Fiscal Multipliers and Balance Sheet Effects in a Small Open Economy

Multiplicadores fiscales y efectos de hoja de balance en una economía pequeña y abierta

Multiplicadores fiscais e efeitos do balanço em uma economia pequena e aberta

Fiscal Multipliers and Balance Sheet Effects in a Small Open Economy

Revista de Economía del Rosario, vol. 23, no. 2, 2020

Universidad del Rosario

Received: 29 august 2019

Accepted: 07 february 2020

Additional information

To quote this article: López Piñeros, M. (2020). Fiscal Multipliers and Balance Sheet Effects in a Small Open Economy. Revista de Economía del Rosario, 23(2), 1-42. https://doi.org/10.12804/revistas.urosario.edu.co/economia/a.9178

Abstract:

Fiscal multipliers are different across countries and according to economic circumstances. Investment multipliers have recently been subjects of analysis, especially for advanced economies. For small open economies, such as Colombia, there is not much research in this regard, and there are no descriptions of the transmission mechanisms. In this paper, we present empirical evidence of the investment and output fiscal multipliers. Afterward, we present a set of models with financial frictions that describe the transmission mechanisms that explain the investment multipliers under different characteristics of the economy. The main results show that balance sheet effects with nominal contracts replicate the empirical findings of increase investment. The degree of openness of the economy and the level of country risk premium are essential mechanisms. JEL classification: D69, D91, E21, E22, E32, E44, E62.

Keywords: Fiscal multipliers, fiscal policy rules, non-Ricardian households, DSGE model, financial frictions, nominal contracts.

Resumen:

Los multiplicadores fiscales son diferentes según los países y las circunstancias económicas. Los multiplicadores de inversión han sido analizados más recientemente, especialmente para economías avanzadas. Para el caso de economías pequeñas y abiertas, como Colombia, no hay muchos estudios, así como tampoco se describen los mecanismos de transmisión. En este documento se presenta evidencia empírica de los multiplicadores del gasto y la inversión. Posteriormente, se presenta un conjunto de modelos con fricciones financieras que describen los mecanismos de transmisión que explican los multiplicadores de inversión considerando las principales características de la economía colombiana. Los resultados muestran que la evidencia empírica es mejor explicada por los efectos de hoja de balance con contratos nominales. El grado de apertura de la economía, así como los niveles de la prima de riesgo país son elementos esenciales. Clasificación JEL: D69, D91, E21, E22, E32, E44, E62.

Palabras clave: multiplicadores fiscales, reglas de política fiscal, agentes no-ricardianos, modelos DSGE, fricciones financieras, contratos nominales.

Resumo:

Os multiplicadores fiscais são diferentes de acordo com os países e as circunstâncias econômicas. Os multiplicadores do investimento têm sido analisados recentemente, mas particularmente para o caso de economias avançadas. No caso de economias pequenas e abertas como a Colômbia não há muita pesquisa ao respeito e os canais de transmissão não se têm discutido. Neste documento apresentamos evidência empírica dos multiplicadores fiscais do investimento e do produto. Subsequentemente, apresentamos um conjunto de modelos com rigidezes financeiras que descrevem os mecanismos de transmissão que explicam o multiplicador do investimento ante diferentes características da economia. Os principais resultados mostram que os efeitos do balanço são contratos nominais replicam a evidência empírica do incremento no investimento. O grau de abertura e o nível do prêmio de risco país desempenham um papel central no mecanismo. Classificação JEL: D69, D91, E21, E22, E32, E44, E62.

Palavras-chave: multiplicadores fiscais, regras de política fiscal, lares não-Ricardianos, modelos DSGE, fricções financeiras, contratos nominais.

Introduction

Advanced and emerging economies during 2007-2009 were affected by the worst financial crises since the Great Depression. As a response to the crises, governments have implemented different fiscal stimulus packages. One question arising from the fiscal policy implemented is how big the fiscal multipliers could be in a world with financial frictions. Some models, developed by Freedman et al. (2010), Fernández-Villaverde (2010), and Carrillo and Poilly (2013), among others, have focused their attention in advanced economies, closed economies, and the recent financial crises. In their closed economy models (CEM) for the United States, these authors have found that financial frictions combined with a Fisher effect cause the increases in investment due to balance sheet effects with the result of high fiscal multipliers.

We focus our attention in Colombia, a small open economy, because it is an emerging country that, during the late nineties, suffered a strong recession, due to significant balance sheet effects reinforced by the fact that the monetary authority tried to maintain the real exchange rate fixed. The shock originated in the Asian crises, and it also affected several other small open economies, which was the moment of a country risk premium increment that emerging economies had to pay, with the foreign-interest rate, for their foreign debt. More recently, like in many other small open economies, the country faced capital outflows that had important effects. The way to deal with the crises was, in part, by increasing government expenditure. How big is the output and investment’s fiscal multiplier in the context of economies that experience strong movements in the real exchange rates and capital inflows and outflows that are foreign interest rates takers, which call for a detailed study?

The goal of the paper is two-fold. First, we present empirical evidence for a small open economy, Colombia, on how big is the fiscal multiplier of output and investment? Second, we set up a DSGe model for a small open economy (soeM) that asses the question if the findings regarding investment by Fernández-Villaverde (2010) (fv from now on), and Carrillo and Poilly (2013) (cp for now on) still hold. More specifically, we want to analyze what is the role of the real exchange rate on a model with financial frictions and nominal contracts. What happens to investment in the case of a small open economy in the context of our model? What are the results depending on the degree of the country risk premium that faces the economy? Finally, as long as one feature of a soe is to be populated by non-Ricardian consumers, we analyze which is its interaction with the real exchange rate and their impact on the fiscal multipliers.

For these purposes, we present empirical evidence based mainly in Ramey’s (2011) methodology for the identification of the government spending shock. Second, we develop a fiscal DSGe model with balance sheet effects à la Bernanke, Gertler, and Gilchrist (1999) for a small open economy, characterized by the presence of non-Ricardian agents and nominal contracts. The model replicates the empirical evidence of an investment increment.

The model consists of 7 sectors. The household sector is divided into Ricardian and non-Ricardian agents. The entrepreneurial sector, which makes the investment decisions and faces a costly state verification problem giving rise to an external finance premium that depends on the balance sheet of the firm and, because contracts are nominal, it also depends on inflation. The third sector is the capital producers’ sector, which purchases consumption goods as material input, combines it with rented capital, and produces new capital. The fourth is the retailers’ sector that uses the wholesale output of entrepreneurs, differentiates it, and sets prices à la Calvo (1983). We also model a national agency in the labor market. There is also a description of the rest of the world’s sector. Finally, we have the government, which conducts monetary and fiscal policies. Fiscal policy is characterized by a public sector that collects income taxes and receipts revenues from oil production. Accordingly, this last sector follows a structural fiscal rule.

Our results are as follows. With respect to the empirical investigation, we found that the investment multiplier is positive, which means that there is not investment crowding out: is about 1% in impact and close to 2% in the fifth quarter. The fiscal consumption multiplier is also positive and close to the output fiscal multiplier of 1.2% in the third quarter.

From the model’s perspective, we first contrasted a model without the Fisher effect (no nominal contracts) with one with the Fisher effect. We analyzed the role of nominal contracts in the economy and found that if there is no Fisher effect, investment falls due to increases in real interest rates that cause a fall in the price of capital and net worth, and an increase in the external finance premium of the entrepreneurs. On the contrary, as in fv and cp, nominal contracts cause a lower external finance premium, an increase in investment, and higher output multipliers. Moreover, in the case of the model with the Fisher effect, the real exchange rate appreciates more due to the higher fiscal multipliers. In this case, the real interest rates are lower, which translates into a higher price of capital that causes an improvement in the external finance premium that, in turn, causes even higher increments in investment.

Then, we analyzed the case of a SOEM vs CEM —here a closed economy model refers to one were the imports share is lower in the consumers bundle than in a SOEM—. In this case, for the SOEM, there is an import-substitution effect that affects the total inflation rate causing higher interest rates and lower price of capital, which, in turn, causes lower investment than in the CEM, which in small open economies the fiscal multipliers of investment and output are lower than in closed economies. Here, the higher fiscal multipliers in the CEM cause higher real exchange rate appreciation reinforcing the balance sheet effects. With respect to the country risk premium, our findings show that the lower the country risk premium, the higher the fiscal multiplier of investment and output.

Finally, regarding the interaction between the presence of non-Ricardian agents and balance sheet effects, our results show that in the same way that in Galí, López-Salido, and Vallés (2007), and Monacelli and Perotti (2010), the fiscal multipliers are higher in the case of non-Ricardian consumers because of the increase in consumption of this agents. However, the increase in investment is not very different among the two models, and neither is the behavior of the real exchange rate or the balance sheets effects.

The remainder of this paper proceeds as follows: Section 1 presents the related literature. Section 2 presents the empirical evidence for the Colombian economy. Section 3 presents the model. Section 4 the calibration of the model. Section 5 discusses the results, and section 6 presents the conclusions.

1. Related Literature

Our results contribute to several strands of literature. First of all, they examine the effect of government spending on consumption and output; for example, Colciago (2011), Galí et al. (2007), and Monacelli and Perotti (2010), who intended to replicate the effect of government spending on consumption for advanced economies. However, as these papers do not include balance sheet effects, they tend to underestimate the impact of the fiscal multiplier, as we will show here. Our results also add to the literature that examines the output and fiscal consumption multipliers, using a DSGE model enriched with financial frictions (Sin, 2016; Castro et al., 2014). These papers are also meant to replicate stylized facts for small open economies. But they do not model the role of non-Ricardian agents in these kinds of economies and, therefore, their fiscal consumption multipliers tend to be very small, as we will show later in our study.

Our paper also relates to the strand of literature that studies fiscal stimulus and crowding out effects on investment under the presence of financial frictions (see, Freedman et al. (2010), Carrillo and Poilly (2013), and Fernández Villaverde (2010) for advanced economies). The first two focus on the fiscal stimulus during the recent financial recession of the United States, while the latter introduced the debt-deflation Fisher effect for nominal contracts in a CEM for the United States. In this regard, our contributions first analyzed the crowding out of the effect of the government spending on investment under the presence of financial frictions for small open economies and, second, examined the prediction of increases in investment in the case of nominal contracts but for the case of small open economies.

Another related literature deals with the Dutch disease phenomenon that affected several countries around the world during 2003-2013 due to the increase in commodity prices (García-Cicco & Kawamura, 2015; Fernández & Villar, 2014; Goda & Torres, 2015; Pieschacón, 2012; Sarmiento & López, 2016). One way to deal with this phenomenon has been the implementation of fiscal rules, and our theoretical model includes this characteristic in the Colombian economy.

2. Empirical Evidence

The empirical evidence about the effect of a fiscal expenditure shock on consumption and investment is escarse. Here, we add to the fiscal multipliers’ empirical literature that has found that consumption increases after a fiscal expenditure shock, and we present evidence on what happens to investment.

