10.12804/revistas.urosario.edu.co/empresa/a.14685

SCIENTIFIC AND TECHNOLOGICAL RESEARCH ARTICLE

Melvin S. Sarsale1

1 Southern Leyte State University (Philippines).

msarsale@southernleytestateu.edu.ph

msarsale@southernleytestateu.edu.ph

0000-0003-4591-5020

0000-0003-4591-5020

Received: July 11, 2024

Approved: May 5, 2025

To cite this article: Sarsale, M. S. (2025). The mediating effect of innovativeness on the relationship between financial literacy and risk-taking propensity: Implications for graduates' readiness for entrepreneurship. Universidad y Empresa, 27(49), 1-20. https://doi.org/10.12804/revistas.urosario.edu.co/empresa/a.14685

Abstract

Objective: This article examined the mediating role of innovativeness between financial literacy and risk-taking tendency and its implications for graduates' preparedness for self-employment.

Methodology: This research employed a cross-sectional design with 157 students at a Philippine state university.

Key findings: Filipino students who were surveyed had moderate financial literacy and entrepreneurial characteristics. Financial literacy, risk-taking willingness, and innovativeness also have a significant relationship. In addition, innovativeness mediates financial literacy and risk-taking willingness.

Conclusion: Financial literacy and innovativeness influence entrepreneurial readiness. Graduates with these characteristics are more likely to be well-equipped to navigate the

challenges and seize the opportunities of entrepreneurship. In response,

educational institutions create specific interventions and educational programs

to help aspiring students become entrepreneurs and self-employed individuals,

help them manage and succeed in various aspects of their future entrepreneurial

ventures.

Keywords: financial literacy; risk-taking propensity; innovativeness.

Resumen

Objetivo: este artículo examina el papel mediador de la capacidad de innovación

entre los conocimientos financieros y la tendencia a asumir riesgos y sus

implicaciones para la preparación de graduandos para el auto-empleo.

Metodología: se empleó un diseño transversal con 157 estudiantes de una universidad estatal filipina.

Resultados principales: los estudiantes filipinos encuestados tenían moderados conocimientos

financieros y características empresariales. Los conocimientos financieros, la

disposición a asumir riesgos y la capacidad de innovación también tienen una

relación significativa. Además, la capacidad de innovación influye en los

conocimientos financieros y la disposición a asumir riesgos.

Conclusiones: los conocimientos financieros y la capacidad de innovación influyen en

la disposición empresarial. Los graduandos con estas características tienen más

probabilidades de estar bien preparados para afrontar los retos y aprovechar

las oportunidades del espíritu empresarial. En respuesta, las instituciones

educativas crean intervenciones y programas educativos específicos para ayudar

a los estudiantes aspirantes a convertirse en empresarios y trabajadores

autónomos, ayudarles a gestionar y tener éxito en diversos aspectos de sus

futuras iniciativas empresariales.

Palabras clave: conocimientos financieros; propensión al riesgo; capacidad de innovación.

Resumo

Objetivo: este artigo examinou o papel mediador da inovação entre a alfabetização financeira e a tendência ao risco, bem como suas implicações para a prontidão dos graduados para o empreendedorismo.

Metodologia: utilizou-se um desenho

transversal com 157 estudantes de uma universidade estadual nas Filipinas.

Resultados: os estudantes filipinos

pesquisados demonstraram alfabetização financeira e características

empreendedoras moderadas. Alfabetização financeira, disposição para assumir

riscos e inovação também apresentaram uma relação significativa. Além disso, a

inovação atua como mediadora entre a alfabetização financeira e a propensão

para assumir riscos.

Conclusão: a alfabetização financeira e

a inovação influenciam a prontidão empreendedora. Graduados com essas

características provavelmente tendem a estar mais bem preparados para enfrentar

os desafios e aproveitar as oportunidades do empreendedorismo. Diante disso, as

instituições de ensino podem criar intervenções e programas educacionais

específicos para ajudar estudantes aspirantes a se tornarem empreendedores e

profissionais autónomos, capacitando-os para lidar com diversos aspectos da

gestão e do sucesso em suas futuras atividades empreendedoras.

