Universidad & Empresa

ISSN:0124-4639 | eISSN:2145-4558

ISSN:0124-4639 | eISSN:2145-4558

Examining the Spillover Effect between the KSE100 and the S&P500 Indexes*

Examinando el efecto de derrame entre los índices KSE100 y S&P500

Examinando o efeito de derramamento entre o índice KSE100 e o S&P500

Mudassar Hasan, Muhammad Ishfaq Ahmad, Muhammad Abubakr Naeem, Muhammad Akram Naseem, Ramiz-ur Rehman

Examining the Spillover Effect between the KSE100 and the S&P500 Indexes*

Universidad & Empresa, vol. 21, no. 36, 2019

Universidad del Rosario

Mudassar Hasan ** Mudassar.hassan@lbs.uol.edu.p

University of Lahore, Pakistán

Muhammad Ishfaq Ahmad *** pakistanmuhammad.ishfaq@lbs.uol.edu.pk

University of Lahore, Pakistán

Muhammad Abubakr Naeem **** M.ab.naeem@gmail.com

Massey University, Nueva Zelanda

Muhammad Akram Naseem ***** iqra4ever@hotmail.com

Universityof Lahore, Pakistán

Ramiz-ur Rehman ****** Ramiz_rehman@hotmail.com

University of Lahore, Pakistán

Received: 29 January 2018

Accepted: 12 June 2018

Additional information

To cite this article : Hassan, M., Ahmad, M. I., Abubakr, M., Naseem, M. A., & Rehman, R. (2019). Examining the Spillover Effect between the KSE100 and the S&P500 Indexes. Universidad & Empresa, 21(36), 175-195. DOI: https://doi.org/10.12804/revistas.urosario.edu.co/empresa/a.6472

Abstract: The volatility spillover is defined as the transmission of instability from market to market. It occurs when the volatility price change in one market causes a lagged impact on volatility price in another market above the local effects of market. In this study the garchmodels are used to examine the possibility of volatility transmission between the KSE100 index (Pakistan) and S&P500 index (usa); in other words, to examine how the volatility in one market mayinfluence the other and vice versa. The egarchmodel is also applied and it was observed that our attempt to analyze symmetry and persistence in the KSE100 index and the S&P500 index volatility proved that there is clear evidence that shocks to the volatitlity of the KSE100 and S&P500 indexes have asymmetric and persistent effects. It is observed from the study that the shocks to the stock returns in one market do not transmit to the other; in other words, it appears that there is no spillover effect between the two stock markets.

Keywords Volatility, spillover, GARCH, EGARCH, KSE100 index, S&P500.

Resumen: El derrame volátil es definido como la inestabilidad entre mercados. Sucede cuando el precio de la volatilidad cambia en un mercado causando un impacto rezagado en el precio de la volatilidad en otro mercado que se encuentra por encima los efectos locales del mercado. En este estudio los modelos GARCH son utilizados para examinar la posiblidad de transmición de volatilidad entre el índice KSE100( Pakistan) y el índice S&P500 (Estados Unidos). En otras palabras, para examinar la influencia de la volatilidad en otro y vice versa. El modelo EGCARCH también fue aplicado y se observa nuestro intento por analizar la simetría y la persistencia de la volatilidad en el KSE100 y el S&P500, se evidencia con claridad que choques en la volatilidad de ambos tiene un efecto asimetrico y persistente. A partir del estudio se observó que los choques al rendimiento de las acciones en un mercado no se transmiten al otro, en otras palabras, no hay presencia de efecto de derrame entre las dos bolsas de Valores.

Palabras clave: volatilidad, derrame, GARCH, EGARCH, KSE 100, S&P500.

Resumo: O derramamento volátil é definido como a instabilidade entre mercados. Acontece quando o preço da volatilidade muda em um mercado causando um impacto atrasado no preço da volatilidade em outro mercado que se encontra por cima dos efeitos locais do mercado. Neste estudo os modelos GARCH são utilizados para examinar a possibilidade de transmissão de volatilidade entre o índice KSE100 (Paquistão) e o índice S&P500 (Estados Unidos). Em outras palavras, para examinar a influência da volatilidade em outro e vice-versa. O modelo EGCARCH também foi aplicado e se observa nossa tentativa por analisar a simetria e a persistência da volatilidade no KSE100 e o S&P500, se evidencia com claridade que choques na volatilidade de ambos os dois tem um efeito assimétrico e persistente. A partir do estudo se observou que os choques ao rendimento das ações em um mercado não se transmitem ao outro, em outras palavras, não há presença de efeito de derramamento entre as duas bolsas de Valores.

Palavras-chave: volatilidade, derramamento, GARCH, EGARCH, KSE 100, S&P500.

Introduction

Forecasting stock market volatility isrecently an emerging subject for researchers. It is important for the selection of better portfolio as well as for pricing and management of assets. The current study is concerned with modeling volatility and researching volatility transmission effect between two stock exchanges, Karachi Stock Exchange (KSE-100) and S&P500. The emerging markets, encountered to a number of financial and currency crises around the globe, led the academics and practitioners to relook the volatility spillover states among the stock markets of the same nation and across the nation as well.This has resulted in large correlated engagements leading to market contagion.