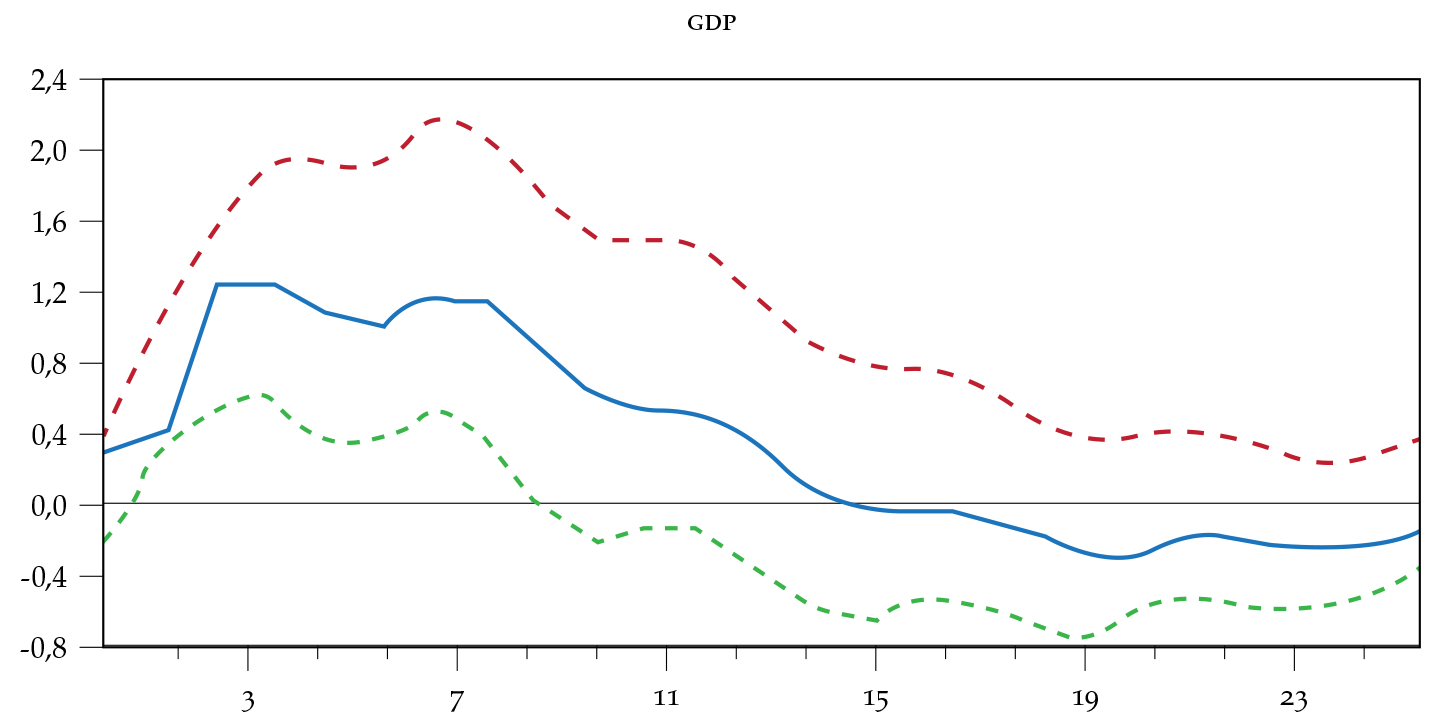

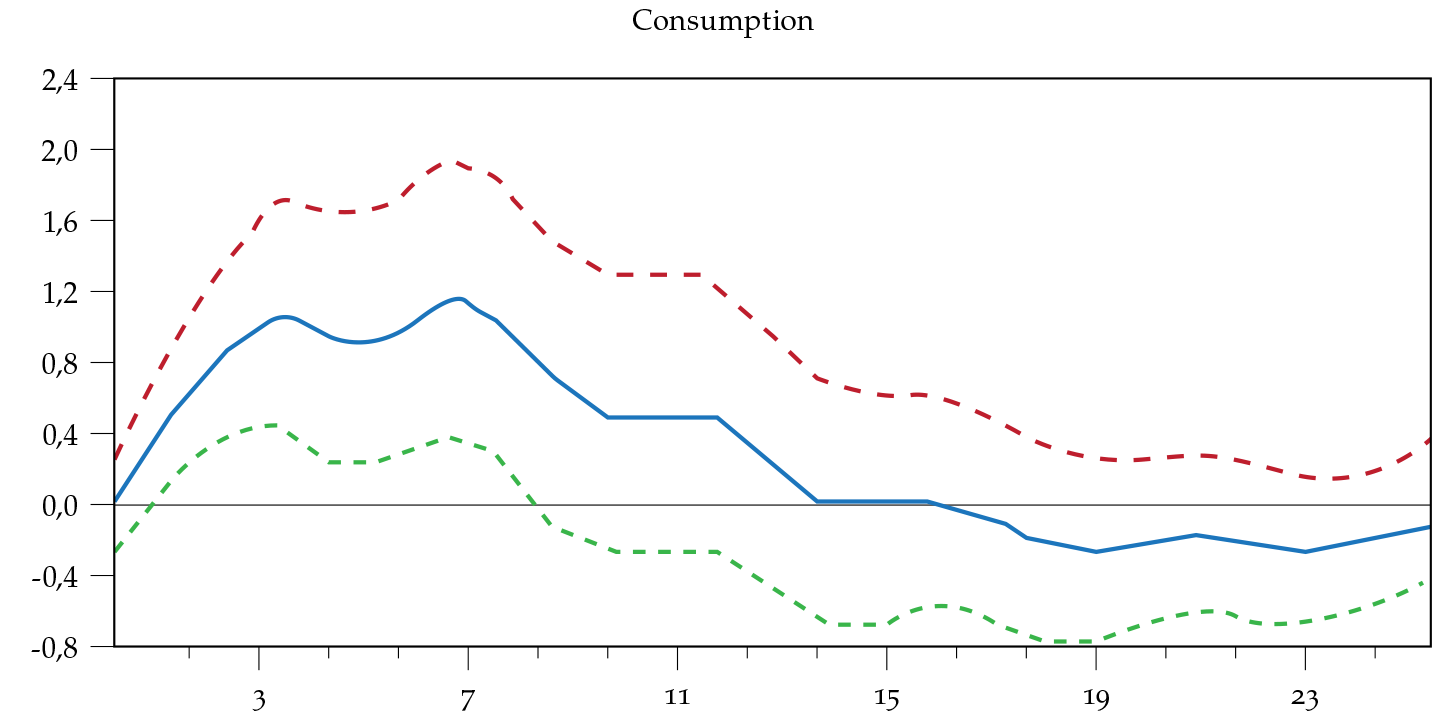

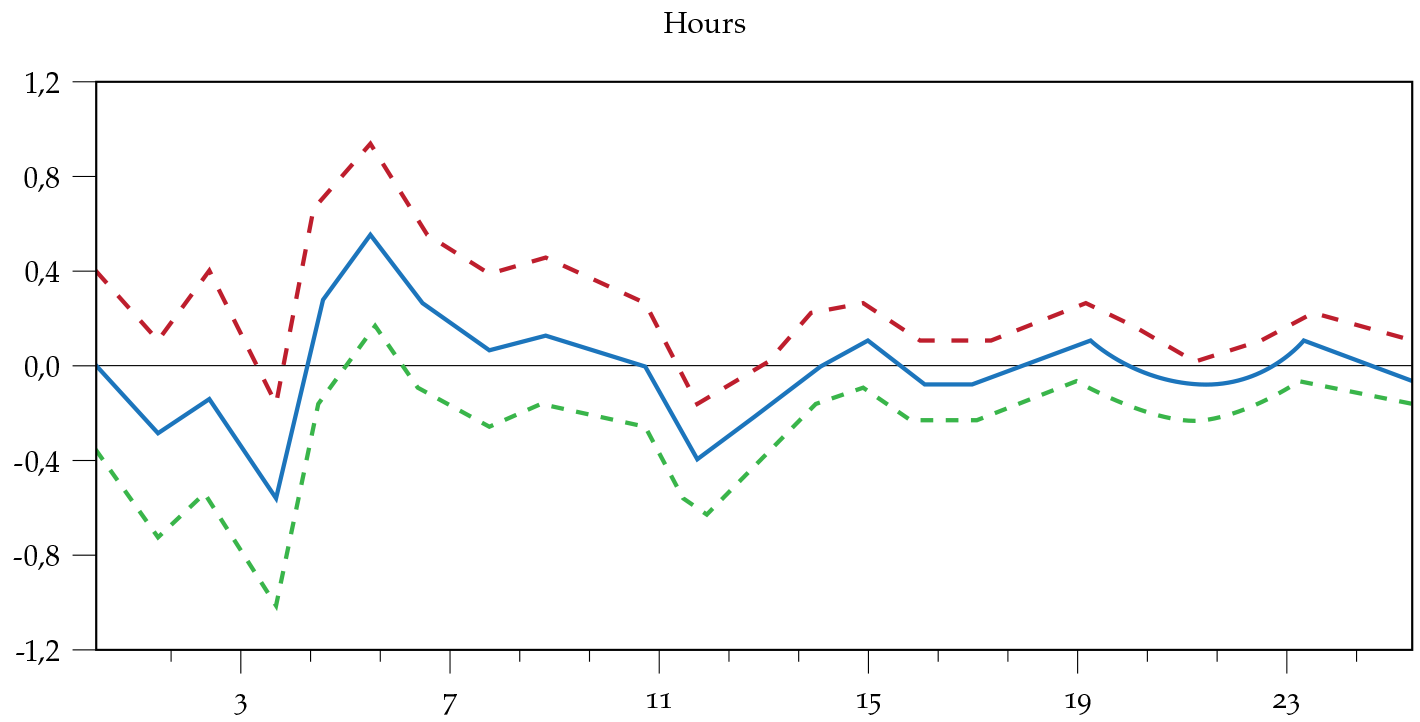

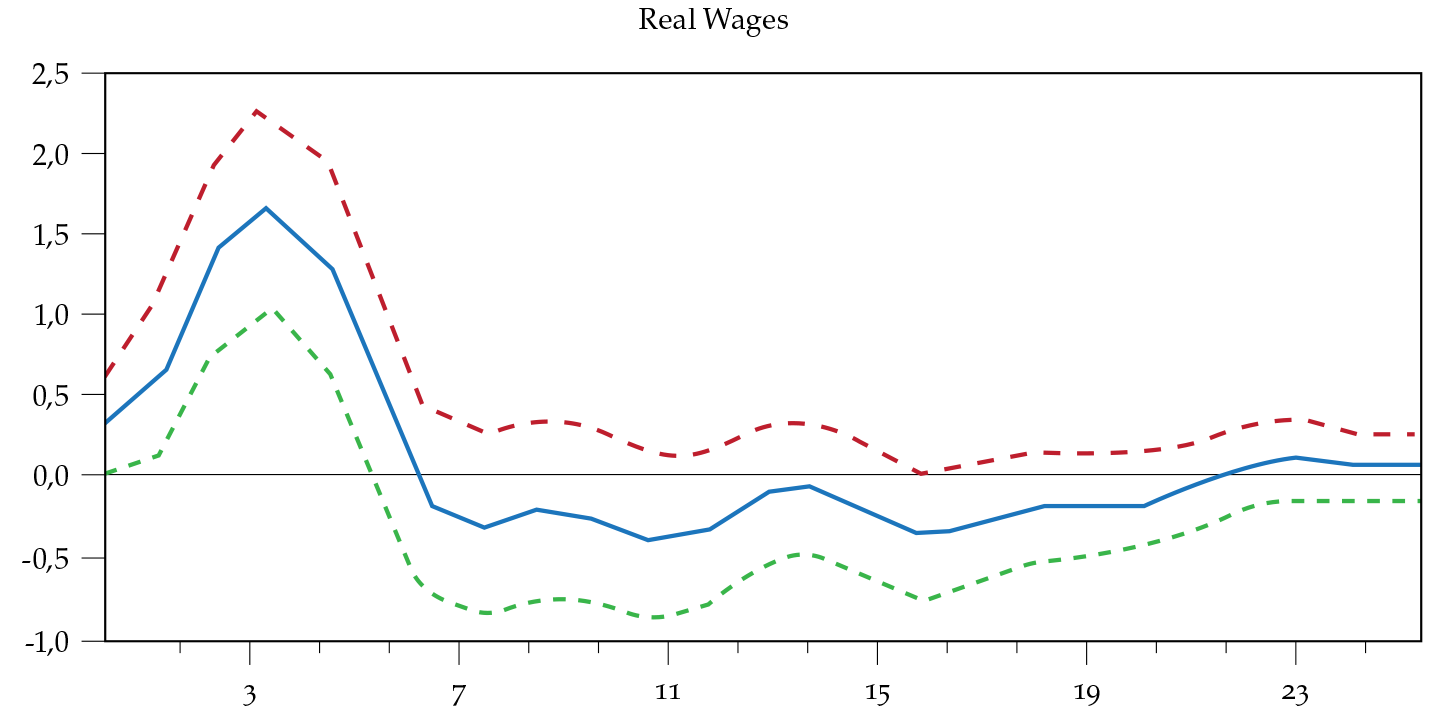

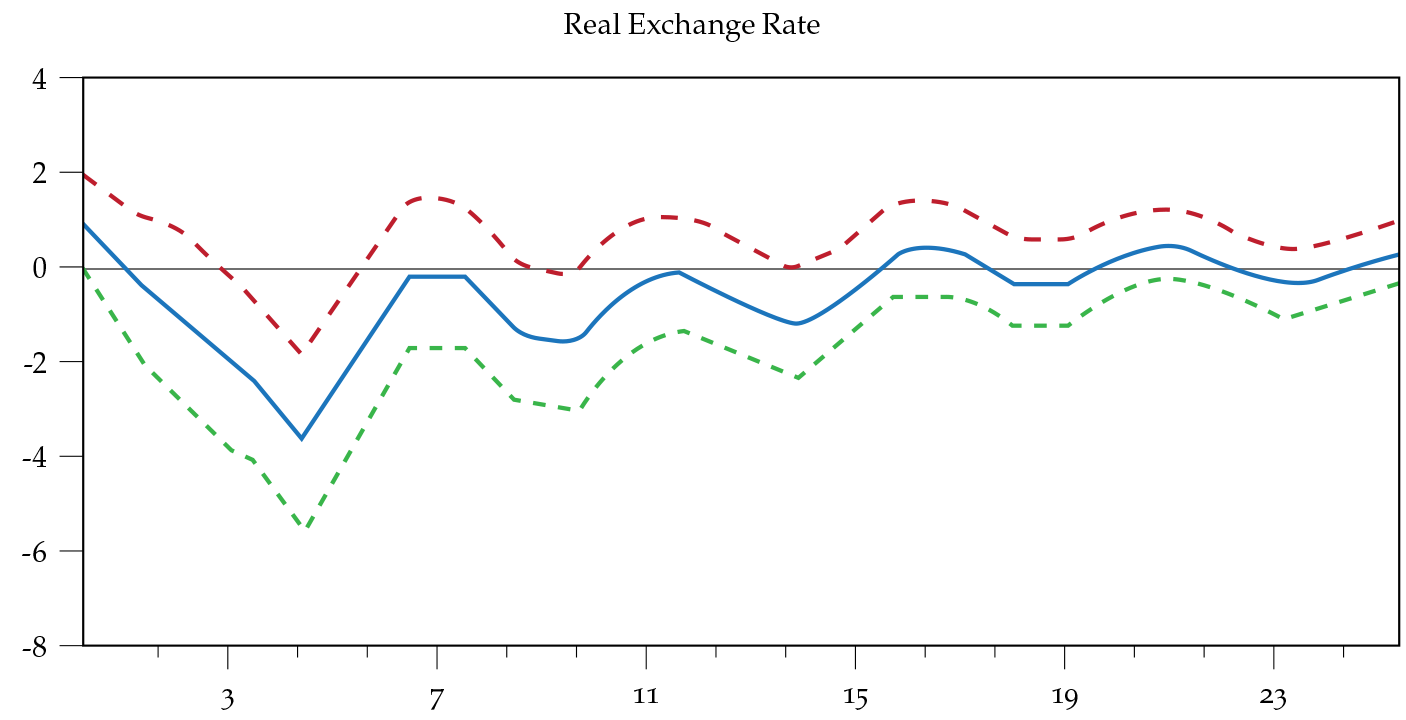

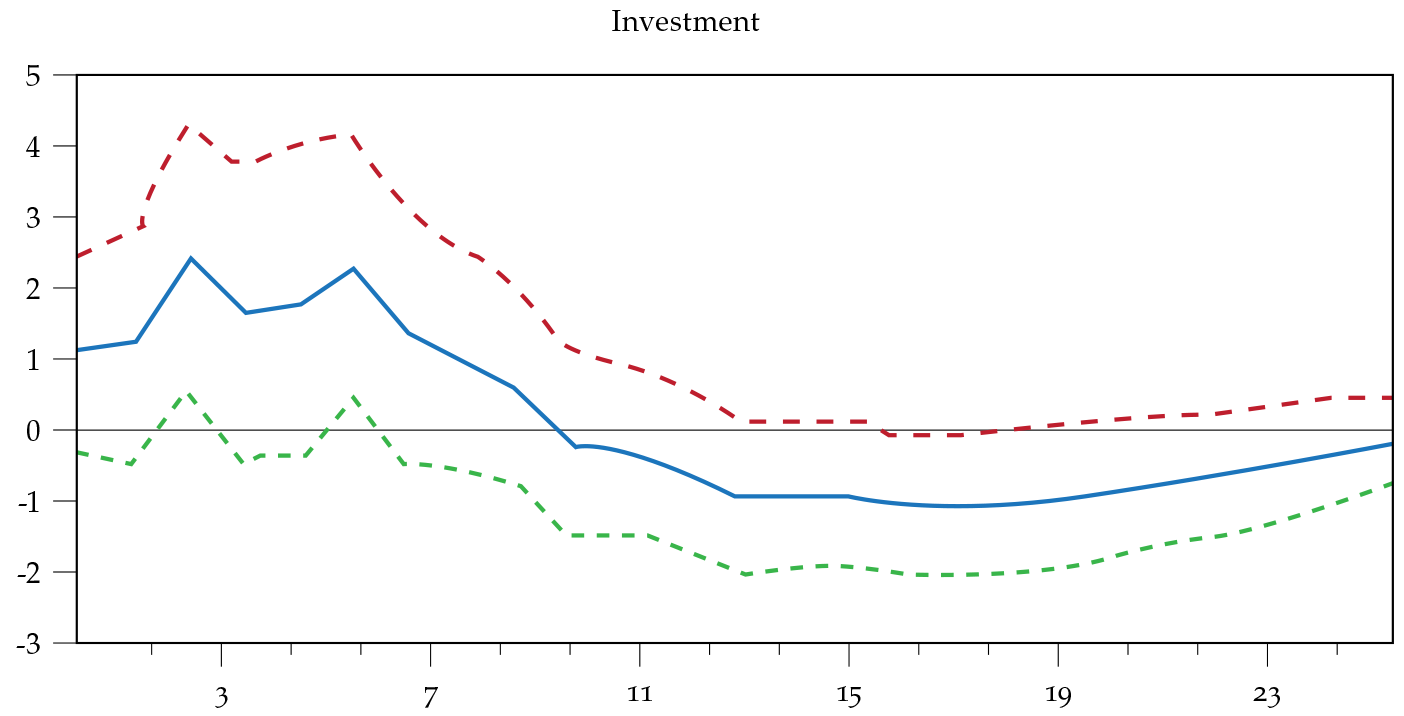

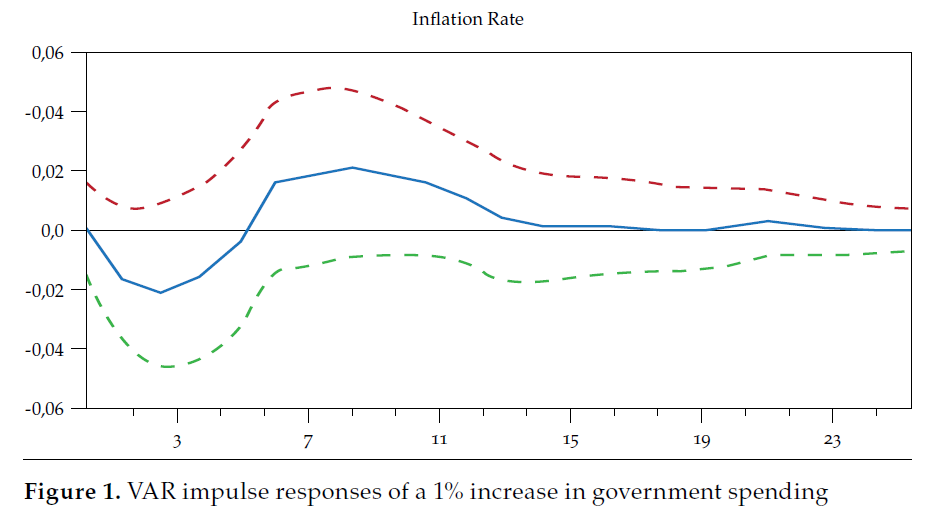

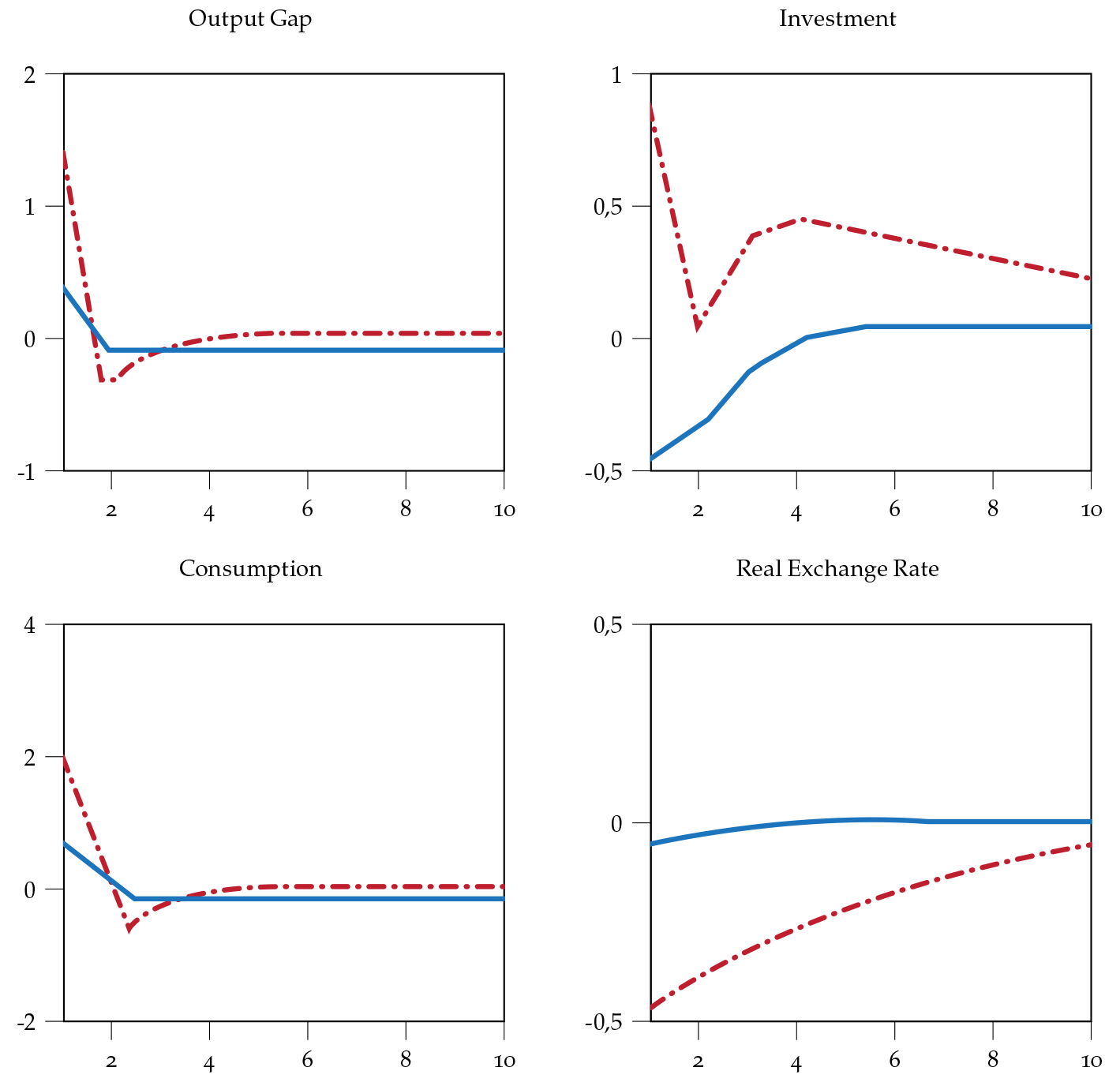

Following Vargas, González, and Lozano (2012), we identified the government spending shock with a method that meets the criteria of non-anticipation and no-contemporaneous correlation with output. To do so, we defined the shock as the difference between the Central Government’s actual primary expenditures —overall spending without interest payments on public debt— and the variable’s forecast. Next, we considered the effect of the shock in a VAr. The data is quarterly from 1999 until 2011. We used Ramey’s (2011) strategy of using a fixed set of variables and rotating other variables of interest. The fixed set of variables consisted of the non-anticipated spending shock, the log of real per capita government spending, and the log of real per capita GDP. We then rotated each of the other variables in the VAr: consumption, hours, real wages, real exchange rate, and investment. The results are plotted in figure 1.