Palavras-chave: alfabetização financeira; propensão ao risco; inovação.

Introduction

The increasing financial market sophistication and global competition demand high entrepreneurial and finance literacy abilities from potential Filipino entrepreneurs. These skills are essential for solving problems, identifying niches, and attracting clients (Ranalan et al., 2022). By understanding finances, prospective investors have become well-equipped to cope with launching and growing the business (Morales, 2023). On the one hand, successful entrepreneurs are characterized by their willingness to take risks and venture into unfamiliar territory to achieve their goals (Al-Mamary & Alshallaqi, 2022). On the other hand, their creativity in formulating new ideas and solutions is equally essential for entrepreneurial success. Acknowledging the impact of financial literacy on risk-taking behavior and creativity in young Filipino entrepreneurs is important for their success and for promoting economic development (Guliman, 2020; Damoah, 2020).

When paired with financial literacy, a positive attitude toward risk becomes a key factor in the successful entrepreneurial journey of today's young Filipinos (Almeda et al., 2020). Entrepreneurship means trying to do the impossible, being open to unexpectedness, and being able to measure your risks (Quezon & Vergara, 2022). However, while the extent to which they are willing to bear such risks may vary, it ultimately influences the outcomes of their entrepreneurial ventures (Llanos-Contreras et al., 2020). As a result, identifying the factors that influence risk aversion—specifically among aspiring Filipino youth aiming to start a business—is essential for developing strategic plans to foster a culture of entrepreneurship and innovation in the country.

Innovativeness is one of the key factors that may influence the relationship between financial literacy and risk-taking propensity (Duréndez et al., 2023). Innovativeness-characterized by creativity, adaptability, and a readiness to generate new ideas-may moderate the relationship between the ability of financial literacy to decrease risk-taking propensity among young entrepreneurs (Tipu & Fantazy, 2023). Through this innovative and imaginative mindset, individuals become more inclined to take risks and pursue the launch of their own businesses (Shahzad et al., 2021). However, the mediating effect of innovativeness on this relationship has yet to be thoroughly examined, especially within the Philippine context. By studying this mediation effect, the researcher can gain crucial insights into how financial literacy influences risk propensity among young Filipino entrepreneurs.

The gap in the literature prompts this study to examine how financial literacy, risk-taking propensity, and innovativeness are interconnected among aspiring Filipino youth. Specifically, this research tries to know how financial literacy influences risk propensity and whether innovativeness influences this. By revealing these relationships, this study contributes to the current knowledge on the determinants of youth entrepreneurship in the Philippines. Also, the results of this research could be used to design intervention programs and educational initiatives aimed at increasing the financial literacy and entrepreneurial skills of young Filipino entrepreneurs, thereby fostering an environment for innovation and economic growth in the country.

