in the benefit of competitiveness and reduces regulatory costs (García Aponte, Vallejo Díaz, & Mora Huertas, 2015). However, in a study for Peru, it is concluded that instead of establishing price controls, what should be promoted is more competition between generic and brand name drugs, so that the gap between both types is closed more of products, given the fact that there were no clear trends between international and local prices (Miranda, 2006).

In Panama, law 28 of 2014 protects individuals with rare diseases, defined as those whose prevalence is fewer than one person per every 2000. Due to the low prevalence, the cost of care can become excessive in many cases, as observed in European countries (Asamblea Nacional de Panamá, 2014; Picavet et al., 2011). One could argue that this type of medication should not follow the same general pricing schemes as other pharmaceuticals, especially in developing countries facing environments of imperfect competition (Simoens, 2011). This situation highlights the relationship between access to medicines and health equity. Policy interventions are needed, and price regulation should not be ruled out, generic products being the tip of the spear for this type of scheme (Ortún, 2008). Although our findings cannot demonstrate the performance of a practice that restricts competition, it is also not clear to what extent retailers are independent to establish their prices, especially in independent pharmacies.

Competition in prices in the segment retail is challenging. The presence of pharmacies within large chains, directly or indirectly, has an impact on the determination of prices at independent pharmacies, which depend on distributor provisioning systems. Panama is mainly an import country that established its national drug policy in 2009 to promote generic drugs and essential quality medicines under the system of free competition; however, the results of this policy are still controversial (A. N. D. l. R. D. Panamá, 2009; Gorgas, 2014; Ministerio de Salud, 2016; Gorgas, 2017). Similarly, its Law 1 of 2001 allows parallel import but has been affected by contracts of exclusivity and challenge from some European countries, given their almost imperceptible impact on prices in some products, such as Simvastatin (Costa-Font & Kanavos, 2007; Ley 1 de Medicamentos, 2001). In Panama, national laboratories do not play a role in fixing prices because they have a reduced market share and produce generic products only, while distributors control the market and have exclusive relationships with regard to foreign laboratories that hold the patents on innovative products.

Although between December 2014 and July 2015, the trend in the price index of generic drugs was decreasing, from August 2015, there was a cyclic trend upward for the original reference drugs. The increase in the cost of raw material was mainly the explanation given by the economic agents. However, the findings regarding the interference in pricing decisions in the retail segment and other distortions of the market raise the question of whether other potential explanations are involved in this situation. Our findings also highlight the effectiveness of the current pricing policy based on competition with generic products and suggest a prompt review of the current trends in the market (Abdel Rida & Ibrahim, 2018; Degtiar, 2017).

Panama has a scarce national industry and is import-dependent, and thus, the conditions of competition are determined outside its borders. Moreover, the country is subject to price discrimination policies from the pharmaceutical industry, given that it is considered a medium-high income country (World Bank, 2017). Similarly, there has been little or no transfer of technology to developed countries, making it difficult for Panama to manufacture costeffective generic products. Controls given to the pharmaceutical companies of developed countries allow them to maintain control of investment in R&D in addition to determining prices under free trade agreements because large pharmaceutical companies seek to protect intellectual capital (Gamba, 2017; Lobo & Velásquez, 1997).

Currently, the benefits of free trade tend to be less extensive and limited to negotiating more specific items, such as the protection of property rights, ensuring the technological advantage for countries with highly developed pharmaceutical sectors (Van Norman & Eisenkot, 2017). Similarly, large multinational pharmaceutical firms establish different pricing strategies between countries and regions. Small and dependent countries that rely on imports, therefore, have few marketing mechanisms with regard to affordable prices, particularly for new products, such as those treating non-communicable diseases. The marketing of medicines based on the pharmaceutical industry strategies is complex and creates underlying inequalities at the social level and with access to drugs, which represents a challenge for the health sector in the face of important pricing policy.

Our study has strengths and limitations. Out-of-pocket surveys cannot be extrapolated to the national level; however, the results are similar to those of other studies in the context of social inequalities. Further, the scarcity of information collected regarding the handling of orphan drugs leaves us with only partial conclusions regarding the objective of this research.

To the best of our knowledge, this is the first comprehensive study in Panama that involves data from different sectors of the market of medicines. The findings provide a much broader picture of a slightly oligopolistic market structure that has been complemented by pricing mechanisms, and it also offers perceptions of the competition environment in terms of the prices of innovative and generic products in the three studied market segments.

