Monetary Policy and Accumulation of Reserves in an Emerging Economy: A DSGE Model for the Colombian Case

Política monetaria y acumulación de reservas en una economía emergente: un modelo DSGE para el caso colombiano

Política monetária e acumulação de reservas em uma economia emergente: um modelo DSGE para o caso colombiano

Monetary Policy and Accumulation of Reserves in an Emerging Economy: A DSGE Model for the Colombian Case

Revista de Economía del Rosario, vol. 21, no. 2, 2018

Universidad del Rosario

Received: October 27, 2017

Accepted: May 02, 2018

Additional information

To quote this article: Botero G., J., Hurtado Rendón, A.,

Franco G., H., & García Guzmán, J. (2018). Monetary policy and accumulation

of reserves in an emerging economy: A DSGE model

for the Colombian Case. Revista de Economía del Rosario, 21(2), 309-339. DOI: https://doi.org/10.12804/revistas.urosario.edu.co/economia/a.6802

Abstract:

This article presents a dynamic stochastic general equilibrium model in which we explicitly include the demand for money, the investment decisions, the role of financial intermediaries and the central bank balance sheet. The model allows the evaluation of the impact of various exogenous shocks on the economic activity and the price levels. Similarly, it allows to assess different forms of central bank intervention in the economy, either through the interest rate, or through the accumulation of international reserves. Special attention is dedicated to the basic parameters of the utility function of households (risk aversion, elasticity of labor supply and demand for money), to the proper formulation of the balance sheets of economic agents, and to the relationship between the central bank balance sheet and the money supply.

JEL Classification: E17, E62, E44, E37

Keywords: DSGE, monetary policy, fiscal policy, economic theory.

Resumen:

Este artículo presenta un modelo de Equilibrio General Dinámico Estocástico (DSGE) en el que se incluye explícitamente la demanda de dinero, las decisiones de inversión, el papel de los intermediarios financieros y el balance del Banco Central. El modelo permite la evaluación del impacto de diversos shocks exógenos sobre la actividad económica y los niveles de precios. También, permite evaluar diferentes formas de intervención del banco central en la economía, ya sea a través de la tasa de interés o mediante la acumulación de reservas internacionales. Se presta especial atención a los parámetros básicos de la función de utilidad de los hogares (aversión al riesgo, elasticidad de oferta laboral y demanda de dinero), a la formulación adecuada de los balances de los agentes económicos, y a la relación entre el balance del banco central y la oferta de dinero.

Clasificación JEL: E17, E62, E44, E37

Palabras clave: DSGE, política monetaria, política fiscal, teoría económica.

Resumo:

Este artigo apresenta um modelo de Equilíbrio General Dinâmio Estocástico (DSGE) no que se incluiu explicitamente a demanda de dinheiro, as decisões d investimento, o papel dos intermediários financeiros e o balanço do Banco Central. O modelo permite a avaliação do impacto de diversos choques exógenos sobre a atividade econômica e os níveis de preços. Também, permite avaliar diferentes formas de intervenção do banco central na economia, seja através da taxa de juros seja mediante a acumulação de reservas internacionais. Prestase especial atenção aos parâmetros básicos da função de utilidade dos lares (aversão ao risco, elasticidade de oferta laboral e demanda de dinheiro), à formulação adequada dos balanços dos agentes econômicos, e à relação entre o balanço do banco central e o fornecimento de dinheiro.

Classificação JEL: E17, E62, E44, E37

Palavras-chave: DSGE, política monetária, política fiscal, teoria econômica.

Introduction

According to Blanchard et al (2012), “before the economic crisis began in 2008, mainstream economists and policymakers converged on a beautiful construction for monetary policy. To caricature just a bit: we had convinced ourselves that there was one target, inflation, and one instrument, the policy rate. And that was basically enough to get things done”. But the crisis has shown the fallacy of this construction: it is not evident that stable inflation is enough to get a small and constant output gap. Excessive leverage of households, firms and government could produce bubbles in asset prices, and consequently could deeply destabilize the economy. On the other hand, excessive leverage by the financial sector could produce an unusual increase in risk levels (frequently originated from asymmetric information conditions, associated with the “moral hazard” concept) that can lead to a sudden stop in the economic activity. Consequently, both asset prices and leverage of economic agents became essential elements, even though we are far from knowing in detail how they influence the economy and how some warnings signals could be considered in the analysis. As a result, economist have a double requirement: first, to explicitly consider the asset prices gap in monetary policy and second, to include agents leverage in the monitoring of economic evolution.

