Effects of Booms and Oil Crisis on Colombian Economy: A Time-Varying Vector Autoregressive Approach*

Efectos de los auges y las crisis del petróleo en la economía colombiana: un enfoque con vectores autorregresivos cambiantes en el tiempo

Efeitos dos auges e as crises do petróleo na economia colombiana: um enfoque com Vetores Autorregressivos variáveis no tempo

Effects of Booms and Oil Crisis on Colombian Economy: A Time-Varying Vector Autoregressive Approach*

Revista de Economía del Rosario, vol. 23, no. 1, 2020

Universidad del Rosario

Received: 13/09/2019

Accepted: 08/11/2019

Additional information

To quote this article: Melo-Becerra, L.A., Parrado-Galvis, L.M., Ramos-Forero, J.E., & Zarate- Solano, H.M. (2020). Effects of Booms and Oil Crisis on Colombia Economy: A Time-Varying Vector Autoregressive Approach. Revista de Economía del Rosario 23 (1), 31-63. Doi: https://doi.org/10.12804/revistas.urosario.edu.co/economia/a.8631

Abstract:

The aim of this paper is to estimate the impact of price and oil production shocks on macroeconomic variables such as public debt, real exchange rate, and Colombian economic activity. This country depends to a large extent on oil exports, which could lead to different obstacles in macroeconomic management when prices and oil production record fluctuations. The paper first describes the importance of oil in Colombia, which went from being a completely-importing country in 1976 to an oil-exporting economy in 1986. The empirical analysis uses a time-varying vector autoregressive methodology, which assumes that the relation between prices and oil production with macroeconomic variables changes dynamically. The results confirm that there are different stochastic volatility patterns of the variables included in the model. According to the impulse response functions, positive oil price shocks did not cause significant effects on the real exchange rate or on government debt. However, the negative price shock in 2015 led to a real depreciation and an increase in public debt. JEL classification: C35, C36, I10, J21.

Keywords: Oil shocks, Colombia, public finances, tpv-var.

Resumen:

El propósito de este documento es estimar el impacto de los choques de precios y producción de petróleo en variables macroeconómicas como la deuda pública, el tipo de cambio real y la actividad económica colombiana. Este país depende en gran medida de las exportaciones de petróleo, lo que podría conducir a diferentes obstáculos en el manejo macroeconómico cuando los precios y la producción de petróleo registran fluctuaciones. El documento describe la importancia del petróleo en Colombia, que pasó de ser un país completamente importador en 1976 a una economía exportadora de petróleo en 1986. El análisis empírico utiliza una metodología de vectores autorregresivos con parámetros cambiantes en el tiempo, que supone que la relación entre los precios y la producción de petróleo con las variables macroeconómicas cambia dinámicamente. Los resultados confirman que existen diferentes patrones de volatilidad estocástica de las variables incluidas en el modelo. De acuerdo con las funciones impulso-respuesta, los choques positivos del precio del petróleo no causaron efectos significativos en el tipo de cambio real ni en la deuda pública. Sin embargo, el choque negativo de los precios en 2015 condujo a una depreciación real y a un aumento de la deuda pública. Clasificación JEL: C35, C36, I10, J21.

Palabras clave: choques petroleros, Colombia, finanzas públicas, var-pct.

Resumo:

O propósito deste documento é estimar o impacto dos choques de preços e produção de petróleo em variáveis macroeconômicas como a dívida pública, a taxa de câmbio real e a atividade econômica colombiana. Este país depende em grande medida das exportações de petróleo, o que poderia conduzir a diferentes obstáculos no manejo macroeconômico quando os preços e a produção de petróleo registam flutuações. O documento descreve a importância do petróleo na Colômbia, que passou de ser um país completamente importador em 1976 a uma economia exportadora de petróleo em 1986. A análise empírica utiliza uma metodologia de Vetores Autorregressivos com parâmetros variáveis no tempo que supõe que a relação entre os preços e a produção de petróleo com as variáveis macroeconomias muda dinamicamente. Os resultados confirmam que existem diferentes patrões de volatilidade estocástica das variáveis incluídas no modelo. De acordo com as funções impulso-resposta, os choques positivos do preço do petróleo não causaram efeitos significativos na taxa de câmbio real, nem na dívida pública. No entanto, o choque negativo dos preços em 2015 conduziu a uma depreciação real e a um aumento da dívida pública. Classificação JEL: C35, C36, I10, J21.

Palavras-chave: choques petroleiros, Colômbia, finanças públicas, var-pct.

Introduction

Since the mid-1980s, oil has played an essential role in the Colombian economy due to the improvement of the productive capability and the resumption of oil exports. The importance of oil became evident in the 1990s and from 2004 to 2014 because of the boom in oil prices and quantities. Due to the relevance of oil in the Colombian economy, the fall of the international oil price since mid-2014 caused macroeconomic imbalances, which are still in the process of adjustment. In general, oil shocks have affected Colombia’s finances, destabilizing the balance of payments and influencing levels of private consumption and investment. The relationship between oil indicators and the macroeconomic context has remained unstable over the last 30 years.

The Colombian oil industry developed during a period of institutional and legal development characterized by significant fluctuations of both international oil prices and worldwide production. These factors have determined the impact of oil shocks on the Colombian economy, which can be characterized based on the evolution of some key economic variables and the behavior of the principal industry figures. In the 1990s, the production boom resulting from new oil discoveries had less impact on public finances and the external sector than the price-production boom observed since 2004. In the latter context, the oil industry acquired a leading role in the economy. Because of its importance, the recent changes in international oil prices has caused considerable imbalances, especially in the fiscal posture.

The aim of this paper is to estimate the impact of oil price or production shocks on macroeconomic variables such as the real exchange rate, private investment and consumption, and public debt over the last 30 years. To measure this impact, we use an econometric methodology based on autoregressive vector models that consider the dynamic relationship between oil price/ production and macroeconomic variables. This model is known in recent literature as tvp-var. The relevance of this methodology is that it accounts for changes in the volatility of oil price/production shocks and assumes that the relationship between prices and oil production with macroeconomic variables changes dynamically.

This paper contains seven sections apart from this introduction. In section 1, we describe the historical importance of oil to the Colombian economy and its evolution through time. In section 2, we explain the transmission channels of oil shocks in the macroeconomic setting. In section 3, we describe the econometric methodology, which bases on mixed time-varying autoregressive vectors. The data and the procedure used for the statistical inference are explained in section 4. In section 5, we summarize the main results, including impulse response functions. Finally, we present our conclusions.