It was reported in the 1990s (Harvey, 1995) that emerging markets tend to show average returns but low volatility overall. Moreover, they are less exposed to risk factors pertaining worldwide and show petite integration. Therefore, it is important to study the volatility aspect in emerging markets along with emergent markets. It is also important to understand the factor of volatility within the stock markets of a single country. It is obliging for the inter-market and across the market pricing of specific securities, in order to trade and hedge those securities. Moreover, it is also supportive for formulating the regulatory policies for an emerging market like Pakistan, who is promptly getting assimilated in the economy at global level.

The reforms in the financial sector of Pakistan has opened up the doors for stock markets towards the global economic system and thus adopting the flexible system of exchange rate. This has caused a rapid upsurge in portfolio investment influxes. This investment is helpful in investable funds levitationand, on the other hand, it also produces desolate swings in the share markets. Similarly, the indexes of Pakistan have also increased with the passage of time. For instance, in 1995 the Karachi Stock Exchange (KSE-100) index of Pakistan amplified to 2600 but in 2005, the index was declined to seven thousand marks. Thus, it was contended that bullish markets bear high volatility as compared to bear markets (Quyyum & Kemal, 2006). However, the economic as well as the financial turbulence through 2008–2009 increased the interest of understanding the procedure of transmitting the information among economic and financial markets (Dooley & Hutchinson, 2009).

There will be various studies looking into countless aspects of stock markets of Pakistan by the investment communities and academia around the globe. However, the current study will take into consideration the two imperative facets of the Pakistan stock market. Principal facet is the volatility returns for Pakistan's equity market, as it is a vital input for financial products’ pricing and the decisions of asset provision. For the respective purpose, garch type models have been evidently employed by many studies that have appeared able to forecast share market returns in international stock markets, exposing clusters in volatility (Akgiray, 1989; Baillie & DeGennaro, 1990; Kim & Kon, 1994). The current study will also consider the garchmodel for respective purpose, as it considers the countless physiognomies of data. The subsequent facet will studythe transmission procedure of volatility between Pakistan’s twoequity exchanges; KSE-100 and LSE-25. In literature, this volatility transmission is denoted as the effect of volatility spillover, and this effect has been studied abundantly among different countries (Ng, 2000; Baur & Jung, 2006).

The volatility behavior in stock market has gained increased interest since the 1990s. Volatility refers to the variations; it tends to happen in financial stock markets, causing various effects in return. This factor has also been researched in time series analysis by various researchers. Poterba and Summers (1986) argued that volatility can have significant impact on share prices, only if shocks to volatility tend to persist for a longer period of time. Furthermore, financial time series have a stylized fact that it contains higher volatility in certain periods. Such volatility phases correspond to economic events that incline major effects, like stock market crushes. Such variations in return can be forecasted through specific time series models, of which generalized autoregressive conditional heteroscedasticity (garch) model is the most common and successful one (Franses & Dijk, 1996).

Volatility spillover is defined as the transmission of instability from market to market. It occurs when volatility price change in one market cause a lagged impact on volatility price in another market above the local market effects. These patterns have predominantly widespread in financial markets. The researches have studied the spillover effects in various market sectors;the extensive research has been conducted in exchange rates (Engle et al., 1990; Baillie & Bollerslev, 1990), equity markets (Hamao et al., 1990; Lin et al., 1994), futures contracts (Abrhyankar, 1995; Pan & Hsueh, 1998), also in the equities and exchange rates (Apergis & Rezitis, 2001).

It has been noticed that by commercial canons, the overall impression of volatility spillover might not be large but it is substantial statistically. Moreover, no additional costs occur if the process of portfolio selection comprehends the effects of volatility spillover. Instead, the small gains signify improvements forinvestors. The findings of the aforementioned researches have summarized the volatility spillover effects as follows:(1)stock returns have time varying volatility; (2)mean and volatility spillovers are substantial from us stock markets to other national markets; (3)the stock market crash of 1987 has widely changed the configurations of information transmission (Cheung & Ng, 1992; Theodossiou & Lee, 1993; Susmel & Engle,1994).

Several financial crises have been witnessed in recent years, which have instigated in developing economies and then have spread across other economies in a shorter time span. The transmission of volatility in this regard is explained as the magnitudes of real as well as financial interrelations between the frugalities. It can also be regarded as the result of activities done by institutional investors having strong groundings in financial instruments of emergent markets. These investors lessen the portfolio’s riskwhen high returns and high-risk positions are sold in the situation of crises (Kaminsky & Schmukler, 1999).

Similar to the simple volatility factor, the prevalent approach for the test of volatility or shocks transmission in financial stock markets is also that of thegeneralized autoregressive conditionally heteroscedastic (garch) models. This model was proposed by Engle (1982) and Bollerslev (1986). The garch models are able to deliver volatility forecasts. They are obliging for modeling the volatility’s historical process as well as providing multi-period future projections. These forecasts are important to the stock market data applications; like allocation of portfolios, vibrant optimization and pricing of options (Goyal, 2000).