We normalized the impulse responses to an unanticipated government spending shock to obtain a response of government spending equal to one. In addition, we used the ratio of GDP to government spending of 6.7 during the period in order to directly obtain the implied fiscal multiplier. Studies for other countries show evidence of an increment of consumption as a response to a government spending shock (Ravn, Schmitt-Grohé & Uribe, 2007; Mountford & Uhlig, 2009; Monacelli & Perotti, 2010; Ramey, 2011). In Colombia, our results show that consumption reaches a peak in the third quarter, and the effect is about 1.2, which suggests that the presence of non-Ricardian agents is an important feature in our economy. On the side of investment, it increases by about 1 in impact, and it is positive, reaching a peak in the fifth quarter. That is the main focus of our paper, given that balance sheet effects are present basically in the investment side of the economy. However, there is a widely spread idea that government spending causes crowding out of the investment. The evidence presented here suggests it is not the case. The other important result is that the impact output fiscal multiplier is around 0.4, with a maximum of 1.2 in the second quarter. The long-run fiscal output multiplier is 3.3 in the fourth quarter horizon.

F i g u r e 1 also presents the response of real wage that increases as expected by models with non-Ricardian agents like the model by Galí et al. (2007) and by those that eliminate the wealth effects on preferences like the one of Monacelli and Perotti (2010). In the case of the inflation rate, it exhibits a negative response at the beginning that afterward increases. Finally, figure 1 plots the impulse response of the real exchange rate and the hours worked, which do not present a definite pattern.

3. The Model

The model we used is based on the financial frictions’ models of Bernanke et al. (1999), Gertler, Gilchrist, and Natalucci (2007), and Carrillo and Poilly (2013), which also followed the models of Galí et al. (2007) and Kumhof and Laxton (2013). As in Galí et al. (2007), the model was characterized by the presence of non-Ricardian agents, which is an essential characteristic of developing countries such as Colombian. From Kumhof and Laxton (2013), we borrowed the way they introduced different fiscal policy rules. The whole model is presented in the online appendix. Here we present the characteristics that make it different from a standard new-Keynesian model.

Financial accelerator mechanism

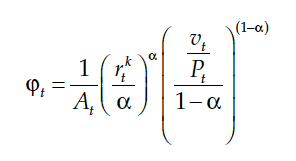

The financial accelerator mechanism introduced by Bernanke et al. (1999) explains how credit market imperfections propagate and magnify initial shocks to the economy. This set up is done at the level of entrepreneurs who make the investment decisions in the economy and also decide how to finance the capital investment. The cost of financing (dependent of the firm’s balance sheet) and the evolution of the net worth of the entrepreneurs explain the magnification of the initial shocks. Entrepreneurs purchase capital in each period, kt − 1, and use it in combination with hired labor, nt, to produce the wholesale output good in the economy, yh. They use a constant-return-toscale technology:

(2)

(2)Where At is an exogenous technology shock and 𝛼 is the share of capital output. The entrepreneurs choose kt − 1 and nt to maximize profits subject to the production technology. The resulting real marginal cost includes real rental rate of capital, nominal wage, prices of home goods, and prices of foreign goods in local currency (the price of foreign goods equals the external price of foreign goods times the real exchange rate):

Where rk represents the rental rate of capital and P v denotes the consumption price index, CPI, that normalizes every price index of the economy.

We now consider the capital acquisition decision. The entrepreneur finances its purchases of capital partly with his or her own net worth (nominal) available at the end of period t, N t and partly by issuing nominal bonds, B t + 1 . Capital financing is divided between net worth and debt as follows:

(3)

(3)Where Qt corresponds to the price of a unit of capital, which varies depending on the capital producing technology. The comparison between the expected marginal return to holding capital with its expected marginal financial cost determines the entrepreneurs’ demand for capital. The expected gross nominal return to holding a unit of capital from t to t + 1 E t F t + 1 is defined as:

(4)

(4)Where τk, t represents government tax on capital, and the parameter δ, the capital depreciation rate, and P t is the general price level that will be defined bellow. The second term is the capital gain enjoyed by the entrepreneurs.

Following Bernanke et al. (1999), the balance sheets effects that affect investment are given by the financial friction. In their set up, there is a costly state-verification problem that limits the entrepreneurs to borrow from lenders. The financial cost condition for purchasing capital is the main feature of this model. According to Bernanke et al. (1999), lenders must pay a fixed auditing cost if they wish to observe the borrower’s realized returns. This cost is interpreted as the one of bankruptcy or default. Additional costs (the premium) over riskless interest rate R t+1 are imposed on borrowers if they demand external funds.

The default risk depends on the degree to which the entrepreneurs depend on external funds, debt. This leads to a relationship between two important ratios: E t f t +1 to R t + 1 and the one of net worth to assets, as follows:

(5)

(5)Where (1 + πt + 1)γb ψ is a term that adjust nominal debt to inflation at a rate γ b ∈ [0,1].

As explained by López, Prada, and Rodríguez (2009), when the ratio of internal funds is low, the default risk is high, and, in this case, the cost of borrowing rises. The optimal (incentive-compatible) debt contract specifies that there is a wedge between the expected return on purchasing one new unit of capital and the rate at which households are willing to lend. Moreover, as shown by Bernanke et al. (1999), this wedge (known as the external finance premium) will be an increasing function of entrepreneurs’ leverage (given by  The parameter ψ represents the elasticity of the external finance premium with respect to the balance sheet position of entrepreneurs. The agency cost and the external finance premium vary with borrowers’ financial health. Higher monitoring cost implies a higher elasticity of external premium on external funds to a change in the balance sheet position. In consequence, the higher the monitoring cost, the higher will be the volatility owing to financial market imperfections.

The parameter ψ represents the elasticity of the external finance premium with respect to the balance sheet position of entrepreneurs. The agency cost and the external finance premium vary with borrowers’ financial health. Higher monitoring cost implies a higher elasticity of external premium on external funds to a change in the balance sheet position. In consequence, the higher the monitoring cost, the higher will be the volatility owing to financial market imperfections.

Finally, after repaying loans, a fraction 1 – v of entrepreneurs exits the market and transfers the remaining profits to Ricardian households. The same fraction enters the market every period, each receiving a startup capital injection from Ricardian, and thus, the law of motion of net worth evolves as follows

(6)

(6)The first term on the right-hand side represents the ex-post return of capital, and the second one the ex-ante cost of borrowing, where v is the share of equity held by entrepreneurs at t1 who are still in business at t. When debt contracts are denominated in nominal terms, γ b = 0, in such a case, an unexpected positive change in inflation improves net worth since the return on capital increases, but the nominal debt remains constant. This effect is called the debt deflation channel or the Fisher effect. Again, as pointed out by López et al. (2009), the introduction of net worth as an additional state variable allows us to explain the propagation and magnification of different shocks to the real economy. Shocks to net worth relative to total finance requirements generate endogenous changes in the external finance premium charged above risk-free rates. Besides, net worth may be highly sensitive to unexpected changes in asset prices, especially if firms are leveraged, which is a multiplier effect. An unanticipated increase in asset prices rises net worth more than proportionately (causing a fall in the external finance premium), which stimulates investment and, in turn, increases asset prices even further. Retailers buy output from entrepreneurs and slightly differentiate it at no resource cost and set prices à la Calvo (1983).

Capital Producers

Capital producers purchase consumption goods as material input, x t , and combine it with rented capital, k t , to produce new capital. Following Dib and Christensen (2008), we assume that capital producers are subject to quadratic capital adjustment costs. Their optimization problem, in real terms, consists of choosing the quantity of investment to maximize profits, so that

(7)

(7)Where q t = Q t /P t

The first order condition is

(8)

(8)With 𝜅 being the capital adjustment cost parameter and q = Qt /Pt .

The aggregate capital stock evolves according to:

(9)

(9)Domestic and Imported Investment

The investment bundle, x t , aggregates domestic and foreign investment according to the next function (10) with its corresponding price index.

(10)

(10)Households

There is a fraction Γ of non-Ricardian households in the economy whose variables are denoted by n, and a fraction (1 − Γ) of Ricardian agents whose variables are denoted by r. The utility function of households is non-separable between consumption and labor.

Ricardian Households

Ricardian Households, denoted by r, are indexed between Γ and one and have preferences of the form:

Where c r,t is a consumption index, and n r,t are hours worked. The parameter σ r measures the intertemporal elasticity of substitution, θ r is a scale parameter, and γr the inverse of the Frisch elasticity. Those preferences were introduced by Greenwood, Hercowitz, and Huffman (1988) and have the property of muting the wealth effect on labor supply. These households maximize utility subject to the budget constraint:

The terms on the right-hand side represent sources of income, including after-tax labor income, domestic real discount bonds issued by the entrepreneurs, foreign bonds holdings, profits from unions, intermediate firms and entrepreneurs, and lump-sum net transfers, respectively. The left-hand side of the equation represents purchases in consumption including taxes and purchases of domestic and foreign assets, where following Schmitt-Grohé and Uribe (2003), the foreign interest rate  depends on the country’s net foreign asset position, b⋆, as a percentage of GDP, the real exchange rate,

depends on the country’s net foreign asset position, b⋆, as a percentage of GDP, the real exchange rate, and an exogenous risk premium shock, φb

. The parameter that defines the Fisher effect in this way is called γ

b

. It is equal to zero when debt contracts are denominated in nominal terms, giving rise to the Fisher effect. It is equal to one when nominal debt adjusts to inflation.

and an exogenous risk premium shock, φb

. The parameter that defines the Fisher effect in this way is called γ

b

. It is equal to zero when debt contracts are denominated in nominal terms, giving rise to the Fisher effect. It is equal to one when nominal debt adjusts to inflation.

Non-Ricardian Households

Non-Ricardian households, denoted by n, are indexed between 0 and Γ and solve a similar problem, but they are assumed to have no access to financial markets. Therefore, they consume all their labor income and the transfers received from the government period by period. They seek to maximize their lifetime utility:

subject to the budget constraint:

Where the sub-index n stands for non-Ricardian, cn,t is a consumption index, and nn,t are hours worked. The parameter σn measures the intertemporal elasticity of substitution, θ n is a scale parameter, and γ n the inverse of the Frisch elasticity.

Domestic and Imported Consumption

It is assumed that the composition of the consumption bundle is identical for both types of households. It takes the form:

(1)

(1)Where ct is a ces index that includes domestic and foreign goods, with parameter α c determining the degree of openness, and η c the elasticity of substitution between domestic and imported goods. The LaGrange multiplier, P t , denotes the consumption price index, CPI, that normalizes every price index of the economy.

Government

Monetary Policy

The monetary policy follows a conventional simple policy rule. The interest rate is set by the Central Bank according to

(11)

(11)Where the long-run interest rate is ¯i, the inflation target is π¯ , and the feed-back parameter is ρπ.

Fiscal Policy

The government purchases both domestic and foreign goods. These purchases are assumed to have null effects on private utility or productivity. Again, the government bundle of goods G t is a ces aggregator of domestic and imported government purchased goods, also with its corresponding price index.

(12)

(12)In addition, government tax consumption, labor income, and capital transfer resources to non-Ricardian and Ricardian households have access to international debt markets. The government budget constraint takes the following form:

(13)

(13)

(14)

(14)Where St is the primary surplus, and Tt denotes the total tax revenues. The second term on the right-hand side is oil revenues from government,  is the government spending as a percentage of GDP, and T

t

is the lump-sum net transfers. The international price of oil, pt

m*, is assumed to follow an exogenous auto-regressive process, implying a domestic oil price

is the government spending as a percentage of GDP, and T

t

is the lump-sum net transfers. The international price of oil, pt

m*, is assumed to follow an exogenous auto-regressive process, implying a domestic oil price  ; oil production, y

t

m

, is assumed to be exogenous. The parameter ω denotes the share of oil production that the government owns, so that a fraction ω of oil revenues accrues to the government, whereas the remaining share of oil revenues goes to foreign companies. Total tax revenues correspond to collected taxes on consumption, capital, and labor income.

; oil production, y

t

m

, is assumed to be exogenous. The parameter ω denotes the share of oil production that the government owns, so that a fraction ω of oil revenues accrues to the government, whereas the remaining share of oil revenues goes to foreign companies. Total tax revenues correspond to collected taxes on consumption, capital, and labor income.

(15)

(15)Government surplus gst is defined as:

(16)

(16)which equals the primary surplus and net interest payments on government debt.

The share of government expenditure to real GDP of the economy, gt , is assumed to follow an exogenous and auto-regressive process:

(17)

(17)where g- is g the long run government share, and ρ G captures the persistence of the process.

Similarly, tax rates on wages, consumption, and holdings of capital are allowed to vary according to:

(18)

(18)

(19)

(19)

(20)

(20)Where τ n, τ k , and τ c are long-run tax rates, ρτn, ρτk , and ρτc represent persistency, and ∈τn , ∈τk , and ∈τc are i.i.d. white noise shocks.

The final component of fiscal policy is the one explained in the next section.

Fiscal Policy Rules

The fiscal policy rule of the government takes the form of

The overlined variables denote their steady-state values, and gsrat is a structural surplus target. A fiscal rule similar to this was introduced in Colombia in July 2011 with a structural surplus target of -2.3% for the year 2014. The remaining items correspond to cyclical adjustments, according to excess tax revenue, excess revenue from the mining sector, and an additional debt gap variable. The parameter 𝜔 is the share of government oil revenues.

A strict balanced budget rule (BBR) corresponds to the parameter values of d tax = d m = d debt = 0. These rules are highly procyclical because they call for higher spending in a boom. An alternative rule, introduced in countries like Chile (see Céspedes, Fornero & Gali, 2013) and Norway (see Pieschacón, 2012) to avoid problems such as the Dutch disease phenomenon, is a structural surplus rule (ssr) that ties government spending to structural/permanent government revenues. This is the case of the parameter values of d tax = d m = 1 and d debt = 0. Finally, a countercyclical fiscal rule is implemented in the case that d tax > 1, which calls for a higher tax rate (or lower spending) in a boom. This rule would represent strong automatic stabilizers, such as progressive taxation or countercyclical transfers: for example, unemployment insurance (see Kumhof & Laxton, 2013).

In order to achieve the objective of the targeting rule, the fiscal authority has five instruments, three taxes 𝜏 c,t , 𝜏 n,t , and 𝜏 k,t , and two spending items Tt and Gt . The default instrument for our baseline results is transfers Tt . In this case, the fiscal rule is given by:

(21)

(21)So that the fiscal rule activates when the variables of interest to the government deviate from their steady-state values, and T has been set to satisfy the structural surplus budget.

Rest of the World

Foreign demand of home-produced goods c h⋆ is given by

(22)

(22)Where the parameter μ represents the price elasticity of exports. The model also consists of labor unions and agencies that set wages à la Calvo (1983). Their problem is described in detail in the online model appendix.

4. Calibration

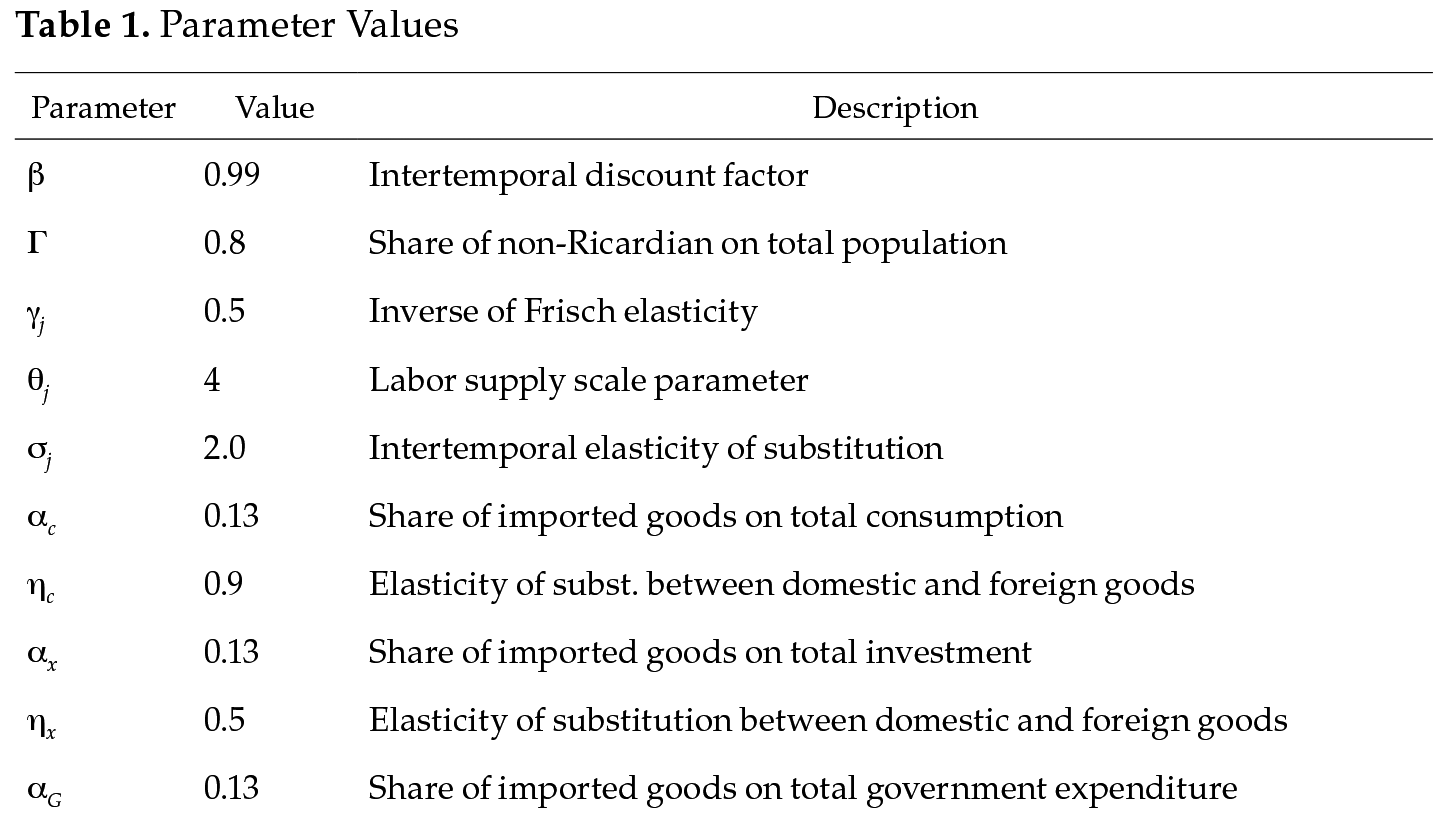

In this section, we present the calibration of the model for the Colombian economy. The parameter that governs the financial frictions corresponds to the inverse of the elasticity of the external finance premium to leverage. In our simulations for the model with the financial accelerator, this parameter was set at 0.05, according to the estimates by López et al. (2009). The other parameters were calibrated as in González et al. (2014). The subjective discount factor β is set to 0.99, implying a steady estate interest rate of 4%. The parameter ω is consistent with the government’s share on total mining sector dividends, which corresponds to the share of government in the State’ firm Ecopetrol. The long-run values 𝜏 are in line with estimates by Fergusson (2003) and Hamann, Lozano, and Mejía (2011). The long-run ratio of government expenditure to GDP g is 0.15 according to the data.