These changes in defining monetary policy go along with the fact that, in developed countries, intervention interest rates have reached their effective lower bound. This has forced these countries to use non-conventional monetary policies implying new problems of consistency and communication, and thus making the monetary policy more complex, as it is pointed out by some authors such as English et al. (2015).

Thus, not only decisions on short-term interest rates can have an influence on asset prices 1 and agents leverage. There are also other monetary policy instruments that have an influence on them: decisions on liquidity provisions, monetary aggregate management, other forms of credit expansion, formation of expectation on future interest rate through forward guidance and macroprudential policies. Additionally, for emerging economies, it is necessary to incorporate foreign exchange interventions in the monetary policy management. Those interventions could affect the use of conventional instruments, or constitute an alternative goal of the monetary policy, as shown by Ostry (2012). Many central banks only recognize the marginal presence of the exchange rate in their monetary management through its inflation impact. But the exchange rate has an essential role, not only for its impact on economy´s competitiveness, but also for its predominant role in foreign exchange holdings in the balance sheet of central banks.

In this context, Vargas et al. (2013) analyze how the Colombian central bank has been intervening in the foreign exchange market and the immediate aims of this intervention. The final objectives of intervention in Colombia have been restricted to three elements, namely: maintenance of a proper level of international reserves, correction of the exchange rate misalignment from its long-term equilibrium level, and, sometimes, the control of its volatility through option auctions where it is possible to buy and sell foreign currency according to its representative market rate in relation with its moving average value during the last twenty days. The bank’s policy has been focused on sterilized exchange interventions in order to maintain the short-term interest rate in the direction of the policy interest rate.

In conclusion, the link between inflation stability and product is not clear, and new objectives must be considered: asset prices, agents leverage, financial stability and exchange rate. According to this, new instruments are also needed: massive interventions in credit markets, macro-prudential policies to mitigate systemic risks, forward guidance to influence the future interest rate, interventions in the foreign exchange market and control over capital flows. Extending the scheme proposed by Blanchard et al. (2012), it could be affirmed that if the simple scheme in Figure 1 could be enough to represent the monetary policy before the great recession, now a more complete scheme, such as the one shown in Figure 2, would be necessary.

This complex scheme has a mixed set of macro-prudential policies and balance sheet measures directly affecting financial stability, but also affecting inflation and product. The interest rate conventional policy now completed with forward guidance affects the traditional prices and the output gap, and similarly impacts the financial stability and the exchange rate. The foreign exchange insterventions influence the exchange rate, prices and product. In this scheme, not only the central bank’s balance sheet recovers its main role in implementing the monetary policy, but also the monetary authority has a complete tool box at its disposition to influence gaps in inflation, output and the system risk that affect the economic activity.

The economic world crisis between 2008 and 2013 has had and will continue to have colossal consequences over economic thinking, the beliefs in free markets and the role of monetary policy. 2 There has been (and there will continue to be) a rich discussion about these topics, but only time will give us the right perception about what happened (Blinder, 2013). However, some conclusions seem to be obvious, at least for those who work in modeling related topics. First, the microeconomic attention given to the financial sector has been deficient and inadequate; second, although some important advances have been made in financial frictions analysis, their role remain marginal in economic modeling; and third, attention provided to asset price bubbles in modeling has been insufficient.

In the same way, there are also some immediate lessons related to monetary policy: 3 the consensus reached about “inflation targeting” scheme, despite the fact that it achieved a fundamental role in the first decade of 21st century, is inadequate today. Excessive emphasis on the short-term interest rate as a monetary policy essential instrument has been seriously questioned after continuous events of “quantitative easing”. The exclusive attention given to inflation and the output gap seems having forgotten essential topics, which have been decisive during the last years: the relation between financial instability and price bubbles, and the role of “macro-prudential” policies in the economic system stabilization. 4

Given all those considerations, our model aims at advancing towards two aspects: incorporating the financial sector into modeling as an optimizer agent with enormous relevance in economy and making the “balance sheet” of the central bank explicit. We pretend to allow a broader monetary policy vision and to clarify the link between this policy and the foreign exchange policy, which in an emergent and small economy such as Colombia depends essentially on the central bank.