1. Oil in the Colombian Economy

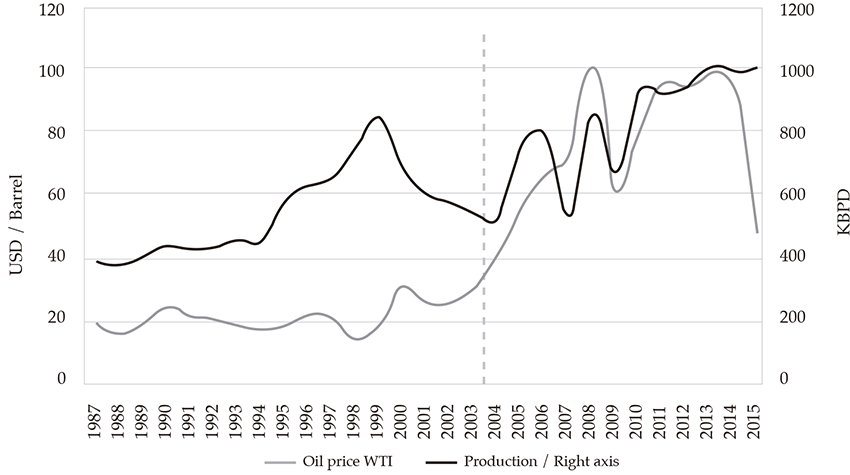

Oil became significant to the Colombian economy at the beginning of the twentieth century with the Barco and de Mares concessions granted by the Colombian state. The scarcity of capital and technology led to the transfer of these concessions to multinational companies that exploited this natural resource. During the first half of the twentieth century, most of the oil production went to domestic consumption (Perry & Olivera, 2012). At the end of the 1960s, the depletion of oil reserves was evident. Thus, it was necessary to introduce adjustments to the national legislation in order to encourage exploratory activity (Perry & Olivera, 2012). Nevertheless, in the early 1970s, Colombian oil production declined drastically, and in 1974, the country became a net importer. During the same period, international oil prices increased rapidly, from close to 3 usd per barrel in 1973 to close to 37 usd per barrel in 1980. As a result of the crisis, the Colombian government issued a regulatory framework to stimulate oil exploration in order to recover the country’s production capacity. These adjustments caused an increase in exploratory activity and foreign investment in the sector. In 1983, the Caño Limón field was discovered, which allowed for the recovery of Colombia’s productive capability, the growth of the oil reserves, the fulfillment of domestic oil demand, and the resumption of exports (Perry & Olivera, 2012).

Later, the Cusiana (1988) and Cupiagua (1992) fields were discovered. These findings raised oil production from 450 kbpd in 1993 to close to 850 kbpd in 1999. In 1995, the government created an Oil Savings and Stabilization Fund as a mechanism to smooth the impact of increasing oil revenues. Over the last 30 years, oil variables have registered important changes in Colombia’s economic performance. Indeed, since the late 1980s, new discoveries have increased oil reserves, and its production has consistently increased, reaching as much as 800 kbpd in 1999, the period in which the international crude oil price wti fluctuated at around 20 usd per barrel.

Simultaneously, exploratory activity consistently decreased due to the reduction of foreign direct investment in this sector. In this period, the real exchange rate appreciated until 1997, and the share of oil and its derivatives in the country’s exports increased from 15 % in 1994 to 32 % in 1999. Moreover, fiscal revenues from oil accounted for about half a percentage point of gdp in national fiscal accounts and in oil royalties transferred to regions.1 At the beginning of the first decade of the 2000s, there was a reduction in the exploratory activity, as oil production gradually declined to levels lower than 600 kbpd in 2003. At the same time, the oil price has experienced an upward trend since 2000, fluctuating at around 30 usd per barrel. Government revenues attributable to oil activity accounted for about 1 % of gdp in 2001 and declined to 0.7 % of gdp in 2003.

Since 2003, international oil prices have increased gradually to reach a peak of 100 usd per barrel in 2008. However, in 2009, the economic stress caused by the international financial crisis temporarily decreased the price to 60 usd per barrel, cutting off the upward trend. In the following years, oil prices recovered levels above 90 usd per barrel, until 2014, when the global increase of crude supply and the decline in the demand for commodities pushed the oil price downward. At the end of 2015, crude oil price wti reached a value of 49 usd per barrel. The spike in the oil price since 2003 encouraged oil production that, with booms and busts, gradually increased until settling around one million daily barrels per day between 2013 and 2015. The recent drop in prices has reduced oil exploration activities.

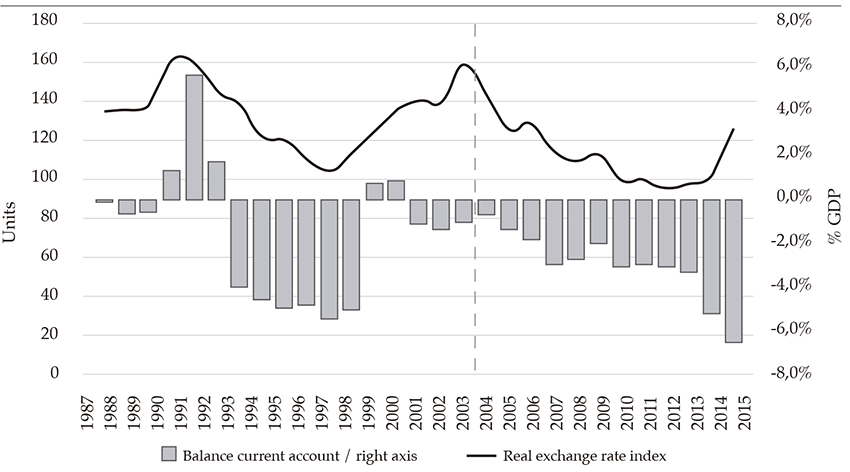

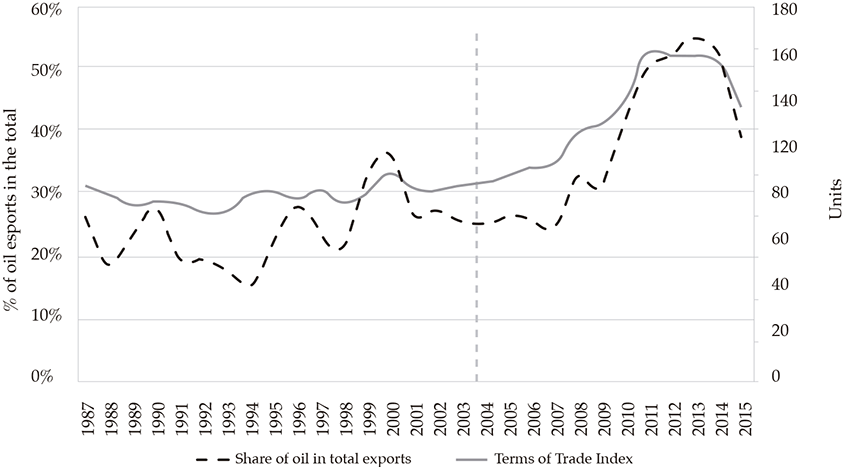

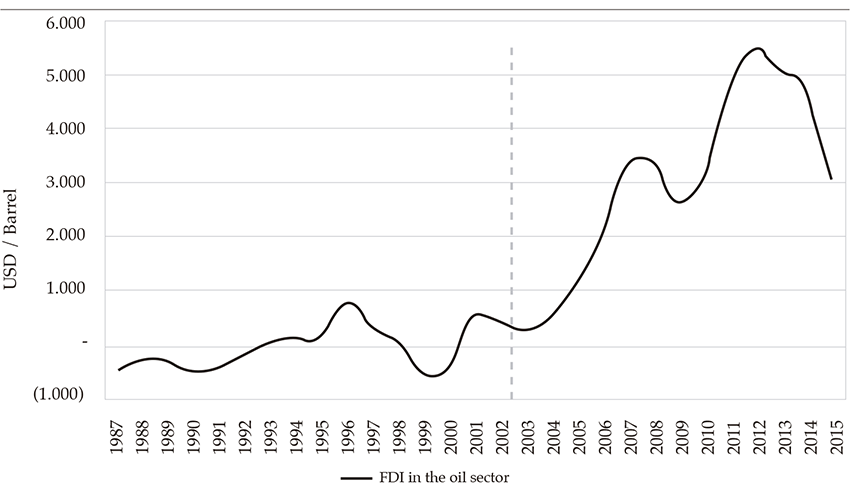

The increase in price and production resulted in higher shares of the oil and its derivatives in Colombia’s total exports, accounting for about 50 % in 2011 and 55 % in 2013. With the decline in crude price, this share decreased to 40 % in 2015. In turn, the oil boom improved the country’s trade terms and increased the flow of foreign direct investment, which, in turn, pushed the real exchange rate up, which caused an appreciation from 2004 to 2012. The recent drop in prices generated a depreciation of the real exchange rate during 2014 and 2015 (Appendix A).