Conclusions

Our study shows that drug prices increased in an aligned manner in the marketing channel. Although it does not show the performance of a monopolistic practice, it does not make clear the independence of retail pharmacies to establish competitive prices. Similarly, the high percentage of people without social and private insurance and the increase in out-of-pocket expenses aggravates social inequality. This highlights the need to review the current pricing policy and consider other regulatory mechanisms.

Agradecimientos

Our sincere thanks to all the staff of the Ministry of Health who participated in the infield surveys and to the Gorgas Memorial Institute for Health Studies. IMV is supported by the Sistema Nacional de Investigación (SNI), Senacyt, Panama.

References

Abdel Rida, N., & Ibrahim, M. I. M. (2018). Medicines pricing policy and strategies in developing countries: A review. In M. I. M. Ibrahim, Wertheimer, A. I., & Din Babar, Z. (Eds.), Social and administrative aspects of pharmacy in lowand middle-income countries (pp. 111-128). Academic Press. https://doi.org/10.1016/B978-0-12-811228-1.00007-8

Autoridad de Protección al Consumidor y Defensa de la Competencia. (2019) Canasta Básica de Medicamentos (Camabed). Retrieved from http://www.acodeco.gob.pa/acodeco/cabamed.php

Banco Mundial. (2014). Índice de Gini. Retrieved from http://datos.banco-mundial.org/indicador/SI.POV.GINI

Caja de Seguro Social. (2012). Listado oficial de medicamentos. Retrieved from http://www.css.gob.pa/Listado%20Oficial%20de%20Medicamentos%20-%202012.pdf

Costa-Font, J., & Kanavos, P. (2007). Competencia limitada en la importación paralela de medicamentos: el caso de la simvastatina en Alemania, Holanda y el Reino Unido. Gaceta Sanitaria, 21(1), 53-59. https://doi.org/10.1157/13099121

Degtiar, I. (2017). A review of international coverage and pricing strategies for personalized medicine and orphan drugs. Health Policy, 121(12), 1240-1248. https://doi.org/10.1016/j.healthpol.2017.09.005

Drummond, M. F., Wilson, D. A., Kanavos, P., Ubel, P., & Rovira, J. (2007). Assessing the economic challenges posed by orphan drugs. International Journal of Technology Assessment in Health Care, 23. https://doi.org/10.1017/s0266462307051550

Gamba, S. (2017). The effect of intellectual property rights on domestic innovation in the pharmaceutical sector. World Development, 99, 15-27. https://doi.org/10.1016/j.worlddev.2017.06.003

World Bank. (2017). Current classification by income. Retrieved from https://datahelpdesk.worldbank.org/knowledgebase/articles/906519-world-bank-country-and-lending-groups

García Aponte, O. F., Vallejo Díaz, B. M., & Mora Huertas, C. E. (2015). La calidad desde el diseño: principios y oportunidades para la industria farmacéutica. Estudios Gerenciales, 31(134), 68-78. https://doi.org/10.1016/j. estger.2014.09.005

Gorgas. (2014). Encuesta de gasto de bolsillo en medicamentos en los distritos de Panamá, San Miguelito, Colón, David y las Comarcas Indígenas de Madungandí y Ngäbe-Buglé. Retrieved from http://www.gorgas.gob.pa/SIGMED/documentos/GastoBolsilloMedicamentos_2014.pdf

Gorgas. (2017). Encuesta de gasto de bolsillo en medicamentos en los distritos de Panamá, San Miguelito, Colón y las comarcas indígenas de Madungandí y Ngäbe-Buglé. In Instituto Conmemorativo Gorgas de Estudios de la Salud (Ed.). Ciudad de Panamá.

Gujarati, D. N. (2009). Econometría. New York: McGraw Hill.

Gujarati, D. N., Guerrero, D. G., & Medina, G. A. (2004). Econometría. México: McGraw-Hill Interamericana.