Literature Review and Hypothesis Development

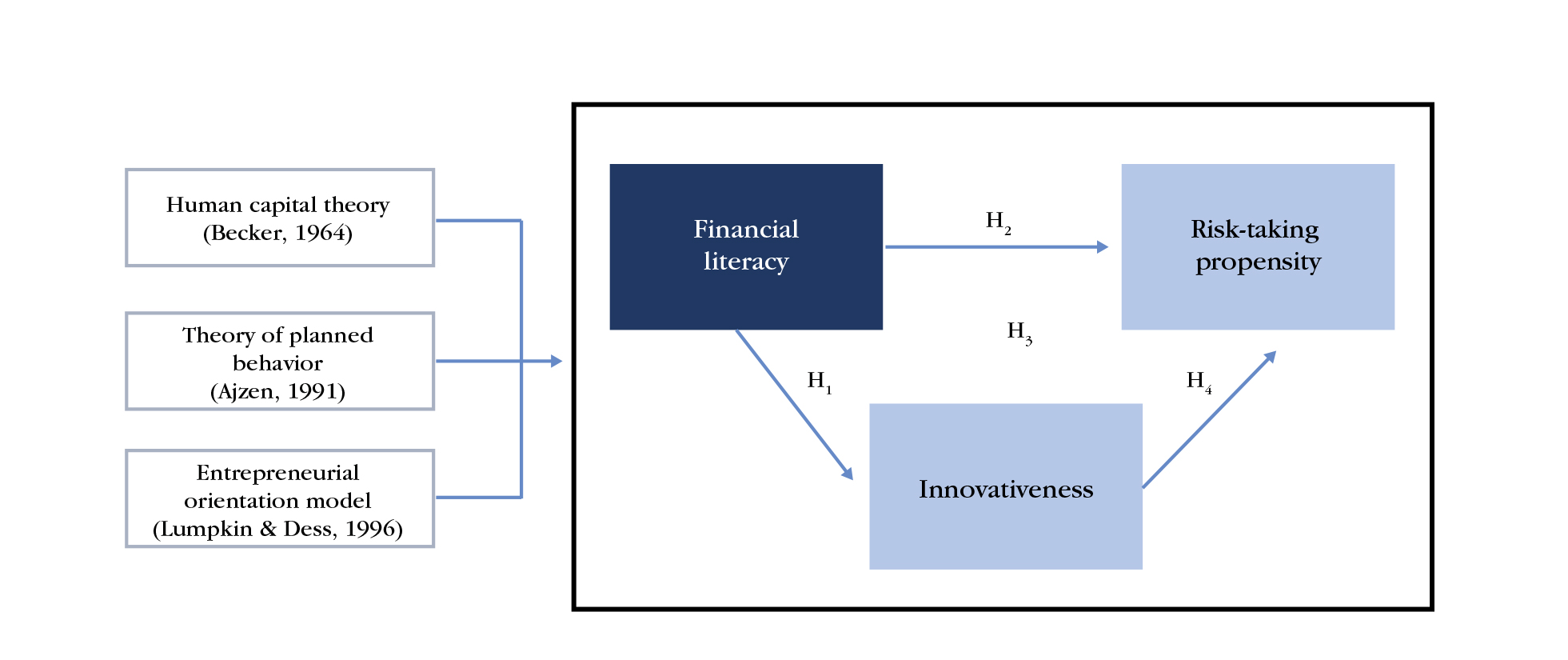

The three theoretical frameworks employed in this study are the human capital theory, the theory of planned behavior (TPB), and the entrepreneurial orientation (EO) theory. Human capital theory (Becker, 1964) emphasizes the effect of skills and knowledge, e.g., financial literacy, on an individual's economic success and career path. The TPB (Ajzen, 1991) describes the relationship between attitudes, perceived behavioral control, and intentions and how these factors shape behavior—providing a framework for understanding how risk-taking capability and financial knowledge might influence entrepreneurial intention. Meanwhile, the EO model (Lumpkin & Dess, 1996) sets innovativeness and risk-taking as key dimensions of entrepreneurial behavior. These theories help explain why internal capacities and external factors create graduates' entrepreneurial readiness.

Anchored on these theories, this study suggests a conceptual model incorporating innovativeness as a mediating variable between risk-taking tendency and financial literacy (see Figure 1). This theoretical advance draws from prior studies by explaining how financial knowledge is translated into entrepreneurial action using innovation. While previous studies have been familiar with examining these constructs independently, this framework brings them together per the dynamic interaction of the competencies needed to facilitate entrepreneurship.

Figure 1. Framework of the study

Source: Own elaboration.

Financial Literacy and Innovativeness

Financial literacy plays a significant role in building an entrepreneurial ecosystem, which is especially important for young entrepreneurs, as it helps establish strong connection between innovation and others (Burchi et al., 2021). Equipping aspiring entrepreneurs with fundamental financial skills will enable them to understand financial concepts, allocate resources, and make informed decisions—ultimately helping them identify and capitalize on entrepreneurial opportunities within their industries (Alshebami & Al Marri, 2022). Financial literacy fuels inventiveness, enabling young entrepreneurs to think, plan, and execute creative business plans that spur much-needed growth and profitability in today's competitive markets (Duréndez et al., 2023).