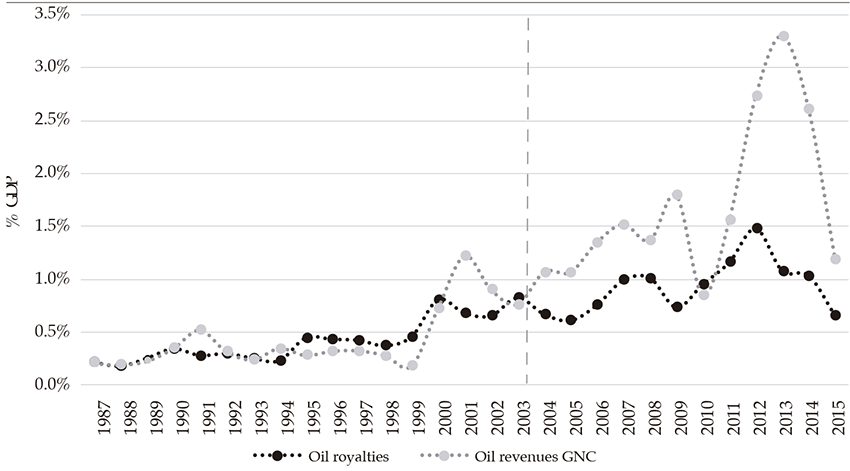

The oil boom during the last few years has produced a critical flow of resources to the public sector that has significantly exceeded those of the 1990s.

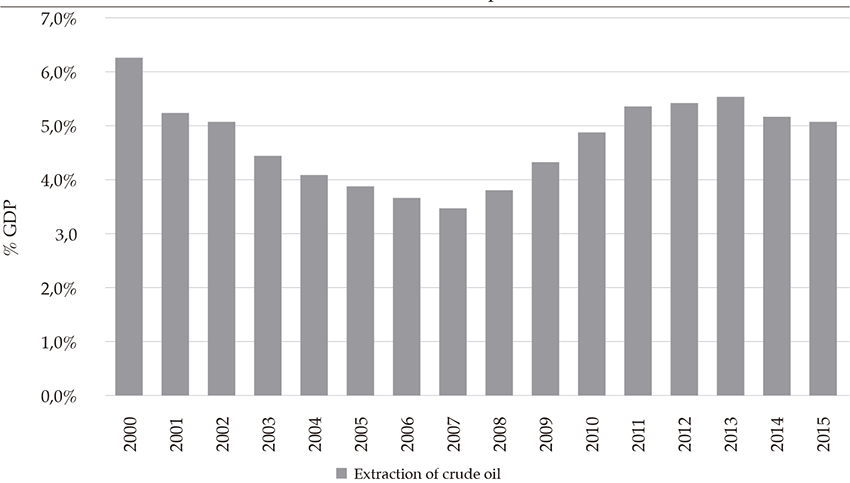

Government revenues from oil, mainly compounded by dividends distributed by the Colombian oil company (Ecopetrol) and taxes from the sector, increased from 0.8 % of gdp in 2002 to 1.8 % gdp in 2009. After a transitory reduction in 2010, these revenues continued to grow to account for about 3.3 % of gdp in 2013 and fell to 1.2 % of gdp in 2015. Likewise, oil royalties, which constitute a source of income to regional governments, rose from 0.6 % of gdp in 2005 to 1 % of gdp in 2008. After a decline in oil royalties due to the international financial crisis, they increased to 1.5 % of gdp in 2012. According to the economic activity, the share of the oil sector in the value of production fell from 5.3 % to 3.4 % of gdp between 2001 and 2007. Later, in the boom years (2011- 2014), the share grew up to 5.6 % of gdp (appendix A).

Summing up, the impact of the oil boom in recent years was bigger than that observed in the oil boom of the 1990s due to the higher international oil prices. These prices stimulated exploration, foreign direct investment in the sector, and oil production. The evolution of these variables contributed to increasing the share of oil in the total of exports to above 50 %, improved the trade terms, and generated a significant flow of public revenues to central and regional governments.

2. Transmission channels

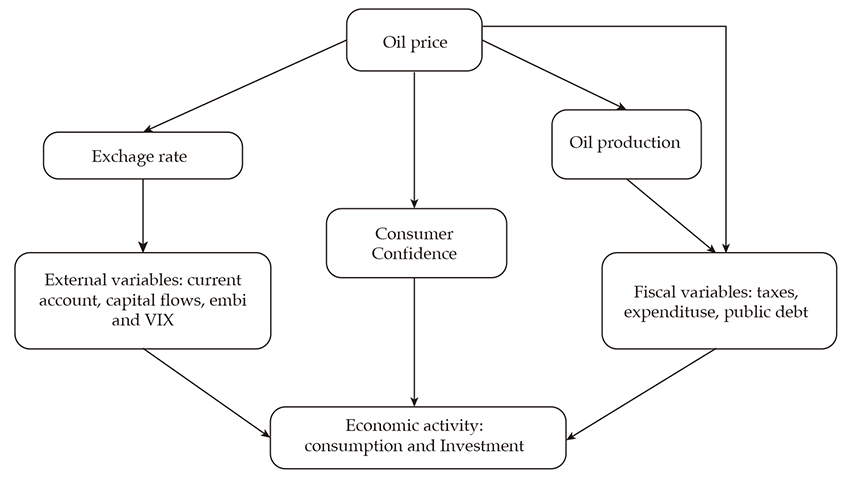

In this section, we describe the main transmission channels of oil prices and production shocks in a small open economy, considering different macroeconomic variables (figure 1). Commodities exporting countries face challenges arising from the upturn and decline of wealth due to elevated price and production fluctuations. These challenges are associated with the side effects of oil shocks on economic activity, government finances, the exchange rate, and the balance of payments.

A commodity price/production boom is associated with the phenomenon known as Dutch disease, which refers to a process of resource reallocation that ends with the reduction of the production of tradable goods other than commodities and with the increase of it and demand of non-tradable goods (Sachs & Larraín, 1994). The main mechanism induced by the process is the appreciation of the real exchange rate, which reduces competitiveness and the profitability of industrial and agricultural activities linked to the international trade and economic sectors that compete with imported goods (Puyana & Thorp, 1998).