We also calibrated the Calvo price probability, ε h , in 0.7, according to estimates for Colombia by Bejarano (2005), which is also in line with the estimates for the United States by Smets and Wouters (2007). The Calvo wage probability was calibrated in 0.4 for Ricardian agents in line with estimates for Colombia by Bonaldi, González, and Rodríguez (2011), and we assumed a low wage rigidity for the non-Ricardian agents.

For the parameter Γ, the share of non-Ricardian agents in the Colombian economy, we used a Superfinanciera (the banking supervision agency in Colombia) dataset recorded by each bank in the 341-form about credit card holders as a percentage of the population in working age reported by DANE (the Colombian statistics department): 20%. This parameter value is also consistent with Prada and Rojas (2009), who found that informal labor in Colombia is about 70% of total labor. This parameter value is also similar to the one estimated for the Chilean economy by Corbo and Schmidt-Hebbel (1991).

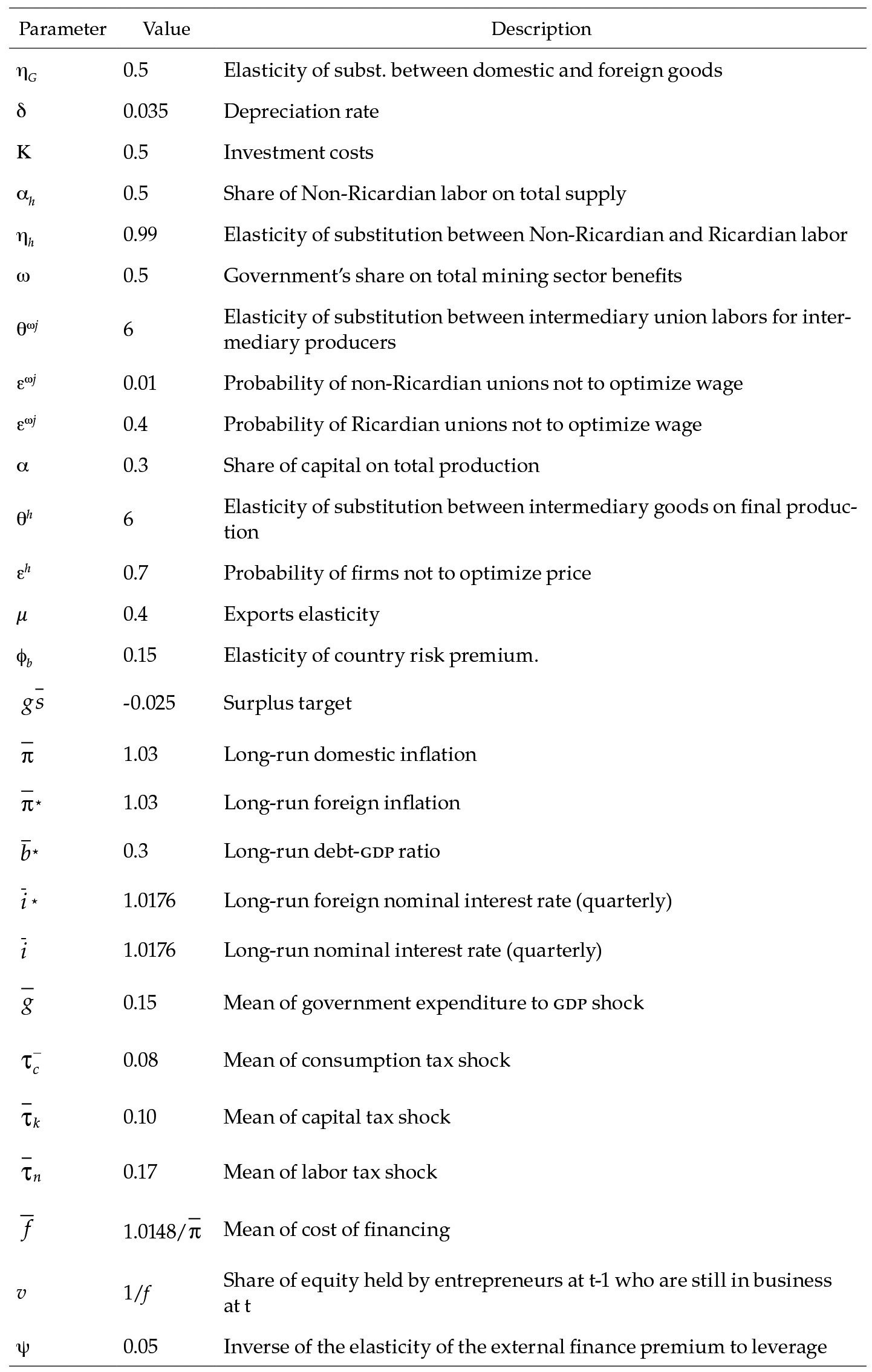

The elasticity of substitution among varieties of intermediate goods, θh, is calibrated in 6, which implies a steady-state mark-up of 20%, a common value used in the literature. The inverse of Frisch elasticity was calibrated in 0.5, according to Prada and Rojas (2009). The investment cost parameter 𝜅 is set at 0.5, as estimated by López et al. (2009) for the Colombian economy. The elasticity of country risk premium with respect to net foreign debt, φ b , is set equal to 0.15, which, as pointed out by Gertler et al. (2007), should be small enough so that the friction in the capital market does not alter the high frequency model dynamics but makes net foreign indebtedness revert to trend.

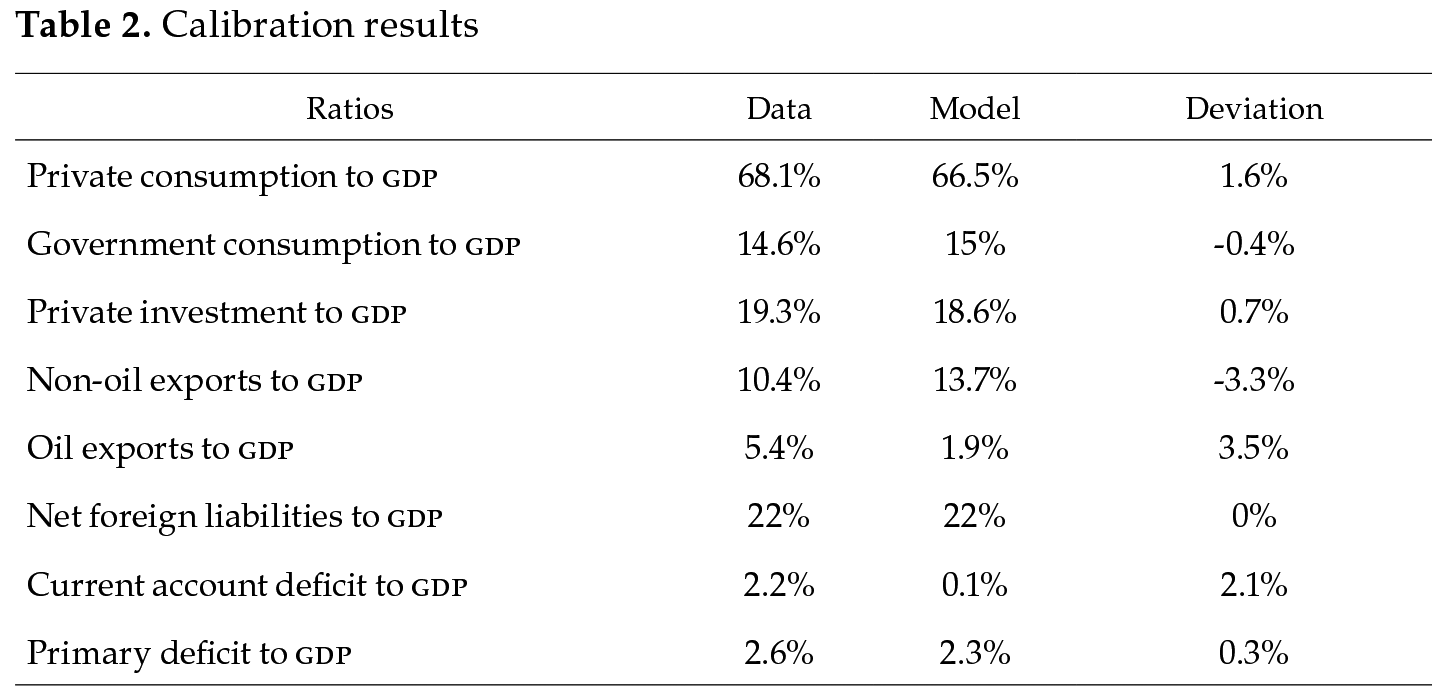

The elasticity of output to capital, α, is set to 0.3 to be consistent with the labor income share. The relative risk aversion coefficient, σ R , was set at 2.0, according to estimates by López (2001). We fix the steady-state world interest rate at 3% per annum. The steady state foreign and domestic inflation rates are set at 3% per annum. Table 1 summarizes all the parameters and their description. Finally, to compare how well the model describes the data, table 2 presents the different long-run ratios used for the calibration with their observed values in the data, their equivalent in the model, and the corresponding percentage deviation. How it can be observed, the model matched very closely the data.

5. Results

In this section, we present the impulse responses of the different models for different macroeconomic variables for a shock of government spending of 1%. We start by comparing the effects of a model with the financial accelerator effect but without the Fisher effect with one with financial accelerator and Fisher effect. After that, we analyze the behavior of macroeconomic variables in the case of an open economy and a “closed economy” both with financial accelerator and Fisher effects. Finally, we study the interaction between the fiscal multipliers of consumption and investment under the absence of nonRicardian agents in the economy.