Furthermore, financial literacy fosters an environment of innovation and entrepre-neurship among young entrepreneurs by promoting continuous learning and exposure to risk and knowledge. This, in turn, contributes to economic growth, job creation, and social development (Liu et al., 2021). Closely connected with innovation-driven economic growth and society's development, an entrepreneur's financial literacy opens the way to entrepreneurial success and achieving a social mission. Therefore, financial literacy should be considered when designing a business.

H1: Financial literacy positively influences innovativeness.

Financial Literacy and Risk-Taking Propensity

To further realize the importance of financial literacy in entrepreneurial behavior, it is essential to recognize its influence on entrepreneurs' risk preference tendencies. Financial literacy, or the capacity to execute financial transactions, investments, and decision-making, is key to building a financially intelligent image (Fong et al., 2021). The extensive apprehension of financial perspective enables budding entrepreneurs to evaluate risks and determine the course of their business procedures regarding investments, resource allocations, and business strategy (Kulathunga et al., 2020; Ye & Kulathunga, 2019). In addition to being risk-takers, those with higher financial literacy tend to view risks as chances, being more confident even with uncertain ventures (Molina-García et al., 2023). Besides, financial literacy offers entrepreneurs the tools to mitigate risks and maximize profits, cultivating a culture of strategic risk-taking critical to entrepreneurial success (Adewumi, 2022).

Risk-taking is another benefit, as financial literacy supports innovations and start-ups (Shahzad et al., 2021). It develops economic choice confidence, makes people creative, and challenges standards. Financial literate and economically intelligent entrepreneurs are useful for market value formation, forecasting potential trends, and driving economic growth (Omoniyi & Bongani, 2022). Finally, the link between financial literacy and risk-taking also emphasizes the role of financial education as a driver behind entrepreneurial mindset and behavior, promoting a rich, unique, and healthy entrepreneurial culture (Ogbari, 2023).

H2: Financial literacy positively influences risk-taking propensity.

Financial Literacy and Risk-Taking Propensity through Innovativeness

Financial literacy positively enhances risk-taking by expanding people's knowledge of economic principles and resource management skills, leading to greater inclination toward taking calculated risks (Duréndez et al., 2023). However, a portion of this relationship is mediated by innovativeness, as those perceiving themselves as innovative exhibit a higher inclination towards risk-taking (Giaccone & Magnusson, 2022). It emphasizes innovativeness as a key mechanism through which financial literacy influences risk-taking (Duréndez et al., 2023). Furthermore, the mediation effect emphasizes the interrelatedness of psychological variables that shape entrepreneurial decision-making, suggesting consideration of financial literacy and innovativeness (Song et al., 2020). Policymakers and educators can utilize such insight to design interventions that promote financial literacy and innovativeness, thereby establishing entrepreneurial innovation and entrepreneurial success-conducive conditions.

H3: Innovativeness mediates the relationship between financial literacy and risk-taking propensity.

Innovativeness and Risk-Taking Propensity

For entrepreneurial behavior and success to be clearly understood, recognizing the critical connection between creativity and a propensity to take risks is warranted (Voda et al., 2019). The main driving force behind individuals' willingness to take risks in entrepreneurship is innovativeness, characterized by creativity, adaptability, and the ability to generate ideas (Williams et al., 2021). Those people who consider themselves creative are more likely to embrace risk, search for development opportunities, and even go beyond boundaries in their entrepreneurial activities (Murnieks et al., 2020). This thinking leads to contesting norms, developing new strategies, and entering business oddities with unpredictable outcomes.

Besides, the positive effect of the innovative process on risk-taking highlights its role as a subject of entrepreneurial innovation and improved economic performance (García-Lopera et al., 2022). In the dynamic business environment, creative people can understand and take quick action when business opportunities arise, driving economic growth by developing new products and services and opening new markets. Building entrepreneurial prowess among entrepreneurs is essential for entrepreneurial success and contributes to broader societal and economic development.