The boom leads to an adjustment of revenues and external accounts due to the increase in the value of oil exports, and capital flows from foreign direct investment. Foreign trade earnings increase the accumulation of currencies and generate a process of the real exchange rate appreciation, enhancing imports, and eroding the exports of commodities and manufactured goods, resulting in imbalances of the current account. In the middle term, the exchange rate adjustment upgrades the current account due to more expensive imports and the improvement of industrial and agricultural export goods.

From the fiscal point of view, commodity price or production booms increase the flow of revenues from taxes, royalties, and dividends over oil company profits. Some countries depend more heavily on these revenues than others, and therefore they are more vulnerable to fluctuations in commodity prices and discoveries of new resources. The management of transitory incomes derived from the mining sector fundamentally depends on the institutional development of the country. For instance, while some countries set up savings funds for macroeconomic stabilization, others allocate additional resources to increasing budgetary expenditures through public consumption and investment, attending to social needs, and improving infrastructure (Perry, Bustos & Sui-Jade, 2011). The fiscal management problem arising in booms is the potential to fund permanent spending with transitory revenue, which can decline or disappear, generating fluctuations in the stock of public debt.

In turn, the depletion of resources or the decrease in international prices shrinks the economic activity, requiring an adjustment in government finances and the current account. The extent to which a negative shock to oil prices reduces public revenues and affects the trade balance depends on the share of the mining sector in total exports (Baffes, Kose, Ohnsorge & Stoker, 2015).

This fact could lead to a depreciation of the real exchange rate that can be partially mitigated through the release of short-run capital and the reduction of foreign investment in the mining sector.

The devaluation of the exchange rate from a negative commodity shock affects the dynamics of prices, the valuation of the external debt in domestic currency, and the cost of serving the debt. In general, the decline in commodity prices could lead to a capital exit, the weakening of fiscal accounts, an increase of debt spread, the loss of international reserves, and the reduction of economic activity, among other effects. Likewise, the shock might hinder the access of the country to international financial markets downgrading the banking indexes due to the loss of dynamism in production and the exposure of some financing institutions to mining activities. Oil shocks also affect the external sector through the sovereign risk premium, measured by the Emerging Markets Bonds Index (embi).

In terms of economic activity, changes in oil prices and production have an effect on consumption and private investment, depending on the share of the oil sector in the gdp and the expectations of agents in the economic performance in the short and middle term. Moreover, a negative oil price shock reduces national and foreign investors as well as consumer confidence.

3. Econometric methodology

In this section, we describe our empirical strategy, which considers the relationship between prices or oil production with macroeconomic and fiscal variables. It is worth noting that this relationship has been unstable since the end of the 1980s. Therefore, the econometric analysis considers two key elements. The first is associated with changes in the volatility of the shocks of prices and oil production between 1987 and 2015. The second takes into account the various forms of the response of macroeconomic variables to price and production oil shocks, which requires consideration of changes in the transmission mechanisms during the period. Thus, the selected methodology is based on multivariate autoregressive vector parameters and changing volatility over time (tvp-var).

Unlike other studies that assume constant shock effects or homogeneous variances over time, the tvp-var model can incorporate asymmetries and nonlinearities from shocks and their effect on the structure of lags of the model, ensuring the consistency of the estimators. This method provides data for the identification of structural shocks. Additionally, in this paper, considering the empirical strategy and the transmission channels of prices and oil production shocks provided in Figure 1, the ordering of the variables before implementing the tvp-var considers the innovations of the oil price shocks weakly exogenous, reflecting the Colombian oil market.2 The econometric methodology considers the joint behavior of variables with coefficients, parameters, and stochastic volatility that change over time as follows:

(1)

(1)Where yt is the set of endogenous variables properly transformed to explain the relationship of the variables of price and production of oil with the selected macroeconomic ones, considering the transmission channels explained in the previous section.

Where ct is a vector of intercepts, Bi,t i = 1,…, . correspond to matrices of coefficients, and Σt is the matrix with standard deviations, σt. In turn, Atis a lower triangular matrix with α. parameters that form a vector of coefficients, and εt is the vector of unobservable shocks with normal distribution εt ~ N(0,1k).

All the vectors and matrices defined above change over time. In addition, following Primiceri (2005), parameters Bi,t, αt and log(σt) are assumed to follow a process of random walk in the following way:

(2)

(2)

(3)

(3)

(4)

(4)Furthermore, the assumption made is that all errors in the model come from a normal joint distribution:

The statistical methodology to estimate parameters and functions is based on Bayesian methods. The tvp-var model includes a number of parameters that change over time, which hinders the use of parametric methods given the complexity of the models. An appropriate estimation procedure is based on the simulation methods of Monte Carlo with Markov Chains (mcmc) attached to the Bayesian methodology. This procedure initially sets the prior joint distribution of the parameters function and then updates it with the data likelihood function, which generates the posterior probability function for the parameters. Because this function is analytically intractable, the mcmc algorithm allows us to generate the respective samples for the analysis of statistical inference.

In the tvp-var model, parameters are considered latent variables; therefore, we can set a state-space model. Unobservable states correspond to the history of the volatilities, Σt, the history of the coefficients (BT, AT ). The Bayesian methodology leads to reductions in uncertainty about the parameters and evaluates the posterior distribution for parameters B, A,Σ, and the hyperparameters of V. The advantage of this approach lies in the efficiency of the estimates when the model has several parameters, and there are asymmetries and nonlinearities in the analyzed model.

In this paper, following Nakajima, Kasuya, and Watanabe (2011), statistical inference is based on the application of mcmc methods, of which the Gibbs sampling is a variant. With this method, the samples for the parameters are obtained from the full conditional distributions of each parameter, which are smaller than the joint distribution of them; although, for some parameters of this distribution, they are intractable. Thus, the mcmc or Gibbs Sampler is an iterative algorithm that builds a sequence-dependent on the values of the parameters with distributions converging with the posterior distribution.

We base our choice of prior distributions for the parameters on earlier studies (Primiceri, 2005; Nakajima, Kasuya & Watanabe, 2011) and in accordance with standard distributions associated with the form of the parameters. It is worth noting that the distributions for the hyper-parameters of the components of the matrix of variances and covariances V: Q, W, and the block of S are distributed as independent inverse-Wishart. Moreover, the priors for the initial states of the time-varying coefficients, B0, simultaneous relations, α0, and the logarithm of the standard errors, log (σ0) are assumed to follow the Gauss distribution. These assumptions imply that the distributions for the complete sequences B, α, Log (σt) conditional on Q, W, and S- also follow the normal distribution. Specifically, a priori distributions have the following form:

(5)

(5)

(6)

(6)

(7)

(7)

(8)

(8)

(9)

(9)The joint distribution of  is given by:

is given by:

(10)

(10)Where the rectangular parenthesis is interpreted as the probability distribution, and the symbol α expresses proportionality. The proposed algorithm by Primiceri (2005) and Nakajima, Kasuya, and Watanabe (2011) generates samples of  in the following way:

in the following way:

1. Sample ΣT from

2. Sample (θ, sT) from

2.a. Sample θ from

2.b. Sample sT from

4. Data and estimation procedure

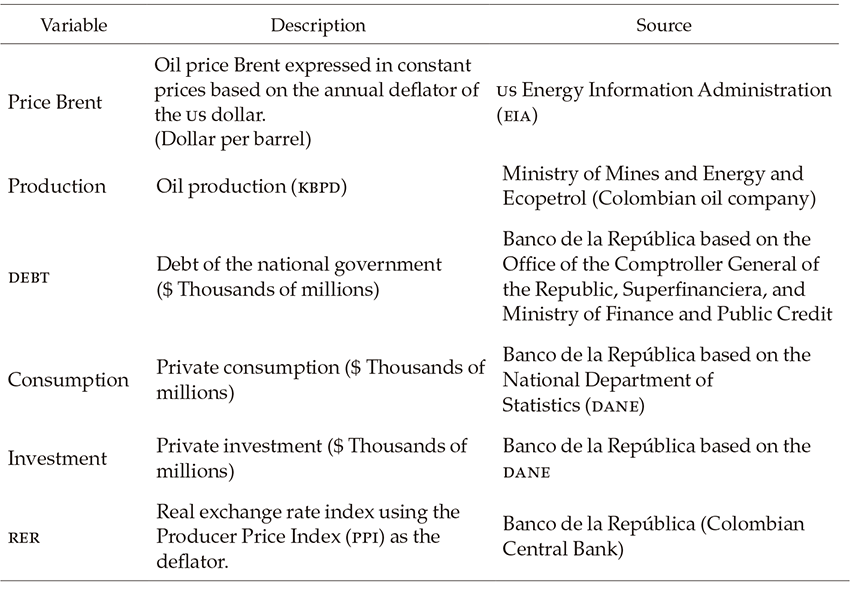

This section describes the data and presents the estimated parameters based on the tvp-var. Bayesian program explained in Nakajima, Kasuya, and Watanabe (2011). The initial dataset consists of variables with different frequencies. Oil price and production and the real exchange rate have a monthly frequency for the period 1985M1 to 2015M12. Moreover, the government’s debt, private consumption, and investment are available with quarterly frequency for the period 1985T1 to 2015T4. Table 1 describes the variables with their respective sources.

In order to accurately measure the impact of oil shocks on the macroeconomic variables, we rely on impulse response functions from observable data by using the tvp-var models for mixed frequencies, following Marcellino and Schumacher (2010). In this paper, we adopt the methodology of missing observations for high-frequency data, interpolating the quarterly series at monthly intervals according to the strategy that Chow and Lin (1971) initially proposed.

The implementation of the tvp-var methodology with mixed frequencies was carried out following the standard analysis on the characteristics of the time series considered in the model. Following Enders (2008), we conducted statistical tests of the unit root proposed by Dickey-Fuller augmented (adf) for the seasonally adjusted series, using a selection scheme of the deterministic regressors. Additionally, we performed the Kwiatkowski, Phillips, Schmidt, and Shin (kpss) test. The main results are presented in appendix B. Based on the theoretical aspects presented in section 3, we specified the order of the tvp-var model recursively in the following way: price, production, itcr, consumption, investment, and national government debt.

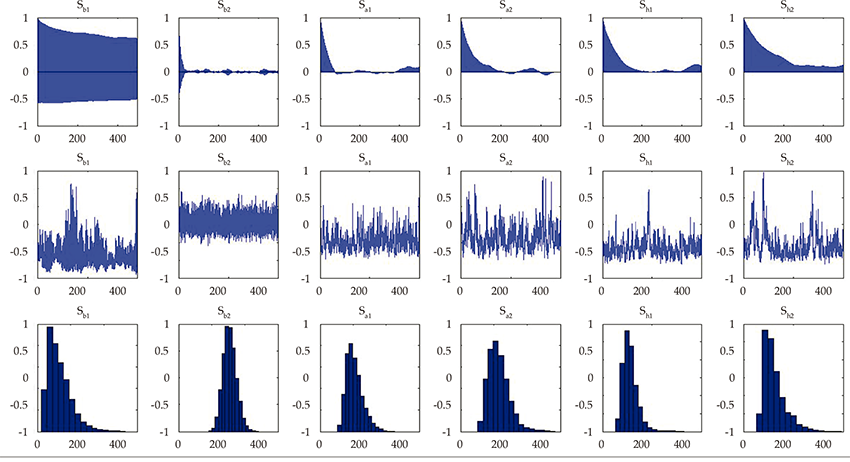

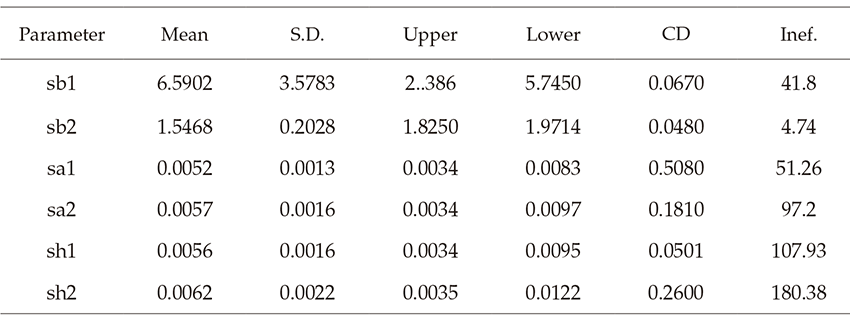

According to the Bayesian statistical inference procedure based on the Gibbs sampling, we generated 10000 samples, discarding the first thousand. The sample autocorrelation functions, the trajectory of the sample, and the posterior density for some selected parameter functions are presented in appendix C. After disposing of the training period, it is observed that the trajectory is stable, which indicates that the chain produced non-correlated samples for almost all the parameters. Even though the autocorrelation function for the sb1 parameter exhibits a high correlation when using the full chain, it was reduced when we thinned the chain (Owen, 2017). Appendix D shows estimates of the parameters posterior mean, their standard deviations, the 95 % credible interval, the diagnosis of convergence with the cd statistic, and the inefficiency factor proposed by Geweke (1992). Based on these statistics, we failed to reject the null hypothesis of convergence to the posterior distribution. The inefficiency factor is low relative to the number of samples, which indicates that the posterior sampling is efficient.

5. Results and discussion

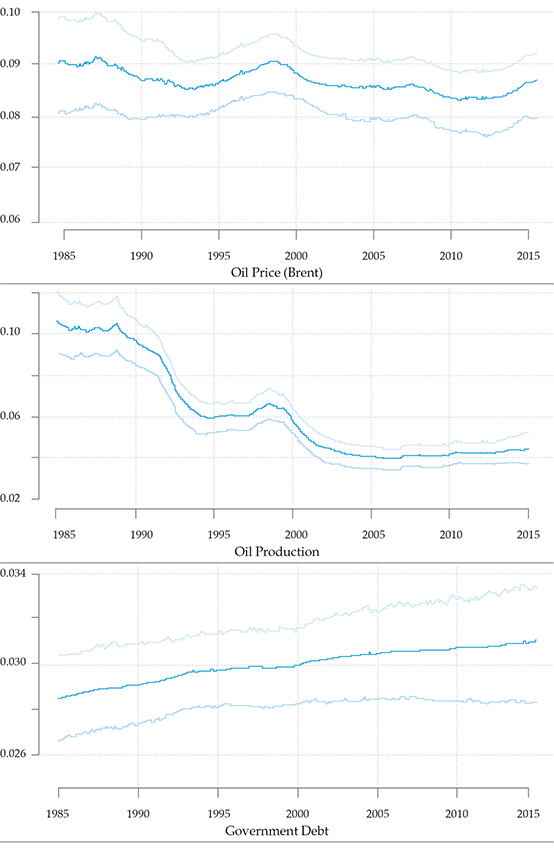

In this section, we present the main results of the tvp-var model. First, we describe the evolution of volatilities of the essential oil variables affected by the shocks in the period analyzed. Second, the impulse-response functions for some relevant selected dates are analyzed. Figure 2 depicts the stochastic volatility of structural shocks for the six variables considered in the tvp-var model. Figures include the confidence interval computed for the 16th and 84th quantiles of the standard deviation of the shock.