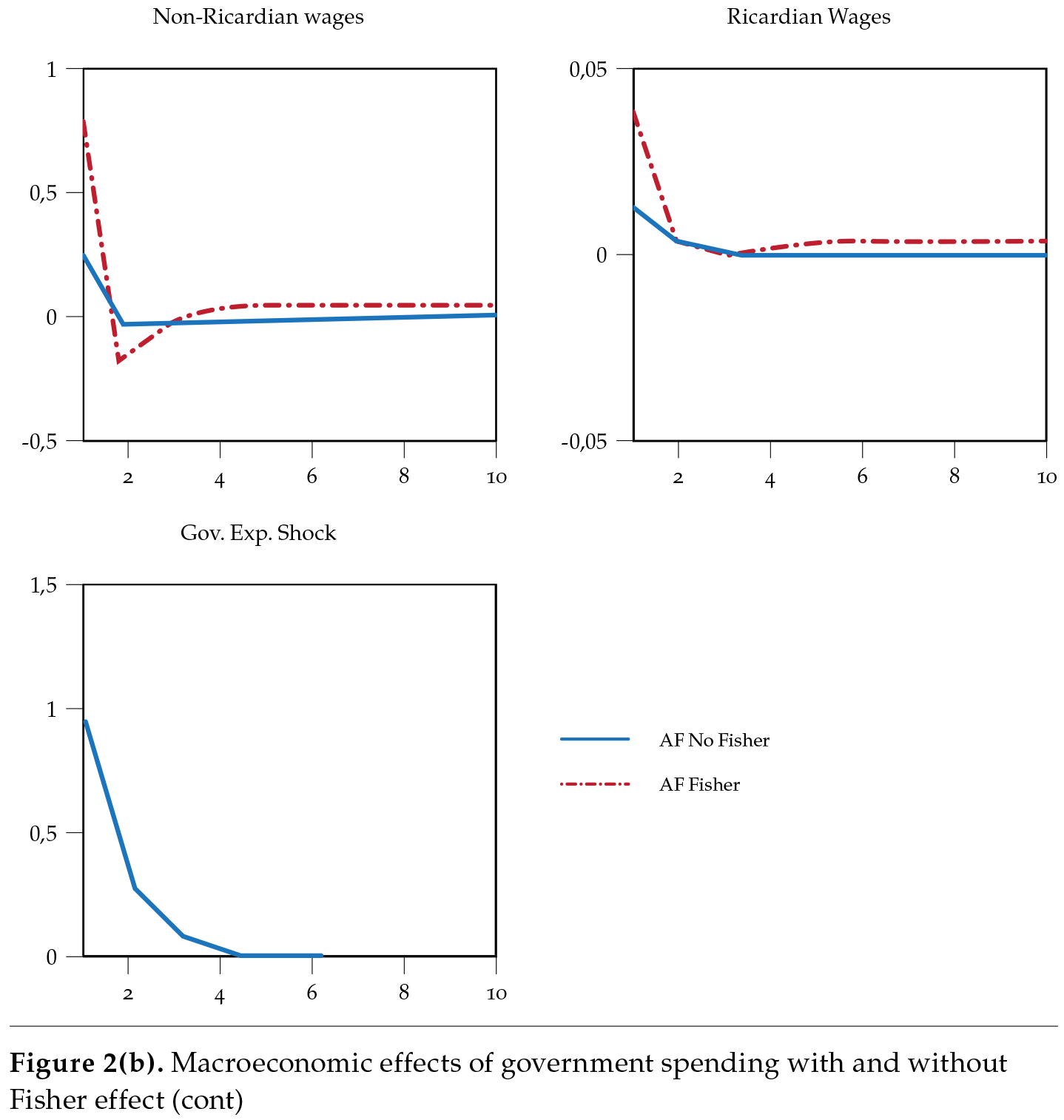

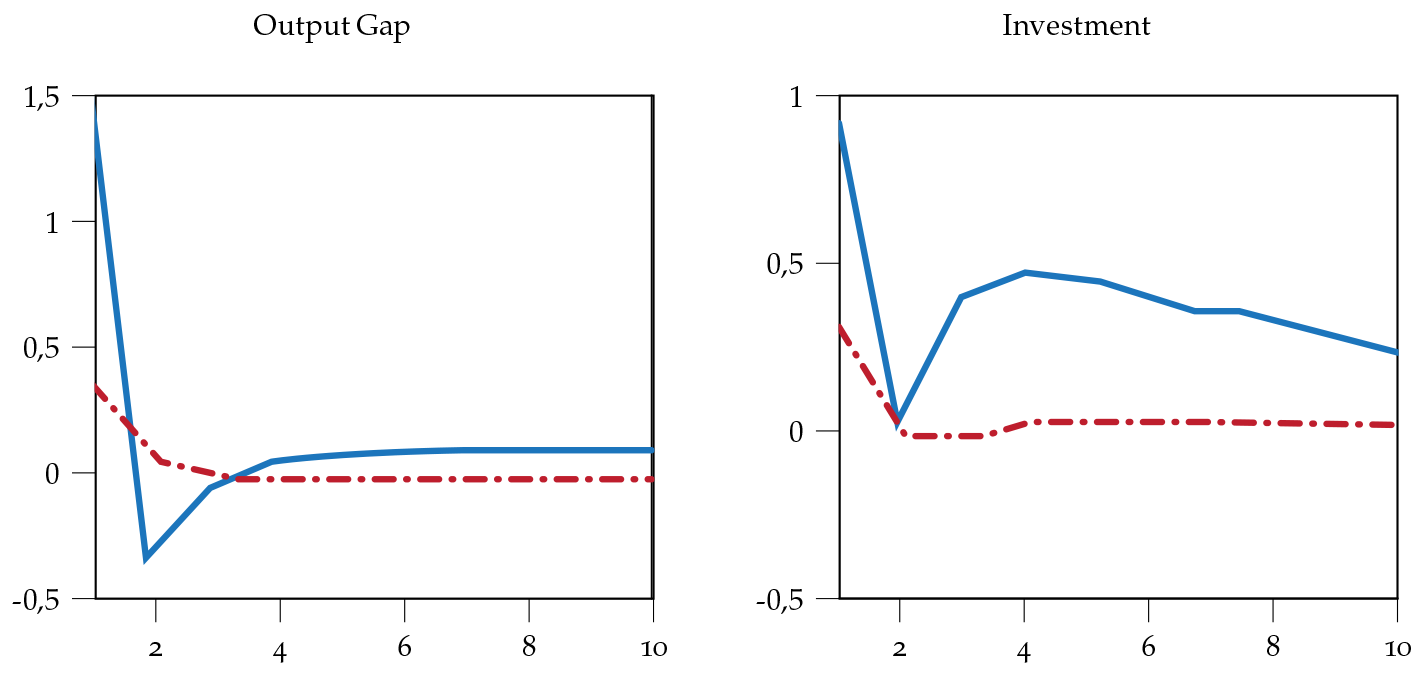

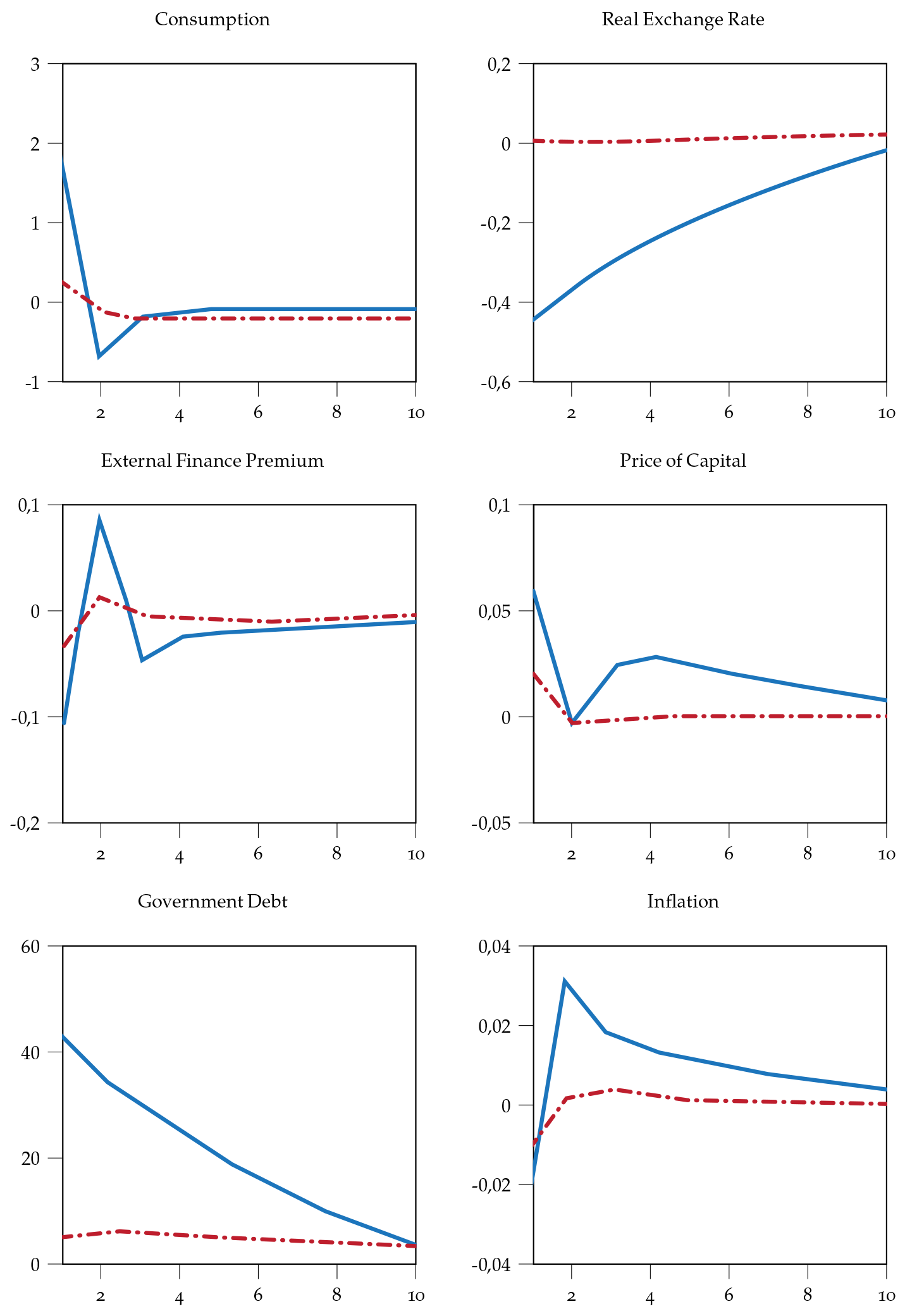

Fiscal Multiplier and Balance Sheet Effects with and without Fisher Effect

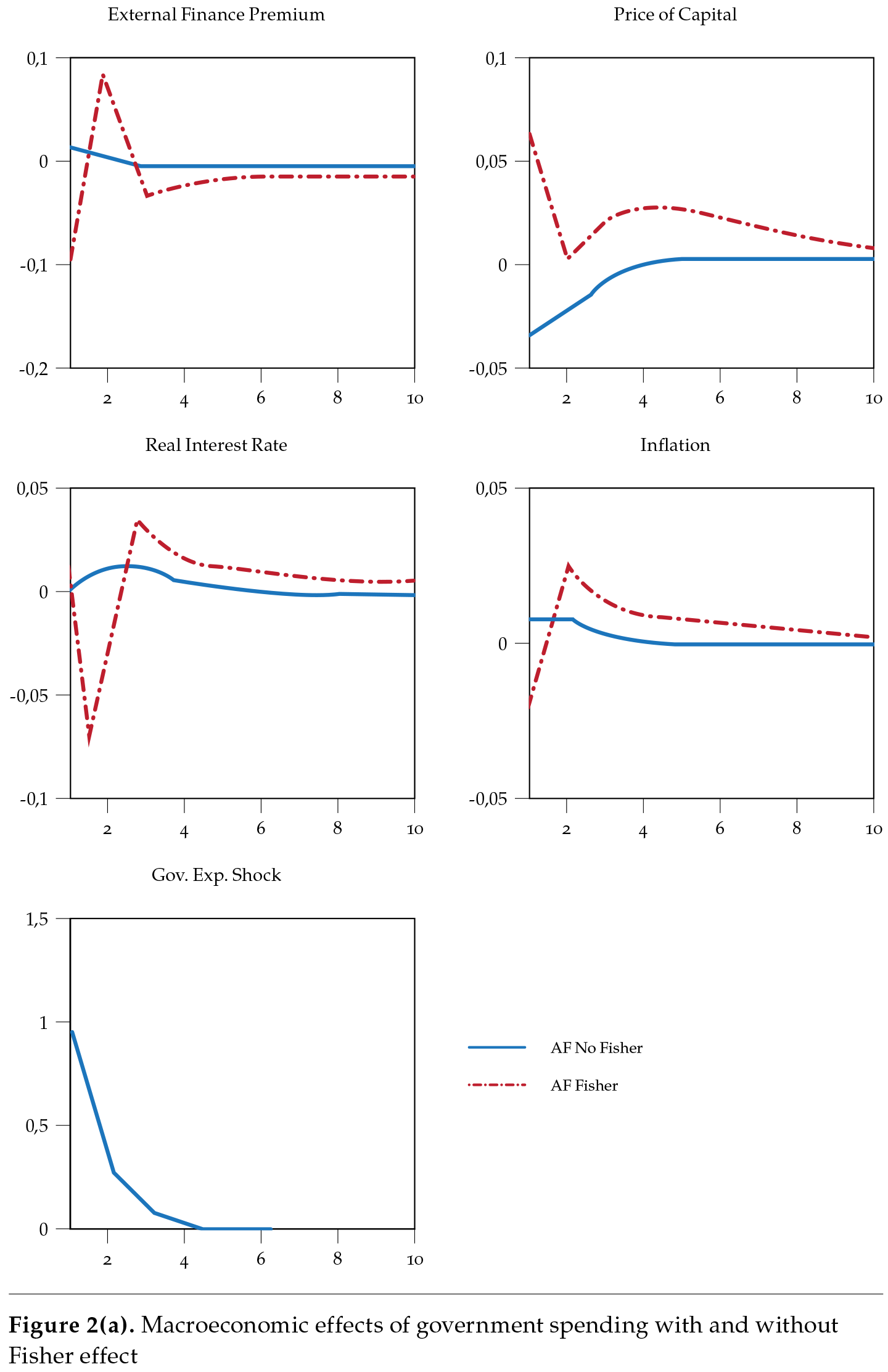

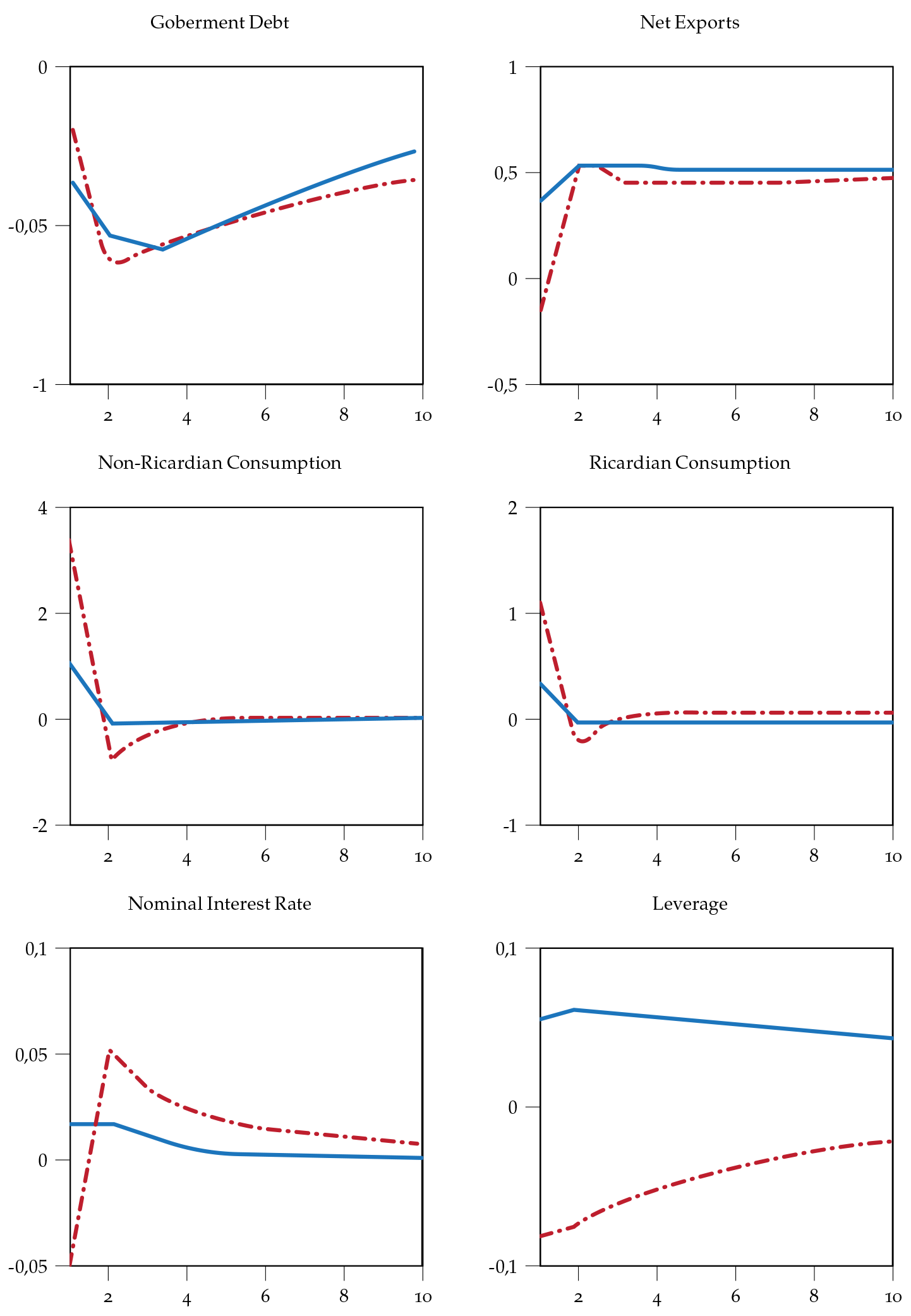

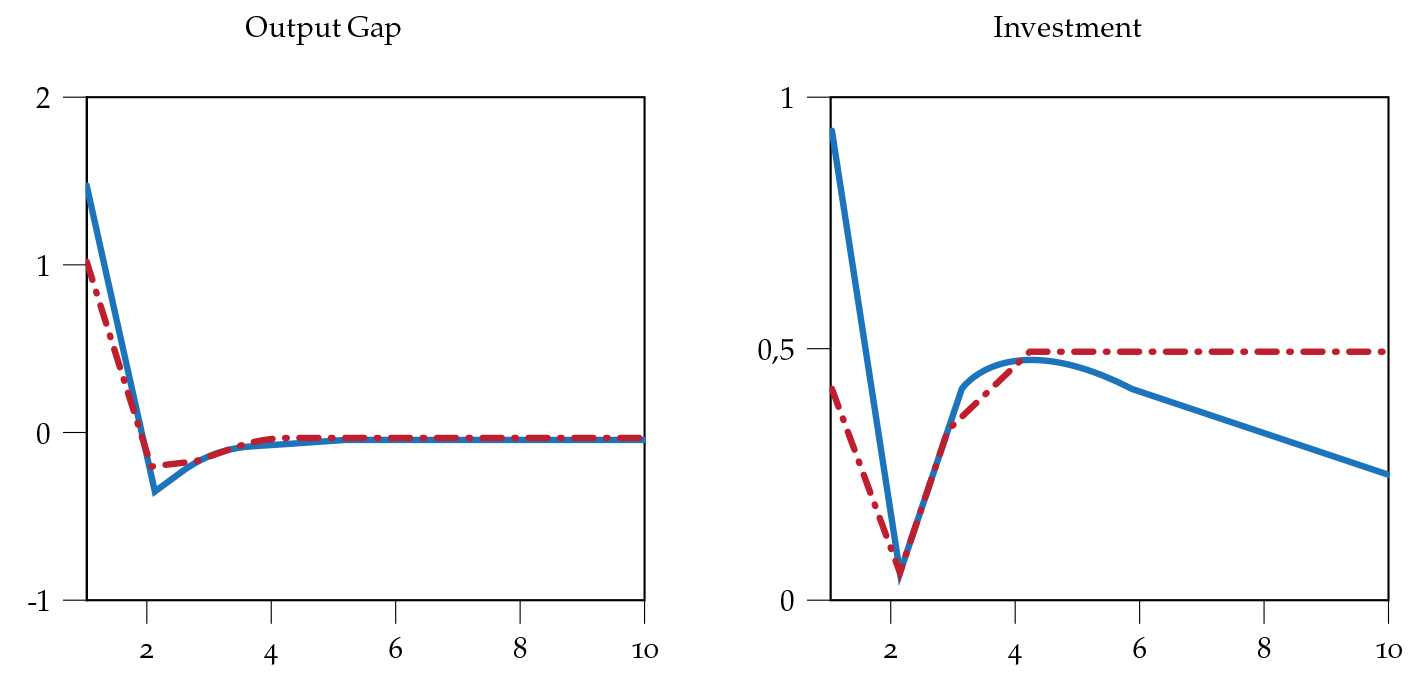

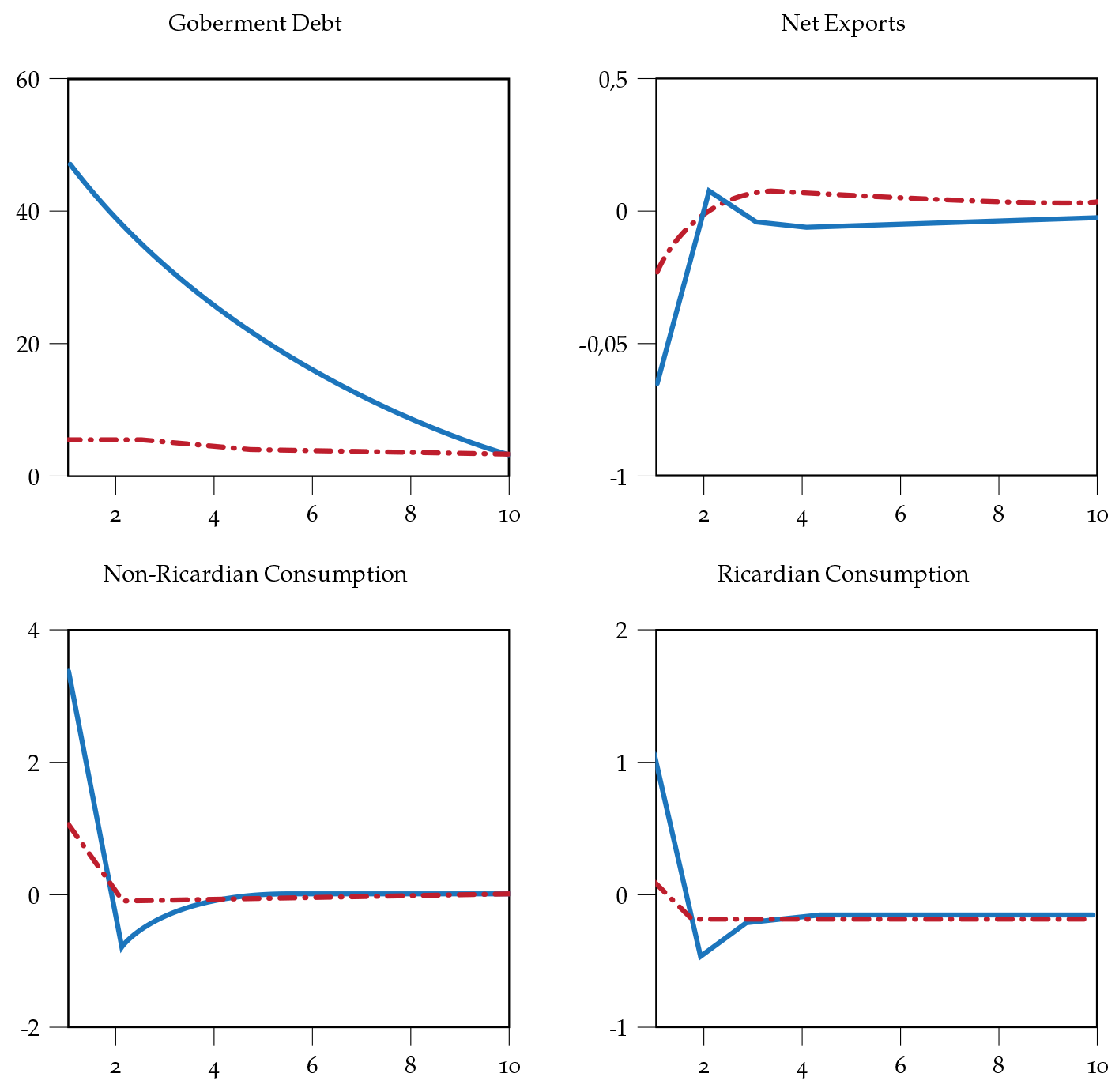

Our main goal here is to describe what happens to investment when there are balance sheet effects with and without Fisher effects (FAFisher and FAnoFisher, respectively). The results are presented in figures 2(a) and 2(b). In the case of a financial accelerator without the Fisher effect, the entrepreneurial debt adjusts to inflation, and it is present in the common result of a crowding out of the investment. The government spending causes an increase in the real interest rates that translates in lower asset prices that increment leverage and the external finance premium, causing a fall in investment.