Herrera-Ballesteros, V. H., Castro, F., & Gómez, B. (2018). Análisis de los determinantes socioeconómicos del gasto de bolsillo en medicamentos en seis zonas geográficas de Panamá. Value in Health Regional Issues, 17, 64-70. https://doi.org/10.1016/j.vhri.2017.12.005

Instituto Nacional de Estadística y Censo. (2016). Empleo informal en la república, por sector en el empleo, según sexo, provincia y comarca indígena: Encuesta de mercado laboral, agosto 2015-16. Retrieved from https://www.inec.gob.pa/archivos/P7851441-10.pdf

Lobo, F. (2014). Políticas actuales de precios de medicamentos en Europa: panorama general: Springer Healthcare Ibérica.

Lobo, F., & Velásquez, G. (1997). Los medicamentos ante las nuevas realidades económicas. Madrid: Civitas.

Mangin, J.-P., & Varela-Mallou, J. (Coords.). (2003). Análisis multivariante para las ciencias sociales. Barcelona: Pearson Education.

Martín-Conde, J. A., Tévar Alfonso, E., & García García, F. J. (2011). ¿Valen los medicamentos lo que cuestan? Farmacia Hospitalaria, 35 (Supplement 2), 32-39. https://doi.org/10.1016/S1130-6343(11)70020-4

Miranda, J. J. (2006). El mercado de medicamentos en el Perú: ¿libre o regulado? Consorcio de Investigación Económica y Social, cies, 2006. Lima: Instituto de Estudios Peruanos.

Ley 1 de Medicamentos y otros Productos para la Salud Humana. (2001).

Ley 94 Por la cual se crea el organismo especial denominado oficina de regulacion de precios y se derogan la ley 19 de 14 de febrero de 1952 y la ley 94 de 28 de diciembre de 1961. (1969).

Ley 29 de 1996 por la cual se dictan normas sobre la defensa de la competencia y se adoptan otras medidas. (1996).

Ley 45 Que dicta normas sobre proteccion al consumidor y defensa de la competencia y otra disposicion. (2007).

Ley 28 Que garantiza la proteccion social a la poblacion que padece enfermedades raras, poco frecuentes y huerfanas (2014).

Ministerio de Salud. (2016). Directorio de farmacias vigentes en la República de Panamá. Dirección Nacional de Farmacias y Drogas. Panamá.

Oliva, J. (2015). Análisis de la intervención de precios de los medicamentos en España y Europa: panorama de la regulación y los estudios empíricos. Gaceta Sanitaria, 29(4), 321.

Ortún, V. (2008). El impacto de los medicamentos en el bienestar. Informe sespas 2008. Gaceta Sanitaria, 22, 111-117. https://doi.org/10.1016/S0213-9111(08)76082-5

Owen, A., Spinks, J., Meehan, A., Robb, T., Hardy, M., Kwasha, D., … Reid, C. (2008). A new model to evaluate the long-term cost effectiveness of orphan and highly specialised drugs following listing on the Australian Pharmaceutical Benefits Scheme: the Bosentan Patient Registry. Journal of Medical Economics, 11(2), 235-243. https://doi.org/10.3111/13696990802034525

Petrecolla, D. (2011). Condiciones de competencia en el sector de medicamentos de Centroamérica. Retrieved from http://www.acodeco.gob.pa:8080/RECAC/InformeSectorMedicamentos_Enero2011.pdf

Picavet, E., Dooms, M., Cassiman, D., & Simoens, S. (2011). Drugs for rare diseases — orphan designation status influences price. Applied Health Economics and Health Policy, 9. https://doi.org/10.2165/11590170-000000000-00000

Puig-Junoy, J. (2010). Políticas de fomento de la competencia en precios en el mercado de genéricos: lecciones de la experiencia europea. Gaceta Sanitaria, 24(3), 193-199. https://doi.org/10.1016/j.gaceta.2009.12.003

Resolución A-30. Guía para el análisis de conductas verticales, C.F.R. (2009). Retrieved from https://www.gacetaoficial.gob.pa/pdfTemp/26349/20113.pdf

Resolucion 632 por medio de la cual se adopta la politica nacional de medicamentos (2009).

Sen, A. K., Foster, J. E. A., & Galindo, E. L. S. (2001). La desigualdad económica. México: Fondo de Cultura Económica.

Shy, O. (1995). Industrial organization: Theory and applications. Cambridge:

Notes

* The authors declare no ethical or economic conflicts of interest. This research was covered by the public research fund of the Gorgas Memorial Institute of Health Studies.