H4: Innovativeness positively influences risk-taking propensity.

Methodology

In examining the mediating role of perceived innovativeness on risk-taking tendency and financial literacy among prospective young Filipino entrepreneurs, the study used a quantitative research approach with a cross-sectional design, as it involves collecting data at a single point in time to provide a snapshot of the population of interest (Wang & Cheng, 2020). The study used a three-part survey instrument to gather the needed data among the 157 business students enrolled in a Philippine university.

The first part has three categorical questions and describes the respondents' socio-demographic characteristics. The second part consists of 42 Likert scale-type questions. It measures the student's financial literacy level using three essential subscales forwarded by Razafimahasolo et al. (2016), which include "cash management," "financial records," and "savings plans." The third part comprises 39 Likert scale-type questions. It evaluates the respondent's entrepreneurial characteristics using six subscales proposed by Anwar and Saleem (2019): "risk-taking propensity," "innovativeness," "locus of control," "need for achievement," "general self-efficacy," and "tolerance for ambiguity." The reliabilities of Cronbach's alpha of all subscales varied from 0.782 to 0.95, which far exceeded the recommended minimum limit of 0.70 (Urbach & Ahlemann, 2010). Moreover, the researcher obtained the necessary approval from the university before administering the survey. The researcher also ensured all respondents provided informed consent before taking the survey, and the anonymity of responses was guaranteed throughout the process.