To precisely describe the role of the financial sector in the economy, it is crucial to explain the role of different agents in the financial system such as borrowers or lenders. Specifically, this model supposes that “households” (main private agents in the economic system) play as resource suppliers in the financial system and a new type of agents (“investment companies”) play as demander of these resources. Investment companies are neutral risk agents, who are looking for new investment opportunities in productive fixed assets and maximizing their expected benefits. These benefits are defined as the difference between investment revenues (obtained by leasing assets for firms that use them for productive processes), and the investment cost, which includes not only the asset value, but also the convex adjust costs that reflect the growing difficulty to adjust productive asset levels to their optimum point. 5

For the central bank, the model makes its balance sheet clear, including money supply, credit operations with the financial sector and a fundamental asset for emerging countries such as Colombia: international reserves.

The reference to the balance sheet of the central bank, and the consideration of the optimum decision of financial intermediaries (and their budget constraints), allow us to analyze in detail the traditional monetary aggregates, M1 and M3, which are included in the system, allowing the analysis of expansive policies implemented through the variation of money supply. This is important, firstly, because the prevalence of nominal interest rates close to zero in almost all developed countries during 2009-2015 limits the use of conventional monetary policies. Secondly, because the foreign exchange policy used in emerging countries, mainly through the balance sheet of the central bank, due to the great participation of reserves in their total asset levels.

We identified three different research strands in the monetary policy recent development: the first one introduces financial frictions related to credit constraints faced by non-financial agents in the dsge standard model; the second one analyzes these frictions in financial intermediaries, particularly the banks; and, the third one, analyzes the relation between monetary and macroprudential policies.

Concerning the first research strand mentioned above, it is essential to introduce the “financial accelerator” concept. The main studies regarding this subject are Bernanke et al. (1999), Smets and Wouters (2003, 2007), Christensen and Dib (2005), and Christiano et al. (2010). They found that the existence of agency problems in financial agreements and liquidity constraints faced by the banks are the main determinants of economic fluctuations. In addition, the presence of asymmetric information between entrepreneurs and lenders generates financial friction that makes capital demand to depend on their financial situation. On the other hand, Kiyotaki and Gertler (2010) developed a financial intermediation model under the framework of business cycles without frictions. Their goals are, first, to illustrate the way financial intermediation interruptions could induce a crisis affecting real activity, and second, to evidence the way interventions in credit markets done by economic authorities could mitigate those crises.

The second research strand includes financial markets and frictions to banking market. Dellas et al. (2010) consider positive implications and rules associated to different financial shocks, proving that those financial frictions significantly affect monetary and fiscal policies. Gerali et al. (2010) present a dsge model in order to study the role played by credit supply factors in the economic cycle, and Meh and Moran (2010) affirm that the main feature is the agency problem constraint between lenders and banks through capital banking.

Finally, there is a series of papers related to the third research strand mentioned above that aim to respond to concerns specific to monetary policy and financial stability, by distinguishing between monetary and macroprudential policies (Adrian & Liang, 2016; Svensson, 2018). They conclude that monetary policy and macroprudential policy are different and have different objectives and instruments, but that there is some interaction between them. The monetary policy has strong and systemic effects on price stability and on real stability, but its impact is small and indirect on the financial stability. In contrast, macroprudential policy has a strong and systemic impact on financial stability, but a small and indirect one on inflation. They suggest separating the implementation of such policies in a way that each of them focuses on achieving their objectives. In addition, they emphasize that monetary policy can influence vulnerabilities. One possible novelty of the work of Adrian and Liang (2016) is the incorporation of a new monetary policy transmission channel (in addition to the traditional price of assets expectations channel); the risk-taking channel that considers the change in prices in asset markets, the banking sector and non-financial sector loans.

The rest of this article is organized as follows: in the next section we present the model, detailing equations in the appendix; then, we report two simulation exercises illustrating how it works; and in the final section we deal with the conclusions.

1. The Model

The model describes an open economy in steady state equilibrium, but that is subject to exogenous shocks that can temporarily deviate it from that equilibrium. It incorporates five types of internal optimizing agents (households, production companies, trading companies, investment companies and financial intermediaries); two public agents (government and the central bank); and two external agents (rest of the world and the international financial system). The steady state equilibrium assumes that income and expenses flows are balanced among agents, and also that financial assets of the economy are in equilibrium, that is, financial assets and liabilities of the agents are adjusted through financial intermediaries and the international reserves are incorporated into the central bank’s balance sheet.