On the contrary, in the case of nominal contracts in a small open economy, the government spending shock causes an initial fall in inflation but, afterward, it increases in a similar way as presented in the empirical evidence of the paper. In the model, the inflation rate increases in the period t + 1. This increase in inflation translates in a rise in net worth due to the Fisher effect, and this improves the external finance premium stimulating investment. In this case, it also presents a strong appreciation of the real exchange rate. The real interest rate falls in t + 1, and, as the price of capital is the discounted value of dividends, the price of capital rises, leverage falls, and the external finance premium also falls even further. All of this causes an increase in investment. In this case, the fiscal investment multiplier is near 1, very close to the multiplier presented in the empirical evidence of section 2. Thus, the model that better matches the data in the case of a small open economy is the one with financial frictions and Fisher effect. In the same way, the output multiplier is also close to the presented in the empirical evidence of 1.2.

Regarding the other macroeconomic variables, the results are the expected for models with GHh preferences, non-Ricardian agents, and wage rigidities such as the ones of Colciago (2011), Galí et al. (2007), and Monacelli and Perotti (2010). Consumption of Ricardian and non-Ricardian agents increases, as well as the hours worked and the wages (like in the empirical evidence). Notice that in the case of the model with financial frictions and the Fisher effect, the fiscal consumption multiplier is much closer to the empirical evidence than the one without it.

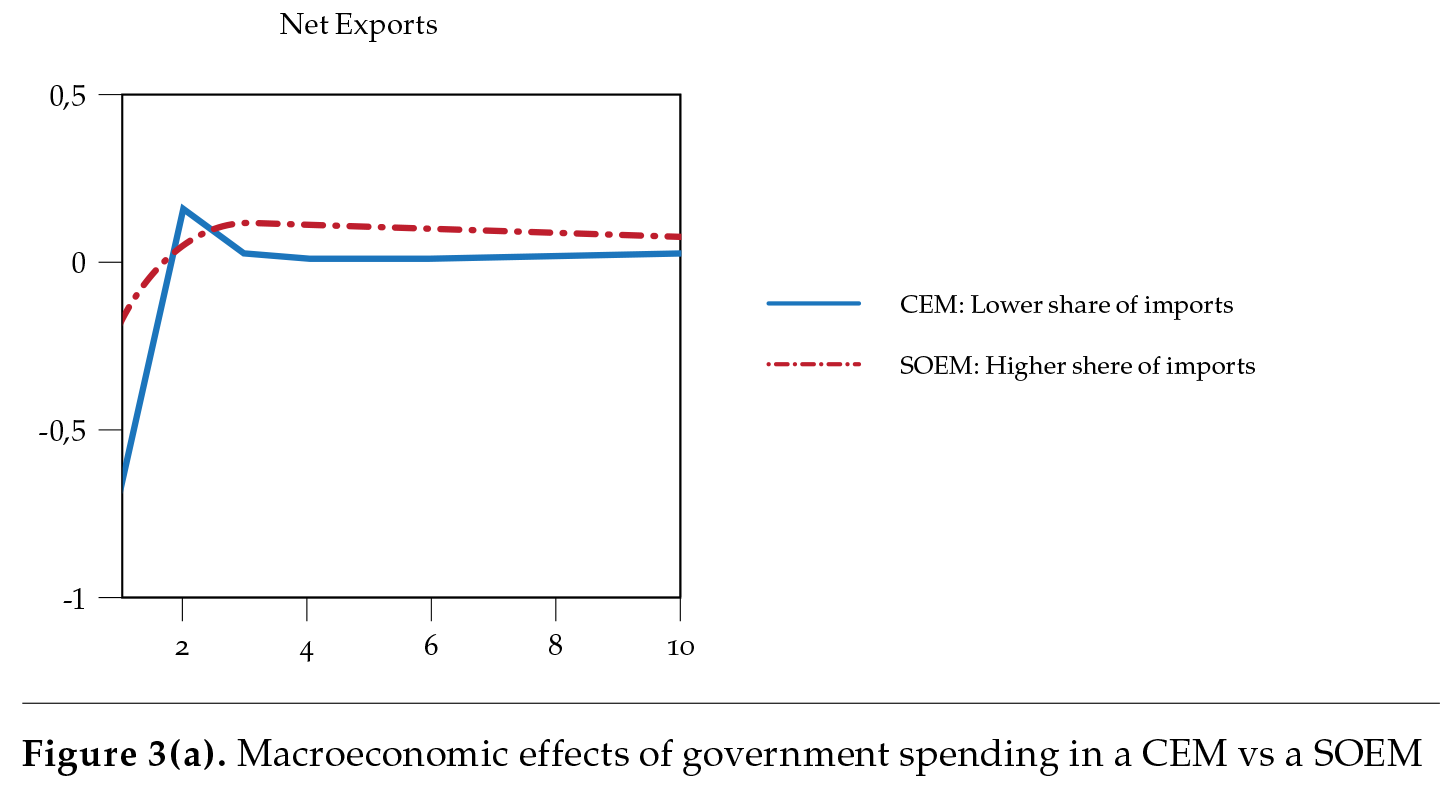

CEM and SOEM

In this section, we explore in more detail the role of the real exchange rate in the results for a small open economy model versus the ones for a closed economy like the ones presented by FV and CP.

Low Share of Imports

Here, we model a closed economy in the sense that it has a lower share of imports in the consumers’ bundle. This means that for the case of the closed economy, we used as a share of imports the value of 0.13, while for the case of an open economy, we set it at 0.5.

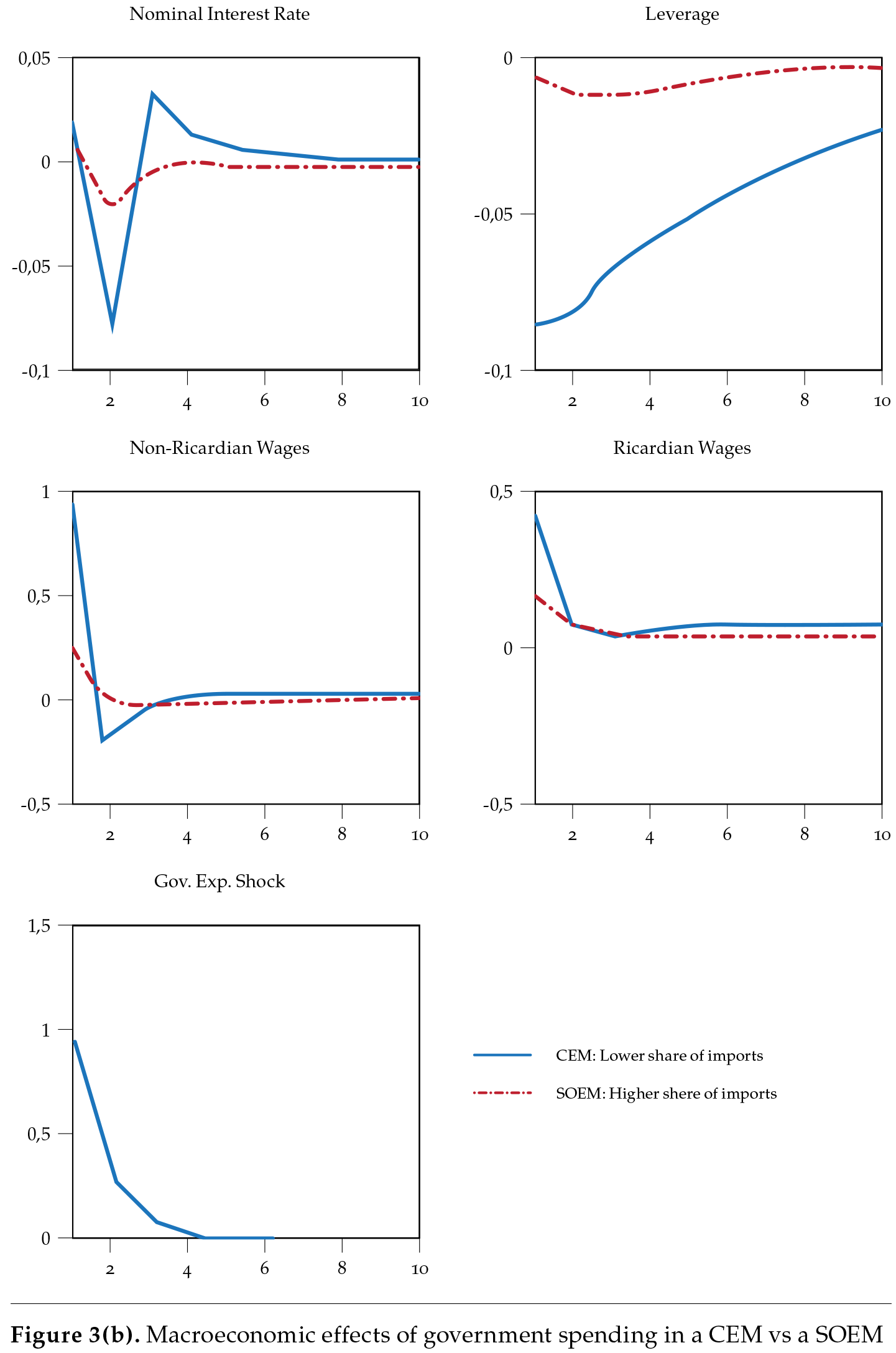

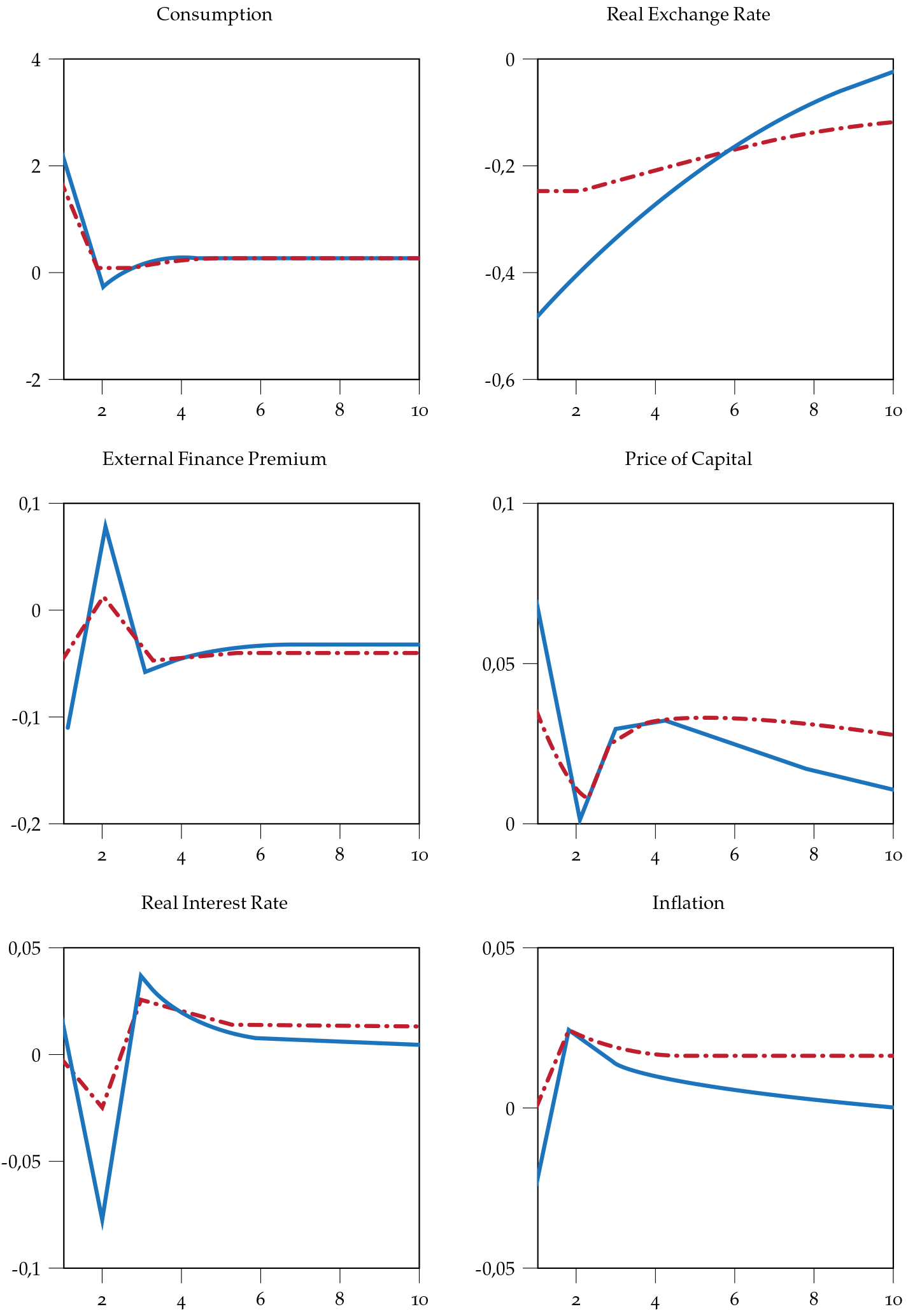

The main consequence of a soeM is that, besides the balance sheet channels, there is an additional channel that affects fiscal multipliers: the importsubstitution effect.

The results are presented in figures 3(a) and 3(b). In an open economy, the import-substitution effect acts as follows: the increases in the government expenditures induce a substitution away from domestically produced goods toward imported ones. There is a lower appreciation of the real exchange rate in the soeM, but the lower share of ceM’s imports causes higher total inflation in t+1 in the case of a ceM, and the balance sheet effects come into place. Leverage is lower in the case of the cEM than in the soeM and financing conditions for entrepreneurs improve, the price of capital and net worth are higher with the consequent higher investment in comparison with the SOEM.

Our results show that in the case of a ceM, fiscal multipliers are high. The output fiscal multiplier goes from 0.5 in the SOEM to 1.4 in the CEM. The case of investment is similar, doubling from a SOEM to a CEM. The consumption output multiplier increases almost three times from a soeM to a ceM, especially in the case of non-Ricardian consumption. Regarding the other macroeconomic variables, net exports are much lower in the case of the cEM due to the appreciation of the real exchange rate. Wages are also higher in the cEM case because of the demand impulse.