According to the dynamics of the volatilities, we detected different patterns of heteroscedasticity between shocks to variables through time. For example, the evolution of the volatility of the oil price shock, which presents high volatility along the period analyzed, is shown. We can highlight the significant increase in the uncertainty in 1999 and 2014. In 1999, the increase in volatility can be associated with the adverse economic conditions that characterized the period and the sudden decrease in the oil price. In 2014, the rise in uncertainty in the second half of the year was associated with the sudden decline in oil prices on the international market.

Regarding the dynamics of shocks to oil production, between 1985 and 1993, relatively high volatility is observed, which can be associated with the discoveries of the Cano Limon and Cusiana and Cupiagua oilfields, and with changes in the regulatory framework related to concession contracts.

Between 1995 and 2000, the volatility stabilized due to a sustained increase in production. Since this period, changes in oil production have been gradual.

The variance of government debt shocks shows a moderate positive trend during the analyzed period. In contrast, private consumption shocks were more volatile for the 1985 to 1995 period, stabilizing at relatively low levels. The volatility of the private investment shock has risen steadily since 2009.

Finally, there is evidence of small changes in volatility for real exchange rate shocks. In summary, the volatility of structural shocks to selected variables has registered different patterns, justifying our use of the tvp-var methodology.

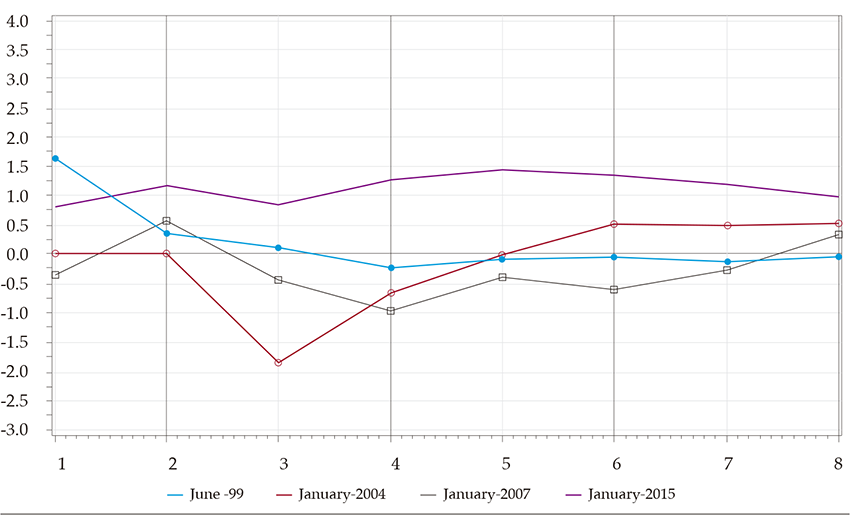

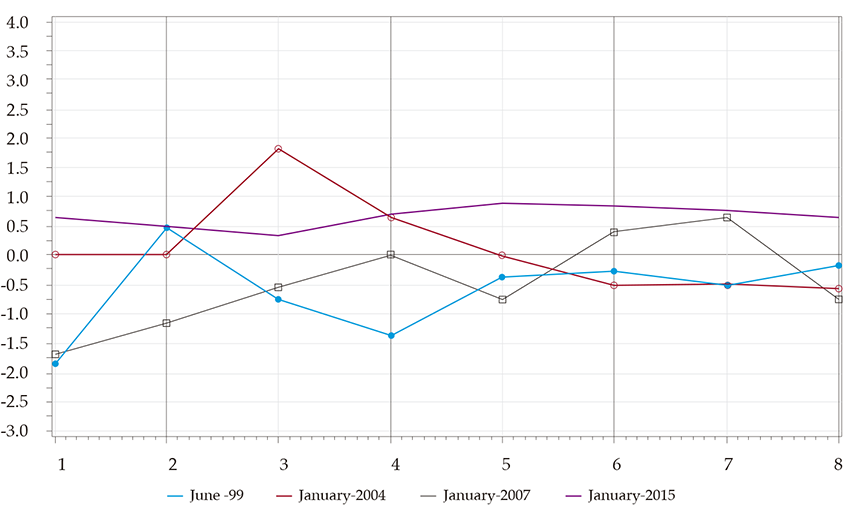

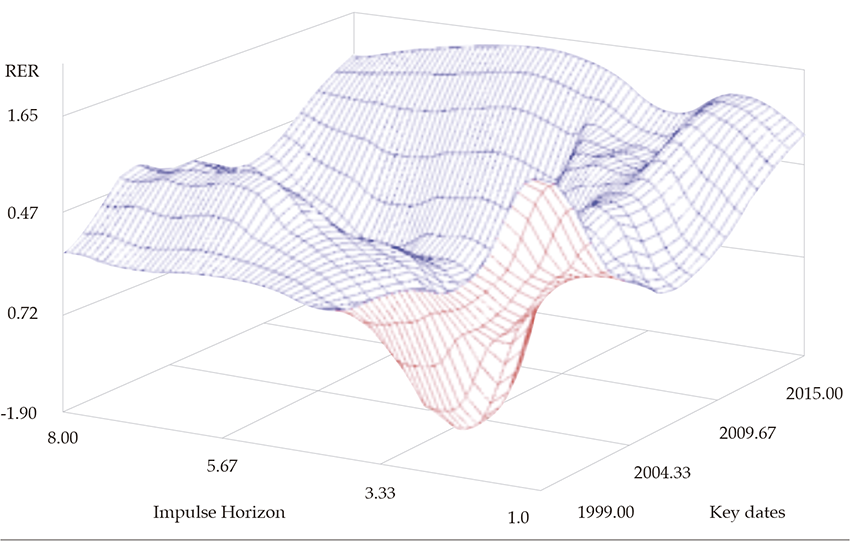

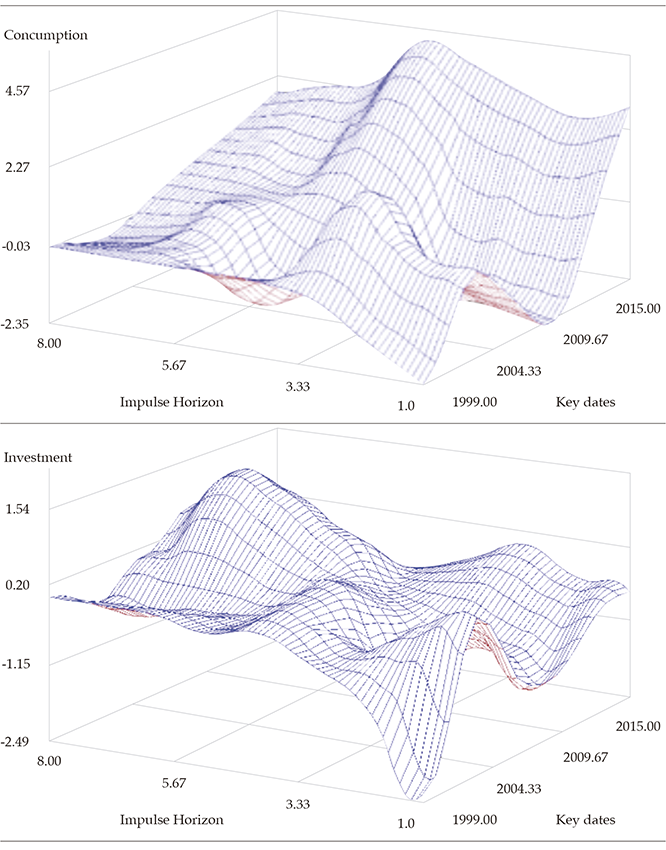

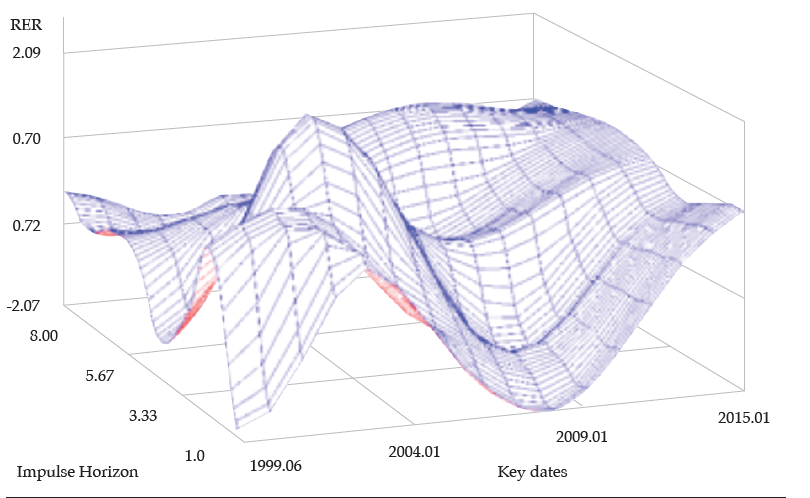

Impulse-response functions are computed for representative dates, selected based on the observed changes in oil price and production variables (figure 3). Specifically, we have selected the following dates: June 1999, January 2004, January 2007, and January 2015.3 The first date corresponds to a period with prices close to 20 us$ and daily production close to 800 kbpd. On the second, the price is growing, and production is falling to less than 600 kbpd. On the third, the price has an upward trend becoming steeper, achieving 70 usd, and production has a switching trend from downward to upward. The fourth date is characterized by a sharp price slide, which started in 2014, and stable production.