The economy operates under monopolistic competition conditions, and is subject to price inflexibilities, which are modeled by Calvo’s prices. The domestic economy sells two types of goods to the rest of the world: commodities (oil), in markets where it is a price taker; and other goods, which are imperfect substitutes for goods produced in countries with which it competes in international markets. The high dependence on commodities makes it vulnerable to exogenous shocks generated by fluctuations in their prices. These shocks affect both the current account of balance of payments and fiscal accounts since a significant proportion of oil revenues are appropriated by the government.

Trading companies buy goods and services from domestic production companies and from the rest of the world. Goods and services produced internally and abroad are imperfect substitutes. With these purchases, trading companies meet consumption demands, investment and public spending.

Domestic agents receive remittances, foreign direct investment and other capital flows from the international financial sector, including those destined to finance the central government’s deficit.

Households maximize their inter-temporal utility function, defining how much labor is to be offered, which is their consumption level, and how much real money balances are to demand. In doing so, they define how much savings to place in the financial system. Investment companies demand funds from the financial system, solving their problem of inter-temporal optimization of capital accumulation, subject to quadratic adjustment costs. The capital they accumulate is lent to productive companies, which also use the capital accumulated by investors from abroad and demand work, to solve their problem of minimizing costs.

Financial intermediaries manage savings and credit demands of agents, maximizing their profit, given convex transaction costs and the risk of portfolio losses due to information asymmetry. They can turn to central bank credit and must comply with macro-prudential restrictions imposed upon them.

The government receives income from oil exports, 6 determines the direct and indirect tax rates and defines an exogenous spending plan. Its fiscal result is endogenously determined and must be consistent in the long term with the level of sustainable indebtedness, which is assumed to correspond to the debt level observed in the steady state equilibrium. Any mismatch taking place because of exogenous shocks the economy experiences must be corrected in the long term through fiscal policy, either by increasing taxes, or through future contraction of public spending.

Finally, the central bank manages assets and non-monetary liabilities of its balance sheet to determine money supply. It also fixes the interest rate at which it lends funds to the financial sector. Thus, it determines the inflation level. It also affects the exchange rate, which is adjusted to equilibrate the current account of the balance of payments with capital movements and variation in reserves.

The model considers three types of economic policies: fiscal policy, which determines taxes and expenditures by adjusting to a level of sustainable indebtedness; monetary policy, which operates through the Taylor rule; and the exchange policy, which determines the accumulation or de-accumulation of international reserves. The central bank may also apply macro-prudential policies, affecting reserve levels that financial intermediaries must maintain in proportion to their deposits. The equations of the model are presented in the Appendix.

2. Calibration and Simulation

The model is calibrated with information of 2010 which is a representative year of the behavior of the Colombian economy and we assume it replicates Colombia´s steady state. During this year, the gdp grew at a yearly rate of 4 %, and inflation was 3.17 %. Additionally, the central bank intervention rate started the year at 3.5 % and finished it at 3 %. Data used are annualized and come primarily from the National Accounts, Balance Payments and the series of monetary aggregates of the Banco de la Republica (Colombia´s central bank). The elasticities of functions used in the model are summarized in Table 1.

Import/exports substitution elasticities reflect typical values of these functions in general equilibrium models. It is assumed that 50 % of firms cannot change prices in each period. The elasticity of default risk and the management costs to the volume of credit generated by financial intermediaries equals 1.2. Deposits and central bank credit substitution elasticity is presumed equal to 2. Risk aversion parameter equals 0.57. Labor supply elasticity is assumed at 0.4, according to Reichling and Whalen (2012). The money demand elasticity to the interest rate is 0.4, which is considered as a common value in the literature (Walsh, 2010). The profit margin of firms in monopolistic competition equals 5.3 %).

Following the oil price reduction in the second semester of 2014, the Latin American economies, and particularly the Colombian, faced strong repercussions on their revenues, altering their short and long-term fiscal incomes. On the other hand, continuous natural disruptions that have challenged the Colombian productive structure, and the dynamism of international trade that has intensified the reallocation of capital and labor productive factors make it necessary to incorporate short-term effects of productivity changes into the model.