However, it has been noticed that tests based on garch models do not permit to discriminate the phases of low volatility called calm periods and the high volatility called crises. garch models are symmetric both in parameterization economy as well as temporal causality. Parameterization causality represents an economy which affects the other economy in same way during calm and crises periods, whereas, temporal economy focuses on affecting the future volatility of other economies, both in calm phases and crises. Thus, garch models are not seemed to accommodate the explanations of crises that are economic as well as financially prevailing (Solaa et al., 2002).

Numerous researches reveal that garch models are popularly rich in capturing the stylized particulars of financial time series with flexible configurations, such as clustering of volatility. This clustering is defined as the propensity of similar magnitude of volatility phases to cluster. This time varying phenomenon of volatility can be considered over a longer period of time through garch specific models, providing better in-sample estimates (French et al., 1987;Franses & Van Dijk, 1996). Furthermore, it is also argued that garch models are perfect in providing future volatility projections, even if the researchers study a case having a good in-sample fit but the anticipating performances are poor (Andersen & Bollerslev, 1998).

The phenomenon of volatility spillover has a major influence on pricing of assets and also leads to the opportunities of arbitrage. The current study is designed to see if there exist the volatility spillover effect between the S&P500 (usa) and KSE100 (Pakistan) indexes.

1. Research Hypothesis

Ho: There does notexist the volatility spillover effect between the S&P500 and the KSE100 indexes.

H1: There exists the volatility spillover effect between the S&P500 and the KSE100 indexes.

2. Research Question

Does there exist the volatility spillover effect between the S&P500 and the KSE100 indexes?

3. Literature

The stock market crash of October 1987, intensified the interests of researchers regarding volatility spillover across international stock markets. This happened when us equity markets faced a sharp drop and produced a pervasive domino effect across global equity markets. This interest was further developed in national equity markets as well along with international markets comparison. The crash of 1987 was first studied by King and Wadhwani (1990).

The results indicated volatility innovations across equity markets and these innovations tend to transmit information of price, even if it is market specific information. It was argued in the study that markets contain contagion effects and, regardless of the information’s pecuniary value, these markets overreact due to the events of other stock markets.

There are two ways in which the effect and the integration of price and volatility transmission between equity markets can be interpreted, and similarly the momentous interrelationships can also be inferred in these two ways. First, there can be a causal relationship among equity markets, such that the volatility in one market is induced by the volatility in another market. This is called lead-lag relationship. This can be possible only due to different trading hours in two respective countries. Second way is the influence of international factors that are common to both markets. Ultimately, this gives rise to a causal relationship between two markets apparently (Mishra et al., 2007).

The volatility behavior in the MENA market was also studied extensively at the level of market index. icss (iterated cumulative sums of squares), had been used by Hammoudeh & Li (2008) to studythe impact of sudden volatility changes in five stock markets of gcc at the level of market index on the persistence of forecasted volatility. The results identified the respective stocks to be more effected by global events rather than regional or local ones. The volatility persistence was also examined by another researcher along with the comparison of time-varying volatility in wtiand European Brent stock markets. The study reported the existence of volatility persistence and noteworthy leverage effect in the stock market of European Brent (Cheong, 2009).

Along with volatility, the transmission of volatility effect has been an emerging issue of study for researchers. The volatility spillover literature can be classified in two groups. The first one considers series of return or errors in order to model series of returns and their relationship across stock markets. It was explained by Eun and Shim (1989) that innovations in some equity markets explain almost 26 percent error variance in returns of equity markets and it was found that the most influential equity market is us market. The other group, however, scrutinizes volatility directly.

The study, conducted by Theodossiou and Lee (1993) stated various results regarding volatility spillover effects across the borders of various republics. It was found that us stock markets radiate fragile mean spillovers to Canada, the uk and Germany and also from Japan to Germany. Less than six percent of the entire variations in returns were explained by these volatility spillovers in the respective markets. Therefore, the conditional volatility in such markets was derived from us markets. Further, the cross volatility spillover factor was found to be noteworthy from us equity markets to uk, Japanese, German and Canadian markets, further from Germany to Japan and also from the uk to Canada.

Lin et al. (1994) targeted us and Japanese markets for volatility transmission research. The results concluded a correlation between one market’s daytime return and volatility with another market’s overnight return and volatility factor. Thus, the effects of volatility transmission were established. The volatility transmission between stock markets of New Zealand and Australia was also studied by a researcher. It was found that the conditional volatility of the stock market of New Zealand is influenced by the volatility of the Australian equity market. Similarly, the Australian market’s volatility was also seen to be influenced by New Zealand’s market (Brailsford, 1996). It was also concluded in one study indicating the greater propensity of stock markets in active periods to transmit volatility rather than in tranquil phases (Andersen & Bollerslev, 1998).