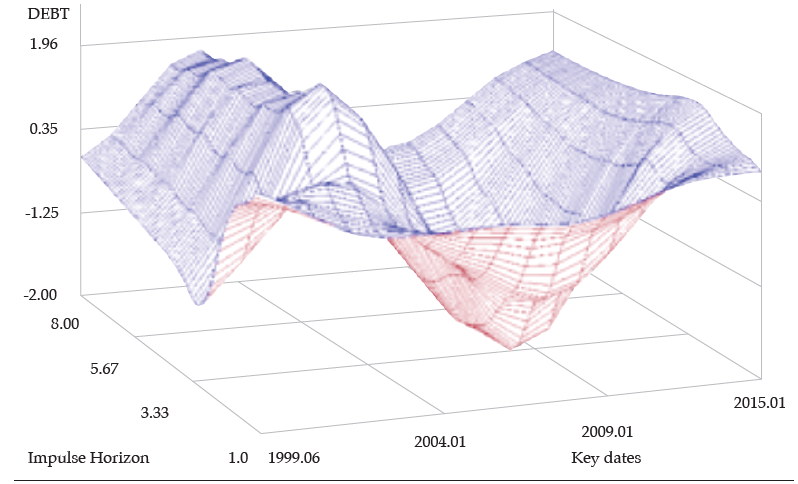

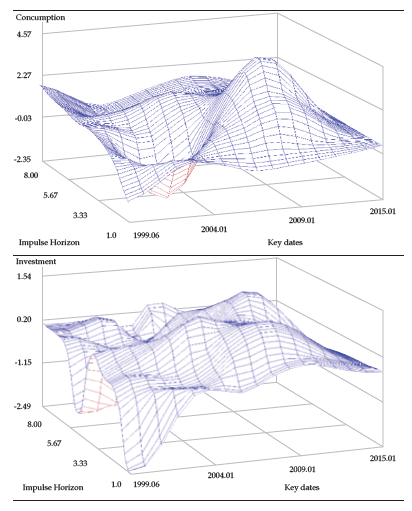

We present the time-varying impulse-response functions, which are calculated at each selected date over the sample period. Thus, the impulse responses are estimated for each iteration of the mcmc simulation with the current draw of the parameters, and the mean of the responses are computed. Figures 4 and 5 display the plot of the responses of the real exchange rate, private consumption, private investment, and public debt to oil-price and production shocks.4 In the cases of positive oil price shocks, the real exchange rate does not present significant variations, except in January 2004, when an upward trend of price and production caused real appreciation. In contrast, the negative oil price shock of January 2015 led to a significant and permanent depreciation of the real exchange rate due to the importance of the oil industry to the Colombian economy. According to the results, a negative price shock equivalent to 10 % leads to a devaluation of the real exchange rate equal to 8.1 % in the next semester. In the case of production shocks, the real exchange rate demonstrates similar behavior, but with less magnitude.

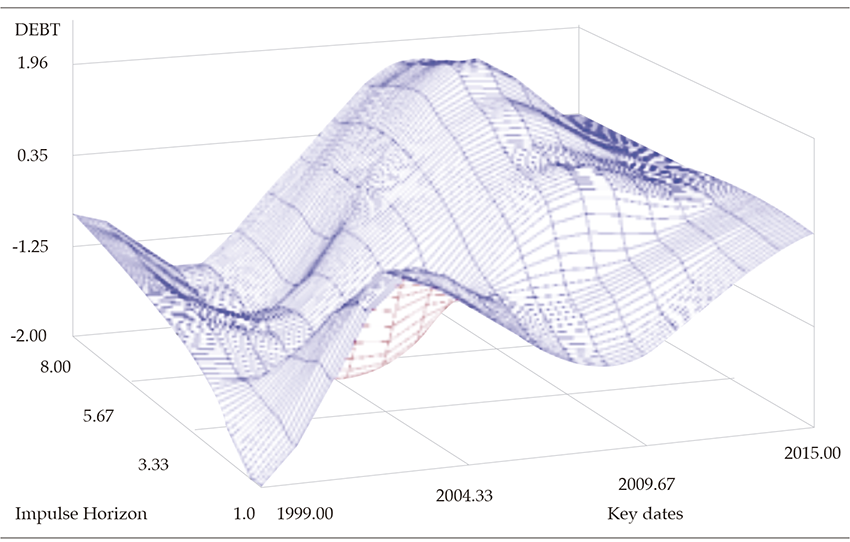

Private consumption adjusts rapidly after positive oil price shocks. The response of consumption to the negative price shock in 2015 is ambiguous, as during the first-trimester consumption drops off, but subsequently, it gradually rises. In the case of production, positive shocks generate a rapid increase in private consumption that stabilizes in the middle term. Likewise, a positive price shock leads to a reduction in public debt, except for in January 2004, when the debt increased, reaching a maximum in the third semester after the shock. We emphasize that a negative oil price shock in the last analyzed period led to an increase in public debt.