Results

Socio-Demographic Characteristics of Aspiring Young Filipino Entrepreneurs

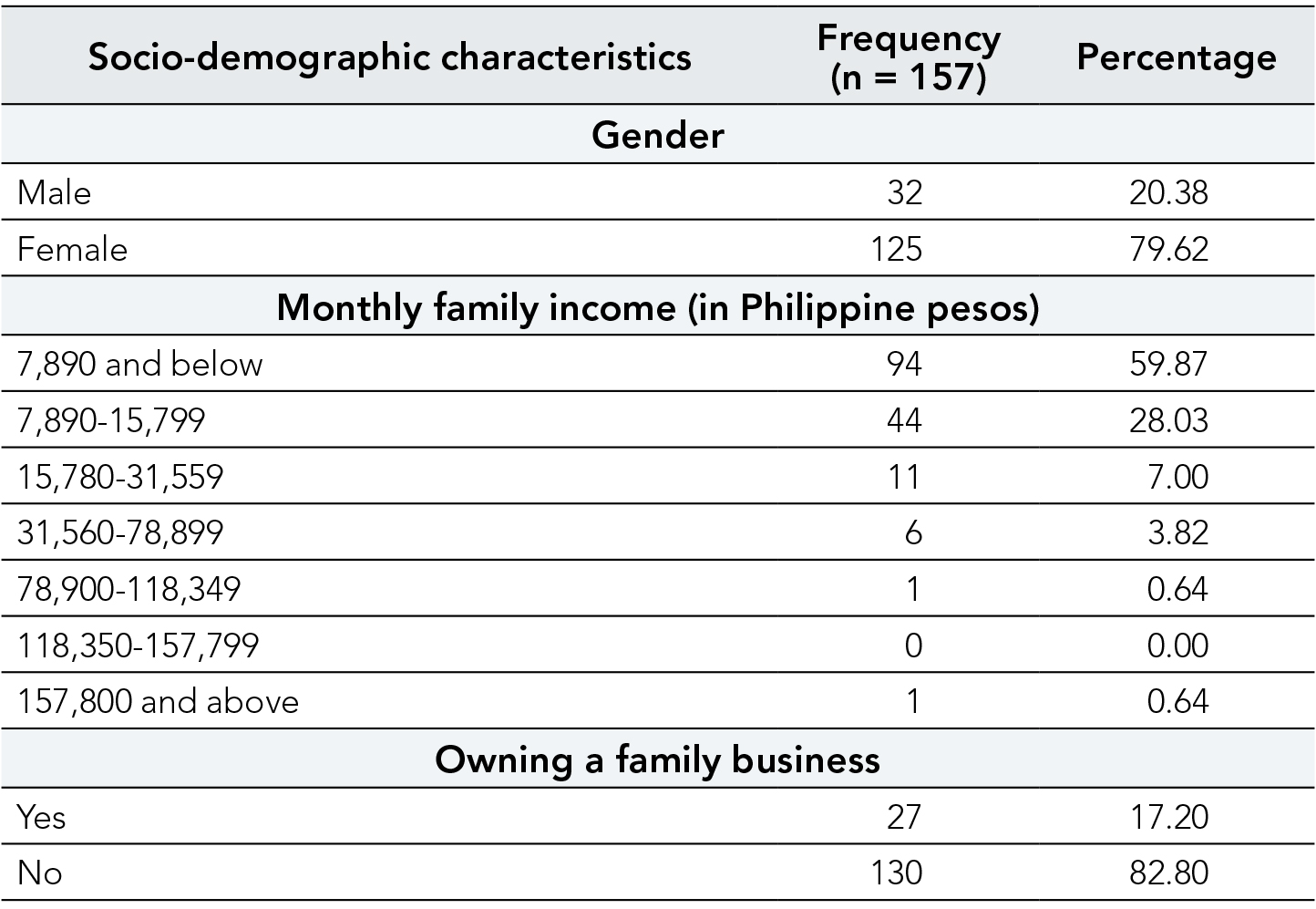

Table 1 presents respondents' socio-demographic profile details, including gender distribution, income, and having a family business. The gender distribution is mostly female (79.62 %) compared to male (20.38 %). Concerning monthly family income, most respondents (59.87 %) fall within the 7,890 and below Philippine pesos category and are typically low-income earners. At the same time, only a small percentage indicated higher income. Moreover, a minority of respondents (17.20 %) indicated owning a family business, while the majority (82.80 %) did not.

Table 1. Description of the respondent's socio-demographic characteristics

Source: Own elaboration.

Perceived Financial Literacy and Entrepreneurial Characteristics of Aspiring Young Filipino Entrepreneurs

Table 2 shows the descriptive statistics of aspiring entrepreneurs' assessment of their financial literacy and entrepreneurial characteristics. The financial literacy-oriented variables, cash management, financial records, and savings plans, show that respondents scored moderately high in financial literacy with fairly low standard deviations, indicating that most participants agreed. In addition, the above-mentioned entrepreneurial personality factors, including risk propensity, innovative behavior, perceived control, need for achievement, general self-efficacy, and ambiguity tolerance, are almost constant, with standard deviation values implying consistent responses from the subjects. This information reveals moderately high financial literacy among future entrepreneurs. The data also shares good entrepreneurial attributes, which can contribute to their success as entrepreneurs.

Table 2. Descriptive statistics of the aspiring entrepreneurs' assessment on their financial literacy and entrepreneurial characteristics

Variables |

Mean |

Std. |

Description |

Financial literacy |

3.918 |

0.475 |

Moderately high |

Cash management |

3.962 |

0.486 |

Moderately high |

Financial records |

3.830 |

0.545 |

Moderately high |

Savings plan |

3.960 |

0.570 |

Moderately high |

Entrepreneurial characteristics |

3.687 |

0.410 |

Moderately high |

Risk-taking propensity |

3.531 |

0.602 |

Moderately high |

Innovativeness |

3.430 |

0.626 |

Moderately high |

Locus of control |

3.655 |

0.561 |

Moderately high |

Need for Achievement |

4.064 |

0.560 |

Moderately high |

General self-efficacy |

3.934 |

0.636 |

Moderately high |

Tolerance of ambiguity |

3.509 |

0.545 |

Moderately high |

Notes: 1.00-1.79 = low;

1.80-2.59 = moderately low; 2.60-3.39 = average; 3.40-4.19 = moderately high;

4.20-5.00 = high.