The features of stock markets in emerging countries were studied by Sabri (2004). The researcher pointed out the highly allied indicators of growing volatility of equity markets and also emerging markets turbulence. The results depicted that stock price changes in emerging markets are highly positively correlated to volume to trading stock as well as exchange rate of currency. Similar studies of volatility spillover were also conducted considering foreign exchange as well as futures and cash markets. The foreign exchange markets of Central Europe were also studied with respect to the effects of volatility transmission (Bubak et al., 2010). The empirical results stated various volatility patterns in the currency of Central Europe. The period before 2008, the short as well as long term components of volatility in Hungarian Forint (HUF) affected the volatilities of both Polish Zloty (PLM) and Czech Koruna (CZK). Similarly, both these markets were also influenced by the us dollar long term components of volatility (USD). On the other hand, EUR/HUF volatility was not affected by any foreign component, other than EUR/CZK medium-term component of volatility. Also, only Hungarian Forint (HUF) reported to be the only currency that was not influenced by EUR/USD volatility components.

The geographical regimes shock also tend to have volatility spillover effects. The findings of Wei et al. (1995) stated that developed markets transmit volatility to developing markets and of them, the transmitted shocks effect more to smaller less emerging markets. Bakaert and Harvey (1997) in their spillover study across developing markets, distinguished global and local shocks and reported Pacific-Basin markets to be effected by regional factors rather than global ones. Baele (2003) studied country specific regional and global shock regarding spillovers for us and thirteen stock markets of Europe. The results depicted both global and regional effects to be significant. Christiansen (2003) conducted an examination related to the effects of volatility spillover from us to aggregate as well as the individual bond markets of Europe. Weak mean spillover effects were reported from us and aggregate markets to individual Europe markets, while strong effects of volatility spillover existed from us and aggregate Europe to individual markets.Moreover, regional factors were also regarded stronger than global factor for Asia region markets (Miyakoshi, 2009).

The erstwhile literature is full of studies related to volatility transmission or spillover effect in exchange rates crossways international markets. us is the main market considered in various studies. A similar research was conducted by Baillie and Bollerslev (1991) considering exchange spot rates across four countries’ currencies: DEM, GBP, CHF and JPY compared with USD. The period was taken as six months and the rates were recorded on the basis of hours. The results did not uncover the effects of volatility transmission presence among the currencies. Kearney and Patton (2000) researched such effects within EMS along with studying time aggregation effects on transmission of volatility. The result concluded smaller tendency of less volatile data (weekly) to transmit volatility rather than high volatile data (daily).

Kanas (2000) studied inter-economy exchange rate changes and stock returns interdependence. Six industrialized republics were considered for the respective purpose:us, Japan, uk, France, Germany and Canada. The results concluded the following points:(1)exchange rates and share prices were co-integrated; (2)except for Germany, all countries present spillover effects from share returns to changes in exchange rates; (3)the nature of volatility spillover from share returns to the changes in exchange rates is symmetric; (4)for all countries, the effect of volatility transmission is insignificant from changes to exchange rates to share returns; (5) egarch filtered returns of shares and changes in exchange rate present a negative correlation coefficient that is significant for all republics. Thus, the contemporaneous association between share price returns and changes in exchange rate indicated to be significant.

Exchange rates also studied showed a substantial influence on stock returns of expected industry as well as their volatility, even though the effect had small magnitude. It was also drawn from findings that the magnitude, exchange rate regime and exchange rate tremors direction were the reasons to influence the prominence of volatility spillovers of exchange rate (Bodart & Reding, 2001). The volatility relationship between the equity market of India and its nominal exchange rate was researched by Apte (2001). The results showeda volatility spillover effect from the foreign exchange market to India’s equity market, but the reverse scenario did not occur. The main limitation of the research was based on the fact that their data series consisted of stock markets periods, having long gaps for various days at a stretch.Thus, the reverse situation for the relationship did not happen at all. The empirical exploration led by Fang and Miller (2002) studied the era of the Korean financial disorder (1997-2000). The effects of daily currency devaluation on returns of the Korean equity markets were examined in the study. The results highlighted various findings:(1)the Korean equity market and the foreign exchange market contain a dual directional connection; (2)equity market returns are negatively affected by the level of exchange rate devaluation, however, the returns of stock markets are positively affected by the volatility of exchange rate devaluation. Thus, volatility of share returns responded to depreciation of exchange rate.

The effect of volatility spillover has been extensively examined by many researchers using garch type models. The volatility transmission effects between EMS members; prior to their comprehensive monetary amalgamation, was analyzed by Kearney and Patton (2000) using multivariate garch series models. The daily and weekly data had also been used for volatility transmission effects across equity markets. The respective studies also employed garch type models for conducting the test for volatility spillovers (Ng, 2000; Corradi et al., 2009).

However, other than being a simple garch model, many garch related models had been employed by researchers to examine the effects of volatility spillovers. Hammoudeh and Choi (2007) researched the volatility behavior for permanent and transitory modules of individual indices of the gccmarket. The study used a univariate garch approach along with the Markov switching model. Also, a trivariategarch approach was applied by Malik and Hammoudeh (2007) to examine effects of volatility spillovers for three gcc republics. The indices in the study included one individual index of the gcc market, the S&P 500 index and the wtioil price. Zarour and Siriopoulos (2008) employed garch model to examine volatility putrefaction existence into short as well as long run modules. The model was applied to the daily data of index returns for Middle East region’s nine emerging markets, including three gcc republics.