Two possible exogenous shocks have been evaluated: a temporary drop in productivity, and a drop of oil prices. The first shock seeks to replicate the situation arising in the Colombian economy when there are extreme climatic conditions (such as the El Nino phenomenon) which affect the agricultural sectors productivity and generate inflationary pressures. The second shock simulates the effects of the fall in oil prices which, since mid-2014, has affected both public finances and the growth of the economic activity in the country.

In each simulation, four economic policy scenarios are evaluated: the basic scenario, in which no intervention is given by fiscal or monetary authorities; a second scenario in which an anti-cyclical fiscal policy is applied by increasing public expenditure in response to negative shocks; a third scenario that uses the Taylor rule formed by monetary authorities; and, finally, a fourth analysis that applies certain exchange rate measures in response to shocks. The results of the negative productivity shock are presented in the following graphic:

The productivity shock affects the output level and the remuneration of productive factors, labor and capital. The wage reduction negatively affects household incomes, reduces labor supply and decreases the consumption demand. Furthermore, the demand for money also drops generating an inflation increase as long as the money supply remains unchanged. The fall in remuneration to capital negatively affects investment and the corresponding demand of funds which, in turn, generates downward pressures on the interest rate. Likewise, output drop generates a shift of the import demand function, thus generating a currency revaluation, which negatively affects exports.

Evaluating the policy options, only the anti-cyclical policy, which moderates the gdp drop, is relevant, at the cost of additional future contractions in the pace of economic activity. The Taylor rule, confronted with a negative output gap and a positive inflation gap, can only exaggerate either gap, so it doesn’t seem to be a desirable option under these circumstances. The ex change rate policy does not play a relevant role either as the shock affecting economy is not generated in the foreign exchange market. Figure 4 analyzes transmission mechanisms the model puts into play as a response to the productivity shock.

The oil price shock has negative effects on output, consumption and inflation, slightly increasing the latter. It also generates currency depreciation, which has a positive impact on non-oil exports and a negative one on imports. Drop in fiscal revenues obliges the government to increase public debt and forces it to implement a tax reform that will, in the future, allow it to pay for the increased indebtedness.

The impulse-response functions of the negative shock in oil prices are presented in the Figure 5:

The anti-cyclical policy moderates the impact on the output but generates the usual long-term costs. The Taylor rule faces its own dilemma of a situation with a negative output gap and a positive inflation gap. Overall, whatever is done to relieve one of the gaps, affects the other one, which leaves an uncertain balance of intervention.

The exchange rate policy, on the other hand, can generate positive effects through decumulation of reserves. It may even reverse the output drop and the inflation increase. Of course, decumulation of reserves involves vulnerability risks that are difficult to analyze in models such as ours as we assume rational expectations. Nevertheless, the suggestion is clear: in order to face non-permanent shocks in foreign exchange markets, the first option is the exchange rate policy, through accumulation or decumulation of reserves.

Conclusions

The analysis presented suggests that, in the face of each type of shocks, there are optimal economic policy responses that fit their peculiarities. In the case of negative productivity shocks, it seems doubtful that a conventional monetary policy would be the right answer because in those circumstances the policy is subject to the dilemma of tackling inflation by generating an additional negative output gap or mitigating the latter gap by triggering an additional price increase. The usual response has been the first one, even when a negative productivity shock is considered to be transitory. This is due to the belief that the formation of expectations can make the effects of the shock on inflation permanent. To adequately assess the relevance of this statement, one would have to adequately establish the formation of expectations in the model. But anyhow, perhaps it is important to consider that the negative impact intervention has on the activity level may also spread over time due to the expectations of entrepreneurs and consumers, who may negatively react to the additional deceleration produced through the intervention.

For the oil price shock, the optimal policy response would be the exchange rate policy, as long as it is assumed that the price change is not a permanent shock. In the case that the oil price shock is permanent, other measures that have to do with transit from one stationary state to another would undoubtedly be required.

In any case, the analysis reveals the need for evaluating economic policy alternatives within the general equilibrium models’ framework, in which the behavior of all agents (including financial institutions) is properly modeled and consideration is given to all alternatives available to the economic authorities to respond to adverse circumstances that may affect the economy. It will be necessary to deepen into a methodology that allows comparing shortand long-term effects of the measures, and adequately weighting different factors that influence its operation.