The decrease in oil prices observed since mid-2014 has generated a reduction in public revenue and, therefore, has been a detriment to the country’s fiscal posture. This fact has forced the government to increase its debt and adopt austerity measures to adjust public expenditures. In 2014, oil revenues constituted the fifth largest part of the government’s; thus, the fall in oil prices caused a pivotal reduction in fiscal revenues from dividends and taxes. According to our estimations, a negative price shock equivalent to 10 % would generate an approximate increase of 8.9 % in the annualized government debt.5

Concluding and policy implications

In this paper, we set two goals. First, we described the main events in the history of Colombia’s oil industry, highlighting the theoretical aspects of booms and crises. We identified the transmission channels through which oil price and production shocks affect public finances, the external sector, and economic activity. From the historical perspective, the boom of the 1990s had a higher impact on the Colombian economy than the recent oil boom.

The sudden reduction in prices led to an appreciation devaluation of the real exchange rate, an imbalance in current accounts, and a reduction of fiscal revenues. Second, we used a tvp-var econometric analysis to provide quantitative empirical evidence of the impact of oil price or production shocks on macroeconomic and fiscal variables, considering that the relationship among variables changes over time.

Our results indicate that the shock volatility of the analyzed variables has remained unstable during the analyzed period, indicating the relevance of using the tvp-var methodology. The impulse-response functions suggest that the real exchange rate does not respond significantly to positive price shocks, except in the case of January 2004, when there was a real appreciation. Likewise, the negative price shock in January 2015 reflects a considerable and permanent depreciation of the real exchange rate.

Concerning the impulse response functions, a negative price shock equivalent to 10 % generates a devaluation of the real exchange rate equal to 8.1 % the following trimester. Finally, a positive price shock causes a reduction in public debt in all periods, except in January 2004, when the response was positive. The negative shock to oil price observed recently has increased the public debt due to the reduction in fiscal revenues derived from oil. According to the estimations, a reduction of 10 % in the oil price would generate an increase in annual debt equal to 8.9 %. The above findings highlight the importance that in countries highly dependent on oil resources, policies taken to deal with positive or negative oil shocks consider the macroeconomic situation of the country given that the relation between prices and oil production with macroeconomic variables changes dynamically.

References

Baffes, J., Kose, A., Ohnsorge, F., & Stocker, M. (2015). The great plunge in oil prices: Causes, consequenses, and policy responses. Retrieved from http://pubdocs.worldbank.org/en/339801451407117632/PRN01Mar2015OilPrices.pdf

Chow, G. C. & Lin, A-I. (1971). Best linear unbiased interpolation, distribution and extrapolation of time series by related series. Review of Economics and Statistics, 53(4), 372-375. Doi: 10.2307/1928739

Enders, W. (2008) Applied econometric time series. London: John Wiley & Sons.

Geweke, J. (1992) Evaluating the accuracy of sampling-based approaches to calculating posterior moments. In J. M. Bernado et al. (Eds.) Bayesian Statistics 4 (169-193). Oxford: Clarendon Press.

Marcellino, M. & Schumacher, C. (2010) Factor midas for nowcasting and forecasting with ragged-edge data: a model comparison for German gdp. Oxford Bulletin of Economics and Statistics, 72(4), 305-9049. Doi: https://doi.org/10.1111/j.1468-0084.2010.00591.x

Nakajima, J., Kasuya, M., & Watanabe, T. (2011) Bayesian analysis of timevarying parameter vector autoregressive model for the Japanese economy and monetary policy. Journal of the Japanese and International Economies, 25(3), 225-245. Doi: https://doi.org/10.1016/j.jjie.2011.07.004

Owen, A. B. (2017) Statistically efficient thinning of a Markov chain sampler. Retrieved from https://arxiv.org/pdf/1510.07727.pdf

Perry, G. Bustos, S., & Su-Jade, H. (2011) What do non-renewable natural resource rich countries do with their rents. caf Working paper, (6). Retrieved from http://scioteca.caf.com/handle/123456789/221

Perry, G., & Olivera, M. (2012) El petróleo en la economía colombiana. In G. Perry & M. Olivera (Eds.), Petróleo y minería: ¿bendición o maldición? (pp. 173-211). Bogotá: Banco Mundial, Fedesarrollo y Gobierno de España.

Pieschacón, A. (2010). Oil booms and their impact through fiscal policy. srrn Electronic Journal. Doi: 10.2139/ssrn.938197

Primiceri, G. (2005). Time-varying structural vector autoregressions and monetary policy. The Review of Economic Studies, 72(3), 821-852.

Puyana, A. & Thorp, R. (1998). Elementos teóricos para el estudio del impacto sectorial de la bonanza petrolera. In A. Puyana & R. Thorp (Eds.), Colombia: economía política de las expectativas petroleras (1-7). Bogotá: TM Editores – Flacso.

Rosoiu, A. (2015). Monetary policy and time varying parameter vector autoregression model. Procedia Economics and Finance, 32, 496-502. Doi: https://doi.org/10.1016/S2212-5671(15)01423-9

Sachs, J. & Larraín, B. (1994). Bienes transables y no transables. In J. Sachs & B. Larraín (Eds.), Macroeconomía en la Economía Global (pp. 633-678). Buenos Aires: Pearson-Prentice Hall.

Appendix A

(a) Oil price wti and National Production.

(b) Fiscal revenue from oil activity.

(c) Balance current account and real exchange

(d) Share of oil in total exports and terms of trade rate index.

(e) Direct foreign investment in the oil sector.

(f) Share of oil sector on gdp.

Appendix B

Appendix C

*Estimation results for selected parameters in the tpv-var model. Sample autocorrelations (top), full sample paths (middle) and posterior densities (bottom).

Appendix D

Appendix E

Impulse Response Functions Due to Changes in Oil-Prices for Eight Quarters and for Some Key Dates (Cont.)

Notes

* We acknowledge Clark Granger for his excellent research assistance. Opinions expressed here are the responsibility of the authors and do not reflect the opinions of Banco de la República or its Board of Directors.

1 Appendix A presents the evolution of the oil and other macroeconomic variables.

2 Pieschacón (2010) assumes strict exogeneity in the oil price in a sample of countries using a lineal var.

3 The methodology allows us to compute the impulse-response functions for any date of the analyzed period.

4 Given that we compared the time-varying impulse-response functions for key dates, credible intervals are not shown in figures 4 and 5, since they make it difficult to read them. This information is available from authors upon request.

5 Appendix E provides the impulse response functions for the macroeconomic variables due to changes in prices and oil production, for eight quarters and for the selected key dates. For this exercise, we follow the strategy by Rosoiu (2015), which allows us to appreciate the entire trajectory of the impulse response functions.

Author notes

‡ Corresponding author. E-mail: lmelobec@banrep.gov.co