All this literature requires further researchin emerging markets for the effects of volatility spillovers using garch type models

4. Methodology and Results

4.1.Modeling Volatility for the S&P500 and the KSE100 Indexes

The econometric package STATA 12.0 is used for applying the garch modeling on the data sets. The data used is thedaily closing index prices of the S&P500 and KSE100 indexes acquired from Yahoo Finance. The sample period is from January 1, 2010 to December 31, 2015, with a total of 1488 observations for both markets.The daily returns were evaluated as the change in natural log of closing prices of succeeding days:

Akgiray (1989) observed that the return series given by Rt = In (St) ─ In (St - 1) can be stated as a white noise process and it should be i.id (identically and independently distributed) with mean=0 and constant variance. Moreover, the series of Rt in absolute and squared form are supposed to show a minimum of autocorrelation.

The results of our analysis showthat the series of returns on indices of both markets are not pure white noise.

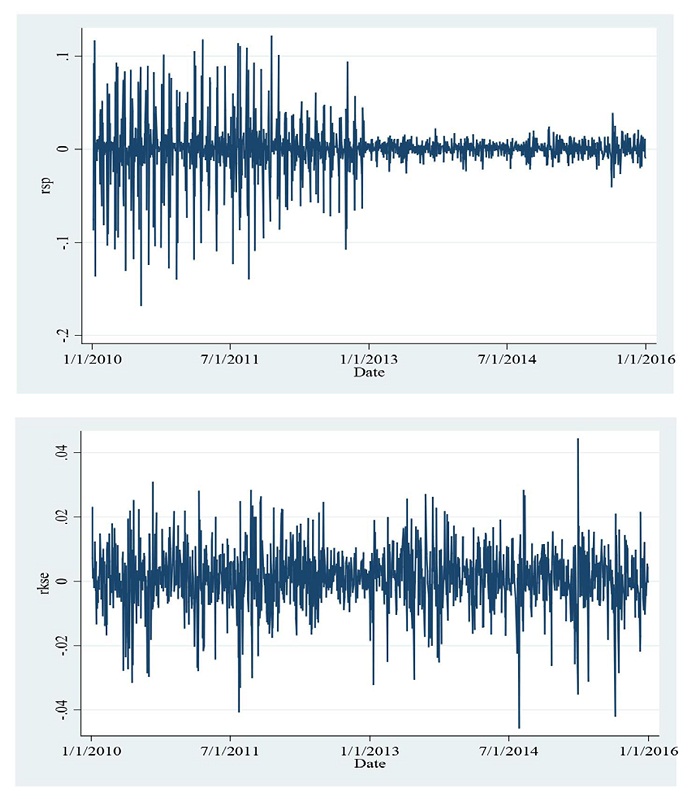

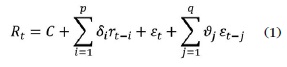

From Figure 1, we can see that volatility clustering, as there areareas with high volatility followed by areas of low volatility. The descriptive statistics presented in Table 1 shows that both stock returns are also not normally distributed.

The Shapiro-Wilk test of normality was applied on the return series having a null hypothesis of normal distribution. The results of the testspecify that the null hypothesis can be rejected for both series.

4.2. garch Models for the S&P500 and KSE100 Indexes

The proposed model is given by:

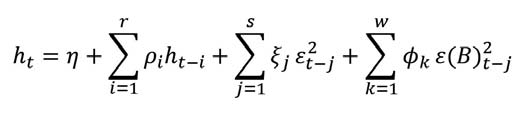

The above equation represents the ARMA (p, q) process, and the conditional variance (ht) for the above equation is represented as:

Where the parameters in (2) should satisfy: α0 > 0,ρi,ξj> 0, i = 1,...,r, j = 1,...,S.

Engle, Lilien, and Robins (1987) established that higher expected returns in share pricesare observed with an increase in risk (variance). For this purpose,the garch-M (garch in mean)model is introduced which is an extension of the garch model. In this model a conditional variance termis introduced. The model is given as:

The relationship between the stock return volatility and the sign of stock returns is also one of interest. It is argued by Engle and Ng (1993) thatthe stock returns and the volatility have an inverse relation, i.e. when one decreases the other increases and vice versa. The phenomenon defined above is called “leverage effect”. It may be modeled by the asymmetric volatility model or egarchmodel and is given as:

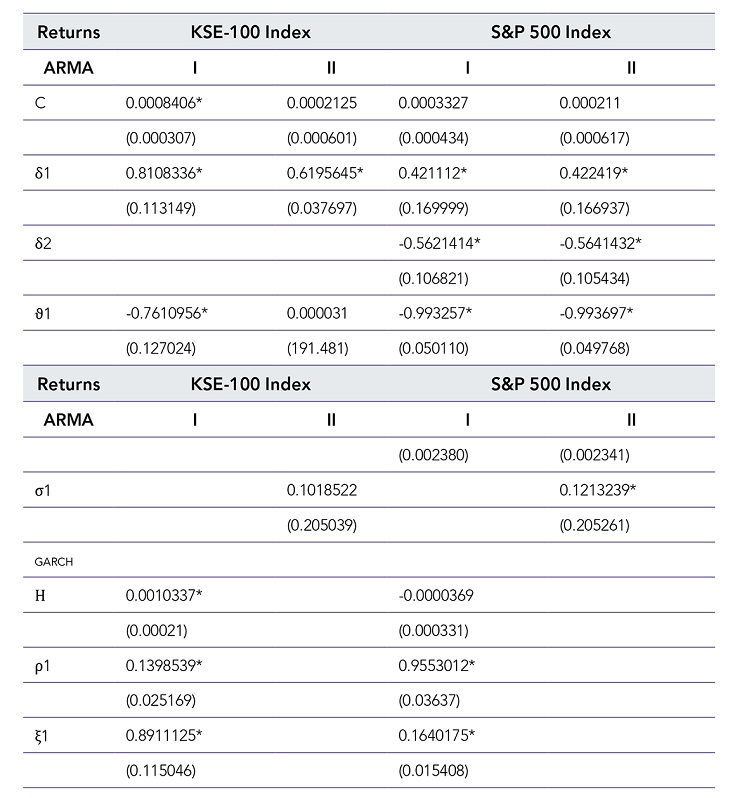

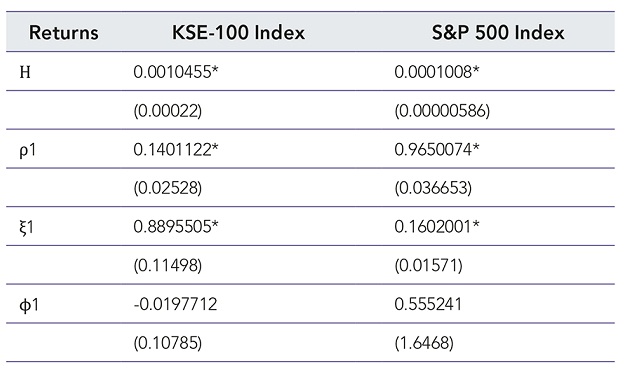

The final garch specification is selected by looking at the properties of standardized residuals. The residuals should be i.i.dand follow the normal distribution with mean zero and constant variance.

We favor the egarch model because the it does not impose restrictions on, and . The β-estimate allows evaluating whether shocks are persistent or not |β|<1.If it shows the stationarity of data that is required for the analysis of time series. The parameter deals with the asymmetric volatility. When γ>0 it means the positive shocks have given rise to higher volatility. The extent of conditional shocks on conditional variance is symbolized as α.

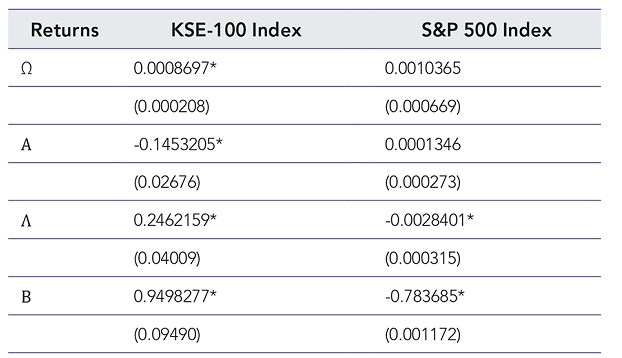

From the results we can see that the KSE100 index returns that coefficient is positive and significant at 1%, but the coefficient is negative for the S&P500 index returns. Hence, we can say that the positive shocks have more impact on volatility of the KSE100 index, whereas negative shocks have more impact on the volatility of the S&P500 index. In other words, we can also say that it shows that shocks have an asymmetric effect on both indices as both negative and positive shocks have unlike impact on the volatility. The β-coefficient captures endurance of shocks. The advantageous price of the coefficient for the KSE100 index shows that the shocks generally tend to persist over lengthy time frames, and the negative price of the coefficient for the S&P500 index shows that the shocks have a tendency to persist over shorter time frames. The value of the α coefficient is -0.145 for the KSE100 index and 0.0001346 for the S&P500 index, which suggests the magnitude of the conditional shocks. As it is the magnitude then we can ignore the negative sign. The α coefficient for the S&P500 index isnot statistically significant. Consequently, it will have a very little effect on the model. In sum, our attempt to examine symmetry and determination of the volatility of the KSE100 and the S&P500 indexes, proves that there is clean evidence that shocks to the KSE100 index and S&P500 index volatility have an uneven and continual effect.

5. The Spillover Effect (Volatility Transmission)

The idea of volatility spillover was first proposed by Hamao, Masulis and Ng (1990) to examine the short-run interdependence of price volatility across the New York, Tokyo and London stock markets.Here we have used the garch models to examine the possibility of spillover effect between the KSE100 and the S&P500 indexes in order to examine that the volatility in one market will influence the other and vice versa. A lagged squared error term from the mean equation of the garch model for market B is introduced in the garch model for market A to model the spill-over effect for both markets. The spill-over effect from market B to market A canbe captured by the following specification:

Where ε(B) shows the previous shocks to market B. The coefficients (i.e., the ϕs) measure the impact of past shocks to the returns of market B on the conditional volatility of market A.

The estimation results for the garch (1,1) spillover model are provided in the table below.

From the above table we can see that the estimates of the ϕs for the two markets are insignificant which suggests that shocks to the stock returns in one market have no effects on the other; in other words, we can say that there is no spillover effect between the two stock markets.