References

Adrian, Tobias, & Liang Nellie (2016). Monetary Policy, Financial Conditions, and Financial Stability. Federal Reserve Bank of New York Staff Reports, March 2016.

Ahmed, W., Haider, A., & Iqbal, J., et al. (2012). Estimation of Discount Factor (beta) and coefficient of relative risk aversion (gamma) in selected countries. MRPA Paper, (39736).

Bernanke, B. S., Gertler, M., & Gilchrist, S. (1999). Chapter 21The financial accelerator in a quantitative business cycle framework, Handbook of Macroeconomics, Elsevier Volume 1, Part C, Pages: 1341-1393.

Blanchard, O. J., Romer, D., Spence, M., & Stiglitz, J. E. (2012). In the wake of the crisis: Leading economists reassess economic policy. Cambridge: MIT Press.

Blinder, A. S. (2013). After the music stopped: The financial crisis, the response, and the work ahead. New York: Penguin Press.

Botero, J. A., & Rendón, N. (2015). Política monetaria convencional y no convencional: un modelo de equilibrio general dinámico estocástico para Colombia. Ensayos sobre Política Económica, 33(76):4-17.

Calvo, G. A. (1983). Staggered prices in a utility-maximizing framework. Journal of monetary Economics, 12(3):383-398.

Chari, V. V., Christiano, L. J., & Eichenbaum, M. (1995). Inside money, outside money and short-term interest rates. Technical report, National Bureau of Economic Research. Working Paper 5269.

Christensen, I., Dib, A., et al. (2006). Monetary policy in an estimated DSGE model with a financial accelerator. Staff Working Papers 06-9, Bank of Canada.

Christiano, L. J., Eichenbaum, M., & Evans, C.L. (2005). Nominal rigidities and the dynamic effects of a shock to monetary policy. Journal of political Economy, 113(1):1-45.

Christiano, L.J., Motto, R., & Rostagno, M. (2010). Financial factors in economic fluctuations. Working Paper Series 1192, European Central Bank.

Dellas, H., Diba, B., & Loisel, O. (2010). Financial shocks and optimal policy. Working papers 277, Banque de France.

Eichengreen, B., Prasad, E., & Rajan, R. (2011). Rethinking central banking: Its time for an alternative framework. Rethinking Central Banking. Brookings Institution: Washington.

English, W. B., López-Salido, J.D., & Tetlow, R.J. (2015). The federal reserves’ framework for monetary policy: Recent changes and new questions. IMF Economic Review, 63(1): 22-70.

Gerali, A., Neri, S., Sessa, L., & Signoretti, F.M. (2010). Credit and banking in a DSGE model of the euro area. Journal of Money, Credit and Banking, 42(s1): 107-141.

Gertler, M., & Kiyotaki, N., et al. (2010). Financial intermediation and credit policy in business cycle analysis. Handbook of monetary economics, 3(3):547-599.

Hayashi, F. (1982). Tobin’s marginal q and average q: A neoclassical interpretation. Econometrica: Journal of the Econometric Society, 213-224.

Kydland, F.E., & Prescott, E.C. (1982). Time to build and aggregate fluctuations. Econometrica: Journal of the Econometric Society, 1345-1370.

Meh, C.A., & Moran, K. (2010). The role of bank capital in the propagation of shocks. Journal of Economic Dynamics and Control, 34(3):555–576.

Ostry, J.D. (2012). Managing capital flows: What tools to use? Asian Development Review, 29(1):82.

Reichling, F., & Whalen, C. (2012). Review of estimates of the Frisch elasticity of labor supply. Washington, DC: Congressional Budget Office.

Smets, F., & Wouters, R. (2003). An estimated dynamic stochastic general equilibrium model of the euro area. Journal of the European economic association, 1(5):1123–1175.

Smets, F. & Wouters, R. (2007). Shocks and frictions in us business cycles: A bayesian dsge approach. National Bank of Belgium Working Paper, (109).

Svensson, Lars E. O. (2018). Monetary Policy and Macroprudencial Policy: Different and separate? Stockholm School of Economics, march 2018.

Taylor, J.B. (1993). Discretion versus policy rules in practice. In Carnegie- Rochester conference series on public policy, volume39, pages 195–214. Elsevier.

Vargas, H., González, A., & Rodríguez, D. (2013). Foreign exchange intervention in Colombia. BIS Paper, (73h).