Lower Country risk Premium

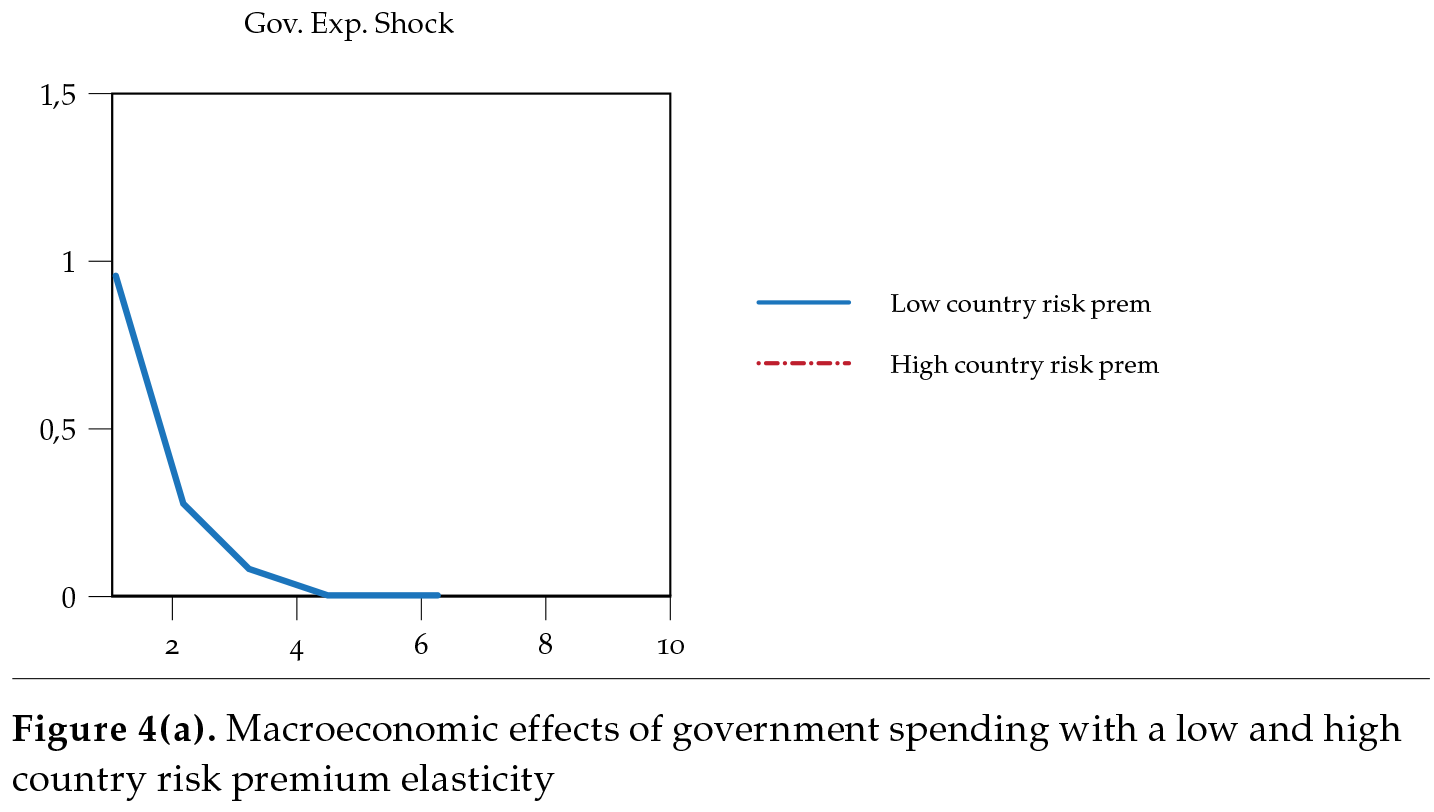

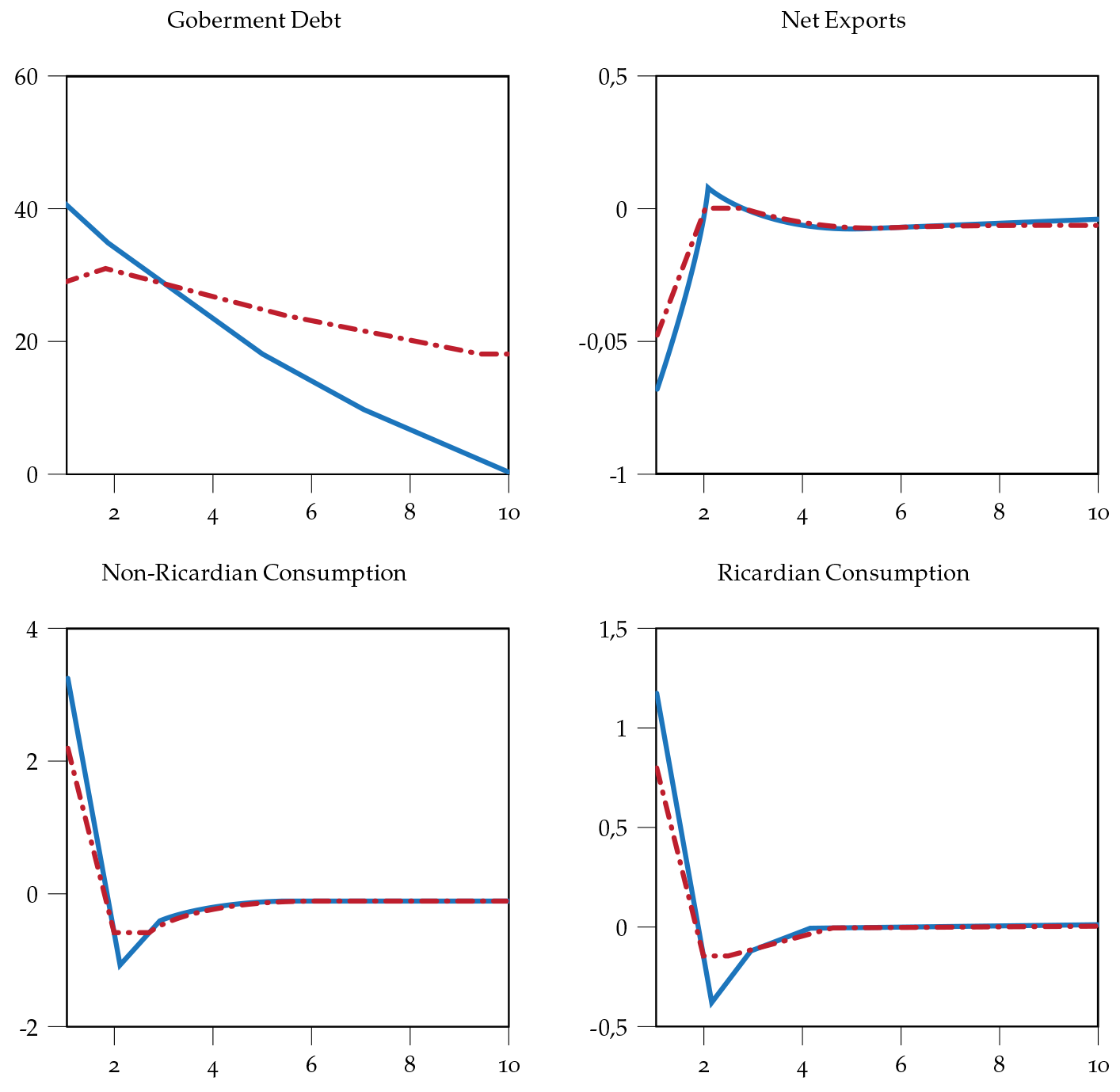

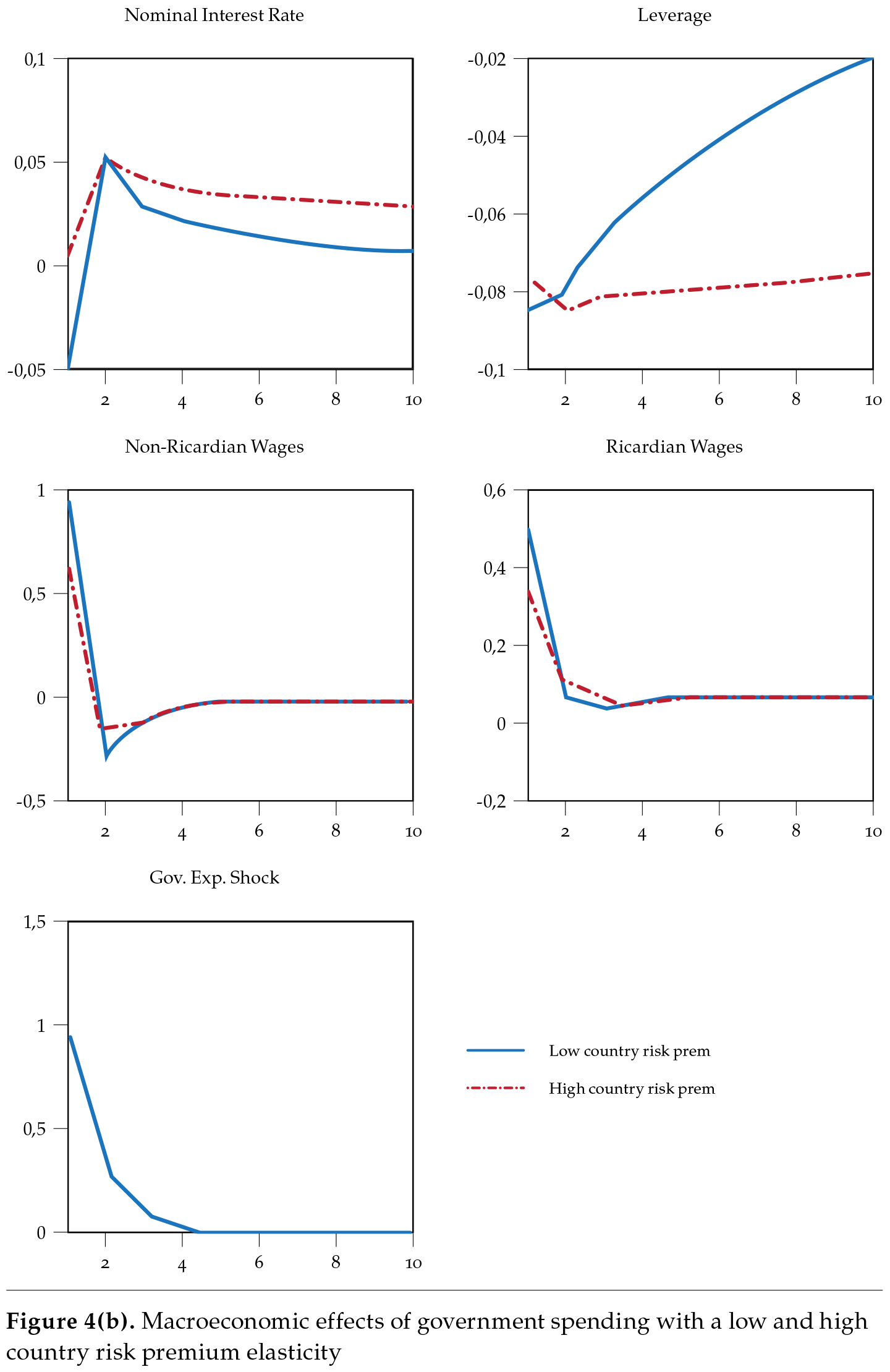

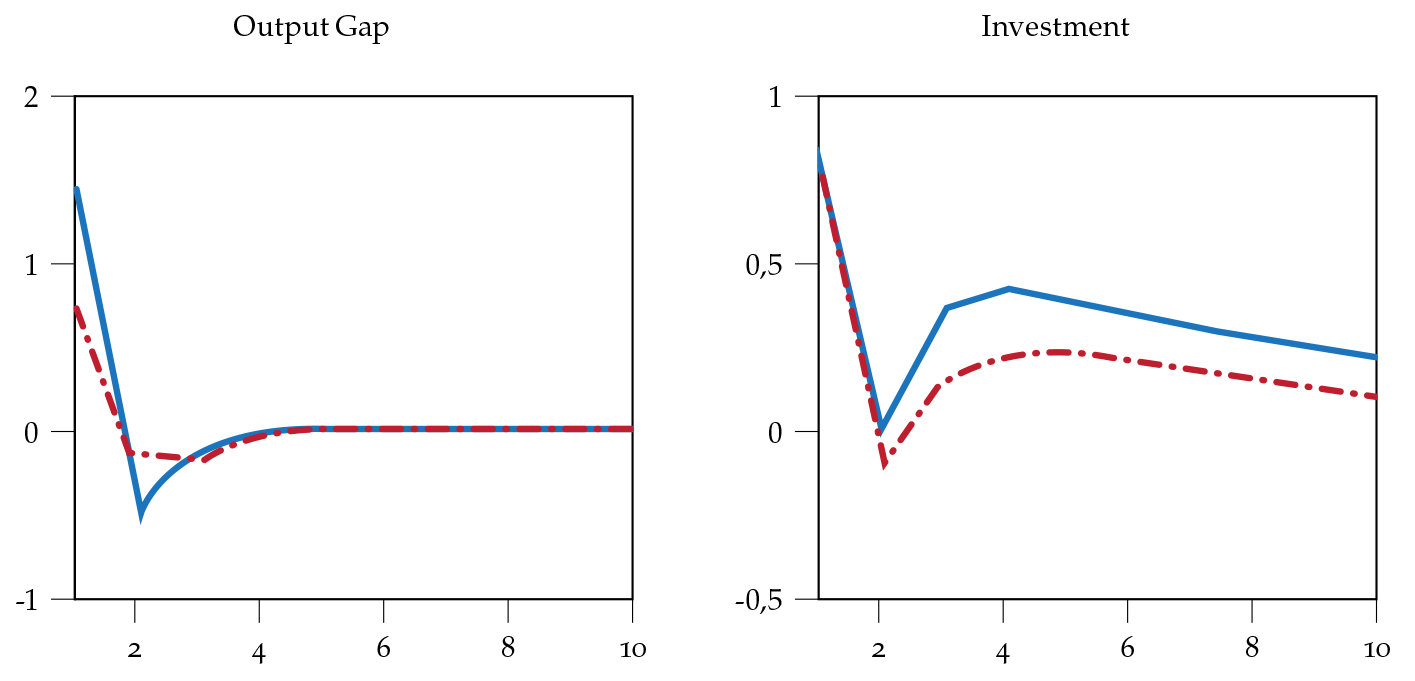

The other important aspect to take into account in a small open economy is the country risk premium that affects the uncovered interest parity condition. As mentioned in the introduction of the paper, many small open economies are often faced with high country risk premium shocks that increase the foreign interest rate that they have to pay for foreign debt. In our set up, we conduct a sensitivity analysis for different values of the parameter that represents the country risk premium φb. In our baseline calibration, this parameter was calibrated in 0.15. Now, we compare the results with a lower country risk parameter of 0.0015.

The results are presented in figures 4(a) and 4(b). As expected, when the country risk premium is low, the foreign interest rate that faces the country is lower with a consequent increase in the interest rate, a differential that causes a stronger appreciation of the real exchange rate. The price of imports and total inflation is lower than in the benchmark scenario of higher country risk premium, and the Central Bank responds with a lower real interest rate.

The later induces a higher price of capital and net worth and a lower external finance premium of entrepreneurs, which stimulates investment with a very high investment multiplier. Nonetheless, the impact on consumption is too moderated, which drives the small difference in the output multipliers.