Conclusion

In this study we have used the garch models to examine the possibility of volatility transmission between the KSE100 and the S&P500 indexes. In other words, to examine if the volatility in one market will influence the other and vice versa. The egarch model is also applied and it is observed that our attempt to analyze symmetry and persistence in the volatility of the KSE100 and the S&P500 indexes, there is clear evidence that shocks to KSE100 index and S&P500 index volatility have an asymmetric and persistent effect. It is observed from the study that the shocks to the stock returns in one market do not transmit to the other; in other words, there appears to be no spillover effect between the two stock markets.

References

Abhyankar, A. H. (1995). Trading Round-the-Clock: Return, Volatility and Volume Spillovers in the Eurodollar Futures Markets. Pacific-Basin Finance Journal, 3, 75-92.

Akgiray, V. (1989). Conditional Heteroscedasticity in Time Series of Stock Returns: Evidence and forecasts. Journal of Business, 62(1), 55-80.

Anderson, T., & Bollerslev, T. (1998). Answering the Skeptics: Yes, Standard Volatility Models do provide accurate Forecasts. International Economic Review, 39(4), 885-905.

Apergis, N., & Rezitis, A. (2001). Asymmetric Cross-Market Volatility Spillovers: Evidence from Daily Data on Equity and Foreign Exchange Markets. Manchester School, 69, 81-96.

Apte, P. J. (2001). The Inter-Relationship between Stock Market and Foreign Exchange Market. Prajnan, 10(1), 17-29.

Baele, L. (2003). Volatility Spillover Effects in European Equity Markets. Ghent University Working Paper.

Baillie, R., & Bollerslev, T. (1990), A Multivariate Generalized ARCH Approach to Modeling Risk Premia in Forward Foreign Exchange Rate Markets. Journal of International Money and Finance, 9(3), 309-324.

Baillie, R., & Bollerslev, T. (1991). Intra-Day and Inter-Day Volatility in Foreign Exchange Rates. Review of Economic Studies, 58, 565-585.

Baillie, R. T., & DeGennaro, R. P. (1990), Stock Returns and Volatility. Journal of Financial and Quantitative Analysis, 25, 203-214.

Baur, D., & Jung, R. C. (2006). Returns and Volatility Linkages between the us and German Stock Markets. Journal of International Money and Finance, 25, 598-613.

Bekaert, G., & Harvey, C. R.(1997). Emerging Equity Market Volatility. Journal of Financial Economics 43(1), 29-77.

Bodart, V., & Reding, P (2001). Do Foreign Exchange Markets Matter for Industry Stock Markets? An Empirical Investigation.

Bollerslev, T. 1986. Generalized Autoregressive Conditional Heteroscedasticity. Journal of Econometrics, 31, 307–27.

Brailsford, J. (1996). Volatility Spillovers across Tasman. Australian Journal of Management, 21(1), 13-27.

Bubak, V., Kosenda, E., & Zikes, F. (2010). Volatility Transmission in Emerging European Foreign Exchange Markets. Monetary Policy and International Finance, 3-47.

Cheong, C. W. (2009). Modeling and Forecasting Crude Oil Markets Using ARCH-Type Models. Energy Policy, 37, 2346-2355.

Cheung, Y. W., & Ng, L. K. (1992). Interactions between the us and Japan Stock Market Indices. Journal of International Financial Markets, Institutions, and Money, 2, 51–70.

Christiansen, C. (2003). Volatility-Spillover Effects in European Bond Markets. Centre for Analytical Finance, Aarhus School of Business, University of Aarhus.

Corradi, V., Distaso, W., & Fernandes, M. (2009). International Market Links and Volatility Transmission. Working Paper, Warwick University, Imperial College London and Queen Marry College.

Dooley, M., & Hutchison, M. (2009). Transmission of the ussubprime Crisis to Emerging Markets: Evidence on the Decoupling-Recoupling Hypothesis. Journal of International Money and Finance, 28(8), 3-29.

Engle, R. F., Ito, T., & Lin, W. L. (1990). Meteor-Showers or Heat Waves? Heterskedastic Introdaily Volatility in the Foreign Exchange Market. Econometrics, 58(3), 525-542.

Eun, C. S., & Shim, S. (1989). International Transmission of Stock Market Movements. Journal of Financial and Quantitative Analysis, 24, 241-256.

Fang, W., & Miller, S. (2002). Currency Depreciation and Korean Stock Market Performance during the Asian Financial Crisis.

Franses, P. H., & Dijk, D. V. (1996). Forecasting Stock Market Volatility Using (Non-Linear) garch Models. Journal of Forecasting, 15, 229-235.

French, K. R., Schwert, G. W., & Stambaugh, R. E. (1987). International Transmission Offstock Markets Movements. Journal of Financial and Quantitative Analysis, 24, 241-256.

Goyal, A. (2000). Predictability of Stock Return Volatility from garch Models. Journal of Finance, 1-44.

Hamao, Y., Masulis, R. W., & Ng, V. K. (1990). Correlations in Price Changes and Volatility across International Stock Markets. Review of Financial Studies, 3(2), 281-307.