Walsh, C.E. (2010). Monetary theory and policy. Cambridge: mit Press.

Wapshott, N. (2013). Keynes vs. Hayek: el choque que definió la economía moderna. Barcelona: Ediciones Deusto.

Appendix: Model Equations

The model describes an emerging open economy, in steady state equilibrium, that incorporates five types of optimizing agents (households, investment companies, financial intermediaries, production companies and trading companies); two public agents (government and central bank); and two external agents (rest of the world and international banking system). The steady state equilibrium incorporates the balance of income and expenditure flows, but also the balance of basic assets of the economy. The behavior of the agents is described below. Only that equation that are included in the model are numerated.

1. Household

We assume a continuum of households indexed within the interval [0,1]. Their utility depends on consumption, leisure, and real monetary balance holdings, and their problem is:

Subject to:

(E1)

(E1)Where c,n,dm are, respectively, consumption, labor and holding of real balances per unit of effective labor; γc is the relative risk aversion parameter in the consumption; 7 1/γn is the elasticity of intertemporal substitution of leisure; 8 1⁄γm is the elasticity of intertemporal substitution of real balances, 9 β is discount factor; ψn , ψm are weighting factors of utility function; bf ,ga ,f,div ,gb are financial savings, profits of firms, remittances, dividends from investment companies and banking profits, respectively, in real terms and per unit of effective labor; 10 τH is direct tax rate; IR is gross nominal interest rate earned by household for its financial saving, w=W⁄P,er=ER/ P are nominal salary, nominal exchange rate, deflated by price of the consumption, πt +1 = Pt +1 /Pt is inflation and Ɵ is gross rate of population growth:

The relationship between consumption and leisure, the demand for real monetary holdings and the Euler condition are derived from the first order conditions:

(E2)

(E2)

(E3)

(E3)

(E4)

(E4)2. Investment Companies

To model investment decisions, we adopt the scheme presented in Botero and Rendon (2015), where investors maximize expected net incomes, given quadratic adjustment costs during investment process.

Subject to Kt = Kt –1 δ+It

Where R,γ,P,δ are, respectively, capital rent, the constant of adjustment cost, price of capital goods and gross depreciation rate, and IRI is gross active interest rate.

After formulating the dynamic optimization problem, we obtain:

(E5)

(E5)Where:

(E6)

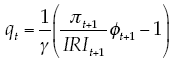

(E6)In the optimal case:

(E7)

(E7)Demand for loanable funds is:

(E8)

(E8)And capital accumulation is:

(E9)

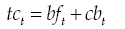

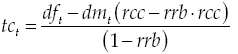

(E9)3. Financial Intermediaries

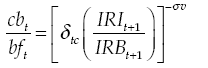

Financial intermediaries receive deposits in current account from households in a fixed proportion (rc) from their money demand dmt , and financial deposits (bft ). They, also, lend money to investment companies (dft ), keep central bank reserves (rft ) and access to credit from the central bank to adjust financial differences (cft ). The relevant nominal rates for deposits, loans and credits are, respectively, IRt ,IRIt ,IRBt .

Lending involves risks of default and management costs, which are reflected in the function Xt = X(dft ), where X',X'' ≥ 0. Financial intermediaries are subject to an institutional constraint, which forces them to keep reserve deposits in the central bank, in a proportion of deposits received: rbt = bt = rrb∙(rcc∙dmt + bft ).

Financial intermediaries have three sources of resources to fund their loans: current accounts, financial deposits and credit from the central bank. The last two sources imply costs, and they are not perfect substitutes. The optimal proportion between them is determined as the solution of the cost minimization problem, through the relation that microeconomist call “expansion path”:

(E10)

(E10)The aggregate cost of resource is:

(E11)

(E11)By definition:

(E12)

(E12)Financial intermediaries seek to maximize their gross rent (final balance of loans minus deposits, including returns and financial costs, adjusted by losses and management costs):

Subject to:

(E13)

(E13)

(E14)

(E14)To replace in objective function, we solve the system formed by restrictions, in terms of df , dm and parameters:

Replacing and deriving

(E15)

(E15)Where function of default risks and management costs is:

Net rents generated are distributed to households:

(E16)

(E16)4. Firms Behavior

There is a continuum of firms (indexed between 0 and 1) in monopolistic competition, which minimize costs, given the demand derived in monopolistic competition. Substitution elasticity between goods of different firms is Ɛ.