Source: Own elaboration.

Mediation Analysis using Innovativeness as a Mediator between Financial Literacy and Risk-Taking Propensity among Aspiring Young Filipino Entrepreneurs

Table 3 displays correlation statistics among the variables under consideration. Students with good financial literacy tend to have higher risk-taking propensity, which means they are more likely to invest more money in riskier ventures when compared to those who have poor financial literacy. Similarly, studies indicate that financial literacy has a positive association with innovativeness, thus suggesting that those with high financial literacy may also show innovative behaviors. Additionally, gender demonstrates a moderate positive correlation with risk-aversion tendency, indicating that men are more prone to risk-taking than women, as supported by the moderated positive correlation. However, the interconnections between other variables such as gender, monthly family income, owning a family business, and so on are not correlated, and these may have no clear relationship between them and financial literacy or entrepreneurial characteristics.

Table 3. Correlation statistics of the variables

Variables |

1 |

2 |

3 |

4 |

5 |

6 |

Financial literacy |

||||||

Risk-taking propensity |

0.415*** |

- |

||||

Innovativeness |

0.268*** |

0.561*** |

- |

|||

Gender |

0.028ns |

0.158** |

0.075ns |

- |

||

Monthly family income |

0.046ns |

-0.020ns |

0.019 ns |

-0.003ns |

- |

|

Owning a family business |

0.061ns |

-0.021ns |

-0.075ns |

0.021ns |

0.195* |

- |

* p < 0.05; ** p < 0.01; *** p < 0.001 ns:

not significant.

Source: Own elaboration.

Table 4 presents mediation estimates analyzing the influence of perceived innovativeness on the relationship between financial literacy and risk-taking propensity. The table indicates a significant direct effect of financial literacy toward risk-taking propensity (z-value = 4.416; p < 0.001). On the other hand, the indirect impact also shows a significant influence of financial literacy on risk-taking propensity mediated by perceived innovativeness (z-value = 3.157; p < 0.001), which indicates a statistically substantial positive mediation effect. The result of the study shows that the literature review confirms financial literacy as the fundamental component of risk propensity among young entrepreneurs (z-value = 5.720; p < 0.001). Moreover, the mediation analysis shows that the direct relationship between financial literacy and risk inclination is 68.9 %, while the relationship mediated by perceived innovativeness is only 31.1 %. Therefore, financial literacy has a direct association with risk-taking propensity while, at the same time, individuals' perceptions of their own innovativeness play an indirect role.

Table 4. Mediation estimates caused by perceived innovativeness on the financial literacy and risk-taking propensity relationship

Effects |

B |

SE |

z-value |

p-value |

% |

Direct |

0.362 |

0.082 |

4.416 |

<0.001 |

68.9 |

Indirect |

0.164 |

0.052 |

3.157 |

<0.001 |

31.1 |

Total |

0.526 |

0.092 |

5.720 |

<0.001 |

100.0 |

Source: Own elaboration.

The path estimates presented in Table 5 indicate that innovativeness serves as the mediating variable between financial literacy and risk-taking propensity. The process of innovativeness leading to risk-taking propensity demonstrates that innovativeness positively predicts risk-taking propensity. Thus, individuals who are digitized and perceive themselves as more innovative are more likely to exhibit higher levels of risk-taking propensity. Finally, the effect of financial literacy on risk-taking propensity points out an impressive positive correlation between financial literacy and risk-taking propensity, indicating that people with high financial awareness show a higher inclination to take risks. In addition, the pathway from financial literacy to innovativeness confirms that financial literacy is a positive predictor of innovativeness, which means that those with greater financial knowledge are more likely to perceive themselves as innovative.

Table 5. Path estimates using innovativeness as mediating variable

Paths |

B |

SE |

z-value |

p-value |

|

Innovativeness |

- Risk-taking propensity |

0.465 |

0.062 |

7.484 |

<0.001 |

Financial literacy |

- Risk-taking propensity |

0.362 |

0.082 |

4.416 |

<0.001 |

Financial literacy |

- Innovativeness |

0.353 |

0.101 |

3.482 |

<0.001 |

Source: Own elaboration.