Hammoudeh, S., & Choi, K. (2007). Characteristics of Permanent and Transitory Returns in Oil-Sensitive Emerging Stock Markets: The Case of gcc Countries. International Review of Economics and Finance, 17, 231-245.

Hammoudeh, S., & Li, H. (2008). Sudden Changes in Volatility in Emerging Markets: The Case of Gulf Arab Stock Markets. International Review of Financial Analysis, 17, 47-63.

Harvey, C. (1995). Predictable Risk and Returns on Emerging Markets. Review of Financial Studies, 773-816.

Kaminsky, G. L., & Schmukler, S. L. (1999). What Triggers Market Jitters? A Chronicle of the Asian Crisis. Journal of International Money and Finance, 18(4), 537–560.

Kanas, A. (2000). Volatility Spillovers between Stock Returns and Exchange Rate Changes: International Evidence. Journal of Business Finance and Accounting, 27, 447-468.

Kearney, C., & Patton, A. J. (2000). Multivariate garch Modeling of Exchange Rate Volatility Transmission in European Monetary System, The Financial Review, 41, 29-48.

Kim, D., & Kon, S. (1994), Alternative Models for the Conditional Heteroscedasticity of Stock Returns. Journal of Business, 67, 563-598.

King, M. A., & Wadhwani, S. (1990). Transmission of Volatility between Stock Markets. The Review of Financial Studies, 3, 5-33.

Lin, W., Engle, R., & Ito, T. (1994). Do Bulls and Bears Move across Borders? International Transmission of Stock Returns and Volatility. Review of Financial Studies, 7, 507-38.

Malik, S., & Hammoudeh, S. (2007). Shock and Volatility Transmission in the Oil, us and Gulf Equity Markets. International Review of Economics and Finance, 17, 357-268.

Mishra, A. K., Swain, N., & Malhotra, D. K. (2007). Volatility Spillover between Stock and Foreign Exchange Markets: Indian Evidence. International Journal of Business, 12(3), 344-359.

Miyakoshi, T. (2003). Spillovers of Stock Return Volatility to Asian Equity Markets from Japan and the us. International Financial Markets, Institutions and Money, 13, 383-399.

Ng, A. (2000). Volatility Spillover Effects from Japan and the us to the Pacific-Basin. Journal of International Money and Finance, 19, 207-233.

Pan, M. & Hsueh, P. (1998), Transmission of Stock Returns and Volatility between the us and Japan: Evidence from Stock Index Futures Markets. Asia-Pacific Financial Markets, 5, 211-225.

Poterba, J., & Summers, L. (1986). The Persistence of Volatility and Stock Market Fluctuations. American Economic Review, 71, 421-436.

Qayyum, A., & Kemal, A. R. (2006). Volatility Spillover between the Stock Market and the Foreign Exchange Market in Pakistan. Pakistan Institute of Development Economics, 3-19.

Sabri, N. (2004). Stock Solaa, M., Spagnolo, F., & Spagnolo, N. (2002). A Test for Volatility Spillovers, 1-8.

Susmel R., & Engle, R. F. (1994). Hourly Volatility Spillovers between International Equity Markets. Journal of International Money and Finance, 13, 3–25.

Theodossiou, P., & Lee, U. (1993). Mean and Volatility Spillovers across Major National Stock Markets: Further Empirical Evidence. Journal of Financial Research, 16, 337–50.

Wei, K. C. J., Liu, Y. J., & Yang, C. C. (1995). Volatility and Price Change Spillover Effects across the Developed and Emerging Markets. Pacific-Basin Finance Journal, 3, 113-136.

Notes

*

This

article has been presented in the 7th International Interdisciplinary Business

Economics Advancement Conference, on April 2017; an abstract has been

published.

Author notes

**

Mphil. Degreefromthe Universityof Lahore, Lahore Punjab Pakistan.

His research interest is investment strategies in stock markets. Currently he

isserving as Assistant Professor of Finance in the Accounting and Finance

Department of Lahore Business School at the University of Lahore, Punjab

Pakistan. E-mail: Mudassar.hassan@lbs.uol.edu.p

***

Ph.D in Management Science & Engineering from

the Liaoning Technical University, Fuxin, Liaoning China. He has teaching experience of more

than eight years and is currently serving as Assistant Professor of Finance in

the Accounting and Finance Department oft he Lahore Business School at the

University of Lahore, Punjab, Pakistanmuhammad.ishfaq@lbs.uol.edu.pk

**** Currently pursuing his PhD in School of Economics and

Finance, Massey University, Albany, New Zealand. E-mail: M.ab.naeem@gmail.com

*****

He did his PhD

in the School of Management at the Xi’an Jiaotong University, China. He has

served in the central bank of Pakistan as Deputy Director, statisticsdepartment

and now serving as Assistant Professor in the Lahore Business School at the

Universityof Lahore, Punjab, Pakistan. E-mail:iqra4ever@hotmail.com

******

Ph.D from the School of Management, Xi’an Jiaotong

University, China. He works as Associate Professor of Finance in Accounting and

Finance Department of the Lahore Business School at the University of Lahore,

Punjab, Pakistan.E-mail: Ramiz_rehman@hotmail.com