Production incorporates three productive factors: national capital, external capital and labor. The accumulation of national capital was described in equation (E9). The accumulation of external capital results from the direct foreign investment:

(E17)

(E17)Relevant equations of cost minimization are:

(E18)

(E18)

(E19)

(E19)

(E20)

(E20)The production function is:

(E21)

(E21)Where yt py are, respectively, output and relative price of production (with respect to the system numeraire); and marginal cost (or unit cost, given constant returns to scale) is defined as:

If there were perfect flexibility of prices, the relationship between price and marginal cost would be:

Where:

Nevertheless: it is possible that, for institutional reasons, producers cannot adjust prices permanently. Such rigidity is modeled with the scheme proposed by Calvo. Probability of not being able to adjust prices in a certain period is ρ. In this case, a representative firm will solve the following maximization problem:

S.t.:

The problem solution is:

(E22)

(E22)Where:

(E23)

(E23)

(E24)

(E24)Aggregate effective price is given by:

(E25)

(E25)And the profit of firm is:

(E26)

(E26)5. Imports Demand

Internal traders minimize:

Subject to:

(E27)

(E27)The corresponding microeconomic expansion path is:

(E28)

(E28)Where:

(E29)

(E29)And total purchases are:

(E30)

(E30)6. Exports Demand

Traders of the rest of the world minimize:

(A7)

(A7)Subject to:

(E31)

(E31)Expansion path is:

(E32)

(E32)7. Exports supply

Entrepreneurs maximize their incomes, given their production possibility frontier: 11

Subject to:

(E33)

(E33)With σd < 0, from cet function.

The expansion path is:

(E34)

(E34)Where:

(E35)

(E35)Total sales of firms are:

(E36)

(E36)8. Government Budget Constraint

Government collects rents from direct taxes, indirect taxes and tariffs. It uses these rents to implement its public spending plan, and goes to external credit market to finance its deficit.

(E37)

(E37)However, indebtedness costs include a risk premium that depends on the indebtedness level of the country:

(E38)

(E38)

(E39)

(E39)9. External Closure

The external balance is:

(E40)

(E40)10. Monetary Supply

Changes in monetary supply evolve according to the variation of international reserves, changes in other assets, banking reserves and credits to financial intermediaries:

(E41)

(E41)11. Closure of Model

We assume the government has an indebtedness target, which is reached adjusting the tax collection to households. When an exogenous shock occurs, the tax rate is adjusted to achieve the expected level of indebtedness:

(E42)

(E42)Where parameter τkH represents speed adjustment.

Notes

1 Including foreign currency.

2 The “Great Depression” of the 30s played an important role in the construction of economic thought: the origin of macroeconomics and Keynesianism were a result of it. Wapshott (2013) makes an interesting review of this line of economic thought and its disputes with the currents of classic thought.

3 A good referent is the report of the Committee on International Economic Policy and Reform: “Re-thinking Central Banking”. Eichengreen et al. (2011).

4 An early study in this aspect was carried out by Blanchard et al. (2012).

5 A classical reference is Hayashi (1982). The investment theory was a late development of neoclassical thinking. Under perfect competition, with constant returns to scale and flexible prices, the problem of optimal investment is indeterminate. Traditional models solve this problem by assigning the decision to households. This implies that the income from investments has a decreasing impact on the household utility function. But this is: i) inaccurate, because productive investment is made in a corporate environment, with the exception of the housing investment; and ii) inconvenient, because it has obscured the role of financial intermediation in the system and it has discouraged microeconomic analysis of financial intermediaries. The classic article by Kydland and Prescott (1982) studies an alternative aspect of adjustment costs: required time to finish the investment process.

6 The state take is defined as a constant share of the government in the oil rents. The difference is appropriated by investment companies.

7 Technically, it is the known Arrow-Pratt measure of relative risk aversion: RRA = γc > 0. It is also the inverse of substitution elasticity. If γc = 1, this function converges to logarithmic case.

8 The parameter is related to the so-called Frisch elasticity: F = 1⁄γn

9 It is the inverse of elasticity for real balances demand to the interest rate.

10 Both dividends of real sector and profits from banking sector are exempt from tax.

11 The production possibility frontier is modeled as a function of constant elasticity of transformation (CET), where substitution elasticity is negative.