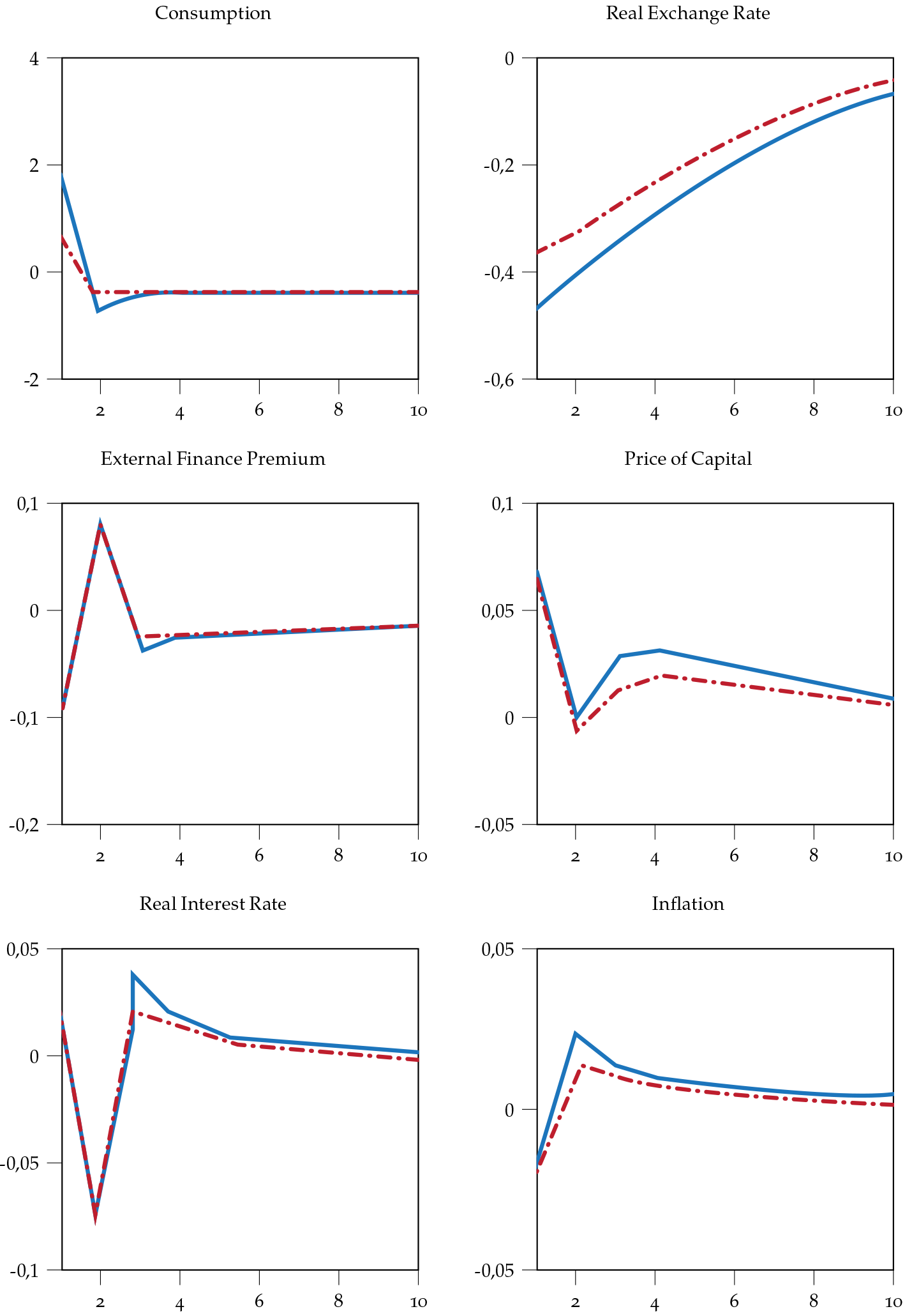

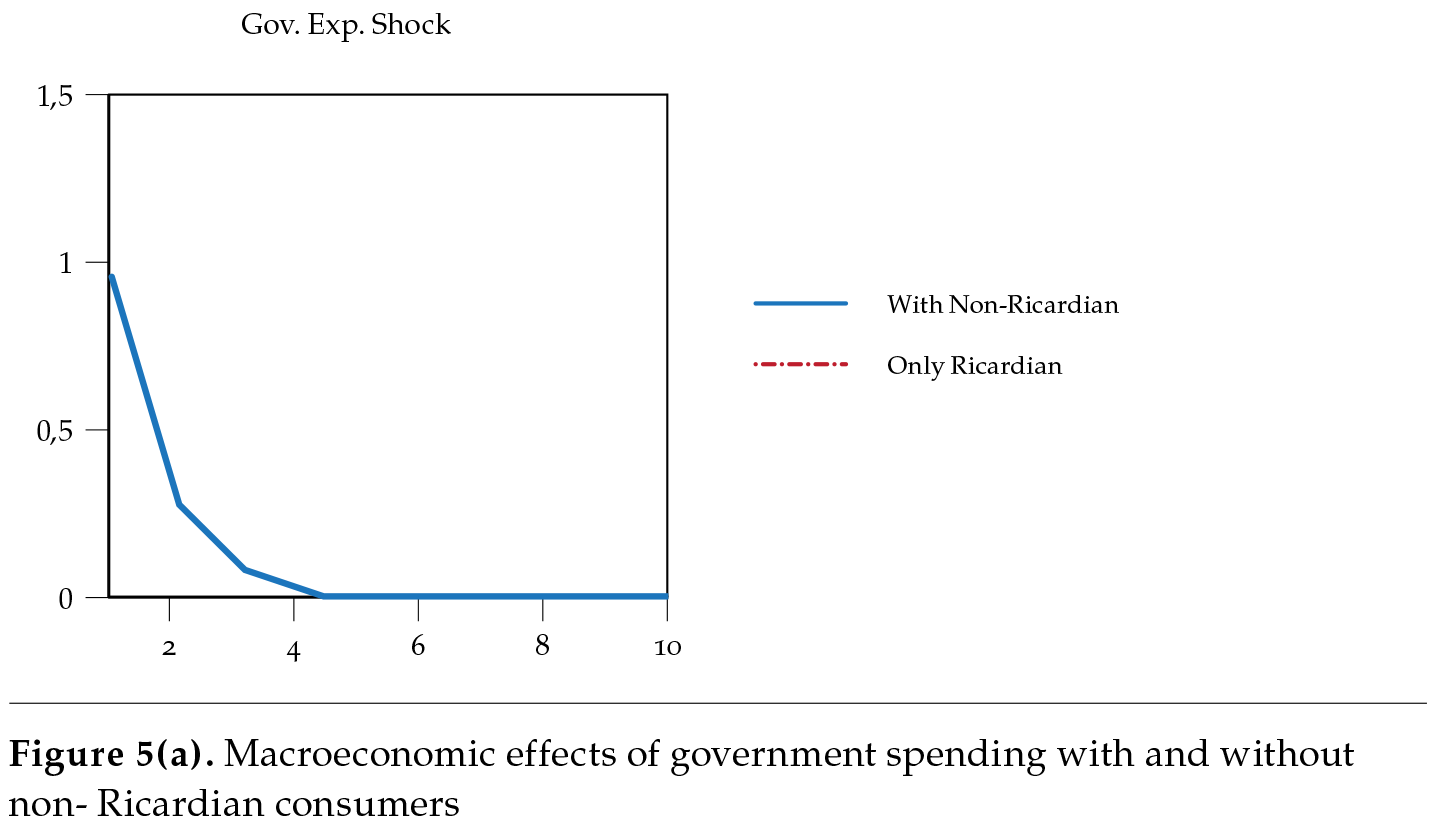

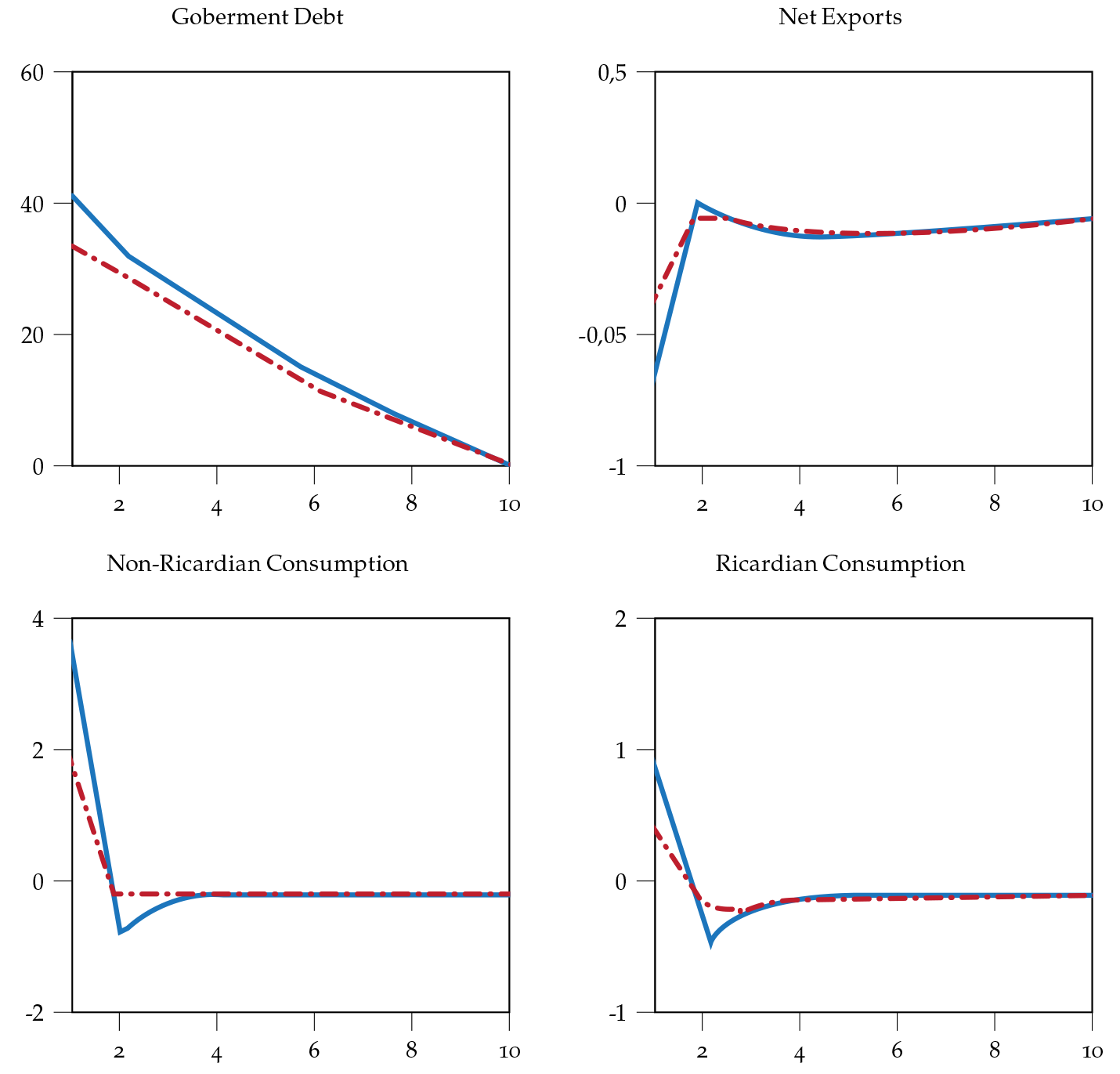

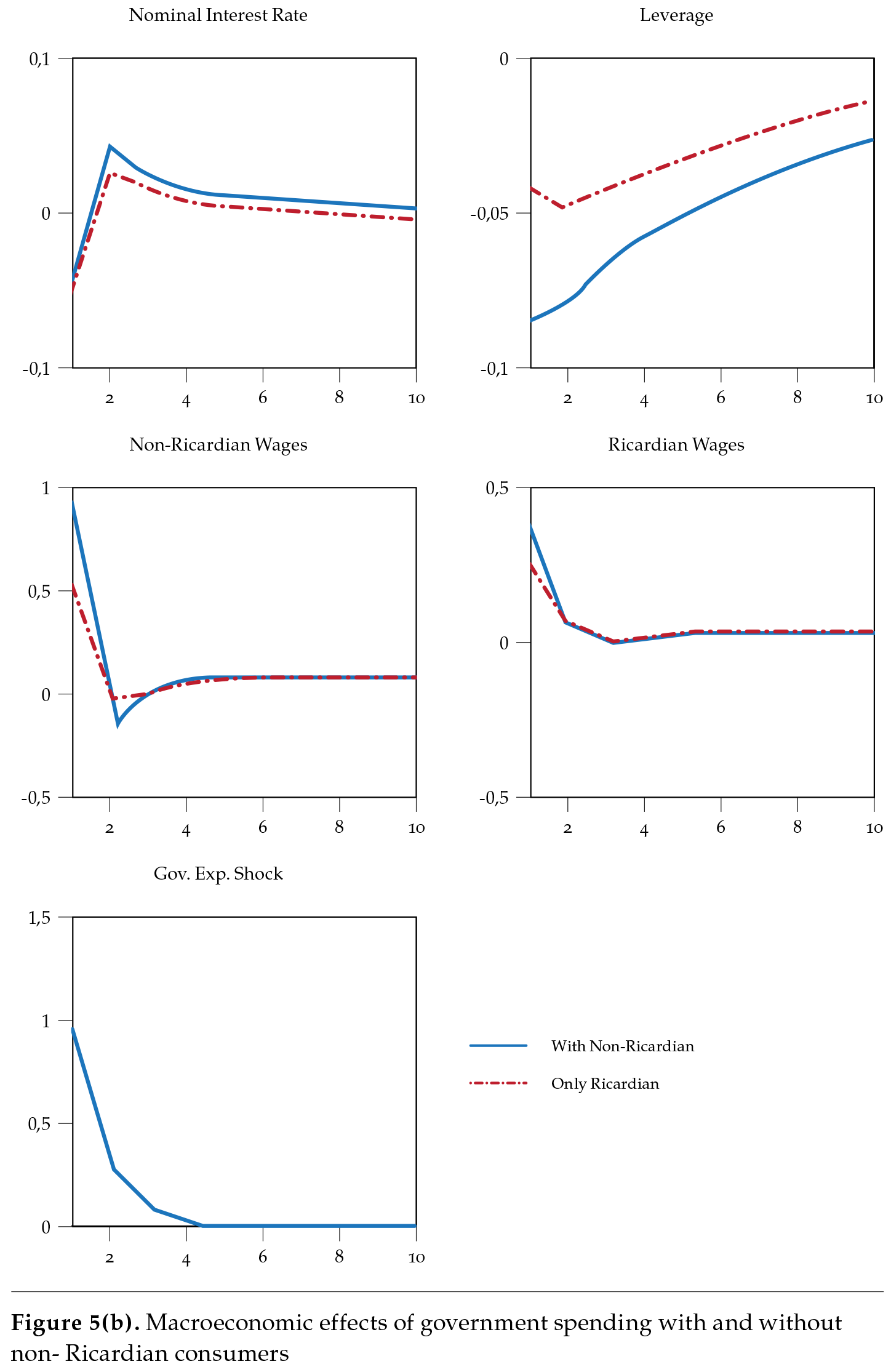

Without Non-Ricardian Consumers

Another essential channel that affects the size of fiscal multipliers in soeM is the presence of non-Ricardian consumers. In the models by Galí et al. (2007) and Colciago (2011), the fraction of non-Ricardian agents is the most influential parameter for the output, especially the consumption multiplier. The modeling of these agents allows replicating the empirical evidence of an increase in consumption when government expenditures increase not only in advanced but also in developing economies. But how important is this channel in the Colombian economy? Is the interaction between this channel and the real exchange rate important for the results?

In our calibration baseline, the fraction of non-Ricardian consumers is 0.8. For the model without non-Ricardian agents, we set up this parameter in 0.1. The results are plotted in figures 5(a) and 5(b). As expected, when the share of non-Ricardian agents is higher, their consumption is also higher, almost twice as big as in the absence of them. Total consumption is closer to the empirical evidence presented in section 2 as well as the output multiplier. However, the real exchange rate does not appreciate too much compared to the only Ricardian case. The results are similar with respect to the total inflation rates and nominal interest rates. As a consequence, balance sheets channels are similar, and investment does not differ very much between models.

Therefore, the channel is very important in terms of consumption and output for the Colombian economy but not in terms of the size of investment. The behavior of the real exchange rate is determinant in this result.

6. Conclusions

This paper highlights the importance that balance sheet effects have on investment and output in small open economies. The important role of asset prices on the net worth of firms and housing investment has a multiplier effect that is different if the model is characterized by nominal contracts. In the case that there are financial frictions but not a Fisher effect, a crowding out of the investment is present, and fiscal multipliers of investment, consumption, and output do not match the empirical evidence. In this regard, our findings are that in a soeM, the results by fv and cp still hold.

The openness of the economy plays an important role in the size of the multipliers. When the economy has low participation of imports in the consumption bundle, the fiscal multiplier of investment is high. The appreciation of the real exchange rate is high, and total inflation and real interest rate are low, improving the financial conditions for entrepreneurs. On the contrary, a high share induces an import-substitution away from domestic demand that reduces the fiscal multipliers. Similarly, if the economy faces a low country risk premium, the real exchange rate appreciates more than in the case of a high country risk premium, this, in turn, reduces real interest rates, increases the price of capital, deters the external finance premium, and pushes up investment.

Finally, our results suggest that there is not an important interaction between investment and consumption multipliers because of the presence of non-Ricardian consumers. The non-Ricardian case delivers higher consumption than the only Ricardian case, but financial conditions of investment prevail, delivering similar investment multipliers.

Acknowledgments

I thank Peter Ireland, Todd Walker, Eduardo Sarmiento Gómez, Hernando Vargas and to an anonymous referee for very useful comments to previous versions of this paper. We also thank Susana Otálvaro Ramírez for research assistance. The views expressed in the paper are those of the authors and do not represent those of the Banco de la República or its Board of Directors.

References

Bejarano, J. A. (2005). Estimación estructural y análisis de la curva de Phillips neokeynesiana para Colombia. Ensayos sobre Política Económica, 23(48), 63-116.

Bernanke, B. S., Gertler, M., & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. In J. Taylor, & M. Woodford (Eds.) Handbook of Macroeconomics Volume 1, (pp. 1341-1393). Elsevier.

Bonaldi, P., González, A., & Rodríguez, D. (2011). Importancia de las rigideces nominales y reales en Colombia: un enfoque de equilibrio general dinámico y estocástico. Ensayos sobre Política Económica, 29(66), 48-78.

Calvo, G. A. (1983). Staggered prices in a utility-maximizing framework. Journal of Monetary Economics, 12(3), 383-398.

Carrillo, J., & Poilly, C. (2013). How do financial frictions affect the spending multiplier during a liquidity trap? Review of Economic Dynamics, 16(2), 296-311.

Castro, G. L. D., Mourinho-Felix, R., Júlio, P., & Maria, J. R. (2014). Fiscal multipliers in a small euro area economy: How big can they get in crisis times? ceFAGe-UE Working Papers 14/7. Banco de Portugal.

Céspedes, L. F., Fornero, J. A., & Gali J. (2013). Non-ricardian aspects of fiscal policy in Chile. In L. F. Céspedes, & J. Galí (Eds.) Fiscal policy and macroeconomic performance Volume 17, (pp. 283-322). Central Bank of Chile.

Colciago, A. (2011). Rule of thumb consumers meet sticky wages. Journal of Money, Credit and Banking, 43, 325-353.

Corbo, V., & Schmidt-Hebbel, K. (1991). Public policies and saving in developing countries. Journal of Development Economics, 36(1), 89-115.

Dib, A., & Christensen, I. (2008). The financial accelerator in an estimated new Keynesian model. Review of Economic Dynamics, 11(1), 155-178.

Fergusson, L. (2003). Tributación, crecimiento y bienestar: El caso colombiano (1970-1999). Documentos ceDE 003662. Universidad de los AndesceDE.

Fernández, C., & Villar, L. (2014). Bonanzas temporales de recursos y producción manufacturera: una perspectiva global. Monetaria (cEMlA), 36(2), 177-232.

Fernández-Villaverde, J. (2010). Fiscal policy in a model with financial frictions. American Economic Review: Papers and Proceedings, 100, 35-40.

Freedman, C., Kumhof, M., Laxton, D., Muir, D., & Mursula, S. (2010). Global effect of fiscal stimulus during the crisis. Journal of Monetary Economics, 57, 506-526.

Galí, J., López-Salido, J. D., & Vallés, J. (2007). Understanding the effects of government spending on consumption. Journal of the European Economic Association, 5(1), 227-270.

García-Cicco, J., & Kawamura, E. (2015). Dealing with the Dutch disease: Fiscal rules and macro-prudential policies. Journal of International Money and Finance, 55, 205-239.

Gertler, M., Gilchrist, S., & Natalucci, F. (2007). External constraints on monetary policy and the financial accelerator. Journal of Money, Credit and Banking, 39(2-3), 295-330.

Goda, T., & Torres, A. (2015). Flujos de capital, recursos naturales y enfermedad holandesa: el caso colombiano. Ensayos sobre Política Económica, 33(78), 197-206.

González, A., López, M., Rodríguez, N., & Téllez, S. (2014). Fiscal policy in a small open economy with oil sector. Revista Desarrollo y Sociedad, 73, 33-69.

Greenwood, J., Hercowitz, Z., & Huffman, G. W. (1988). Investment, capacity utilization, and the real business cycle. American Economic Review, 78(3), 402-17.

Hamann, F., Lozano, I., & Mejía, L. F. (2011). Sobre el impacto macroeconómico de los beneficios tributarios al capital. Borradores de Economía 668. Banco de la República de Colombia.

Kumhof, M., & Laxton, D. (2013). Simple fiscal policy rules for small open economies. Journal of International Economics, 91(1), 113-127.

López, M. (2001). Seigniorage and the welfare cost of inflation in Colombia. Ensayos sobre Política Económica, 19(39), 114-131.

López, M., Prada, J. D., & Rodríguez, N. (2009). Evidence for a financial accelerator in a small open economy, and implications for monetary policy. Ensayos sobre Política Económica, 27(60), 12-45.

Monacelli, T., & Perotti, R. (2010). Fiscal policy, the real exchange rate and traded goods. Economic Journal, 120(544), 437-461.

Mountford, A., & Uhlig, H. (2009). What are the effects of fiscal policy shocks? Journal of Applied Econometrics, 24(6), 960-992.

Pieschacón, A. (2012). The value of fiscal discipline for oil-exporting countries. Journal of Monetary Economics, 59(3), 250-268.

Prada, J. D., & Rojas, L. E. (2009). La elasticidad de Frisch y la transmisión de la política monetaria en Colombia. Borradores de Economia 555. Banco de la Republica de Colombia.

Ramey, V. A. (2011). Identifying government spending shocks: It’s all in the timing. The Quarterly Journal of Economics, 126(1), 1-50.

Ravn, M. O., Schmitt-Grohé, S., & Uribe, M. (2007). Explaining the effects of government spending shocks on consumption and the real exchange rate. NBEr Working Papers 13328. National Bureau of Economic Research Inc.

Sarmiento, E., & López, M. (2016). Dutch disease exchange rate incidence over profits of traded and nontraded goods. Monetaria, IV(1), 41-75.

Schmitt-Grohé, S., & Uribe, M. (2003). Closing small open economy models. Journal of International Economics, 61(1), 163-185.

Sin, J. (2016). The fiscal multiplier in a small open economy: The role of liquidity frictions. IMf Workig Paper 16/138. International Monetary Fund.

Smets, F., & Wouters, R. (2007). Shocks and frictions in US business cycles: A bayesian DSGe approach. American Economic Review, 97(3), 586-606.

Vargas, H., González, A., & Lozano, I. (2012). Macroeconomic effects of structural fiscal policy changes in Colombia. In Bank for International Settlements (Ed.) Fiscal policy, public debt and monetary policy in emerging market economies Volume 67, (pp. 119-160). Bank for International Settlements.