Table 6 presents the results of the hypothesis testing conducted as part of the research. Firstly, the hypothesis regarding the relationship between financial literacy and innovativeness is supported, suggesting that respondents with higher financial literacy tend to be more innovative than those with lower financial literacy levels. Moreover, the study's hypothesis is further supported by the finding that individuals with higher financial literacy show greater risk-taking propensity than aspiring entrepreneurs with lower financial literacy scores. The hypothesis regarding the mediating effect of innovativeness on the relationship between financial literacy and risk-taking readiness has also been supported. Finally, the results also indicate that innovativeness serves as a predictor variable. Therefore, individuals who perceive themselves as innovative are more likely to exhibit risk-taking behavior. The empirical results of the hypothesis testing confirm that all three elements positively influence financial literacy, innovativeness, and risk-taking propensity.

Table 6. Hypothesis testing results

Hypothesis |

Results |

||

Financial literacy |

- Innovativeness |

Supported |

|

Financial literacy |

- Risk-taking propensity |

Supported |

|

Financial literacy |

- Innovativeness |

- Risk-taking propensity |

Supported |

Innovativeness |

- Risk-taking propensity |

Supported |

|

Source: Own elaboration.

Discussion and implications

Drawing from the implications of this empirical research, the researcher determines key areas that play an important part in this attempt to build an integrated picture of the interaction among financial literacy, risk-taking inclination, and innovativeness of prospective young entrepreneurs.

First, financial literacy enhances innovativeness by providing the skills and knowledge necessary to make sound financial decisions, mitigate risks, and conserve resources. Knowledge of financial principles enables individuals to confidently pursue challenges and make proactive decisions in transforming environments (Alshebami & Al Marri, 2022). This financial literacy fosters engagement in new enterprises, testing new concepts, and adjustment to new market patterns (Duréndez et al., 2023). Facilitating individuals to assess risks and possible outcomes more accurately reduces fear of failure, allowing them to take calculated risks and pursue entrepreneurial opportunities (Shahzad et al., 2021).

Financial literacy also develops a mindset conducive to opportunity, strategic planning, and thinking for the long term—three key drivers of innovation (Hamdan, 2023). With enhanced financial literacy, individuals are better equipped to anticipate trends before they emerge and capitalize on them to drive growth and sustainability. The informed and visionary approach enables them to pursue creative solutions, foster business growth, and contribute to economic growth (Khursanaliyev & Solidjonov, 2024). Financial literacy is the foundation for innovative thinking that stimulates individuals and businesses to thrive in a constantly evolving economy, instilling optimism and faith in the future (Kumar et al., 2023).

Second, a solid understanding of financial principles and the ability to accurately evaluate risks and rewards, can increase one's willingness to take risks. With this knowledge, individuals can more confidently pursue investment opportunities, entrepreneurial ventures, and other financial decisions, thereby reducing the uncertainty and anxiety that often hinder risk-taking (Ahmad et al., 2024). Those trained in finances can take risks more confidently (Molina-García et al., 2023). They can estimate the advantages, bear losses, and diversify investment to anticipate and avoid potential deficiencies (Adewumi, 2022).

Financial literacy also enables a cautious approach to risk-taking by empowering individuals to make informed decisions about their financial future. Financially literate people understand the importance of dealing with present risks and future benefits (Lusardi & Messy, 2023). In assuming a well-organized risk, they can identify it as appropriate and affirmative (Hermansson & Jonsson, 2021). Such awareness fosters a positive attitude toward risk-taking, enabling individuals to seize new opportunities and contribute to progress and economic development.

Third, innovators serve as the pillars of opportunity recognition, indirectly exerting a positive influence on risk-taking propensity. They foster open-mindedness toward new ideas, experimentation, and unconventional solutions. Innovative individuals naturally venture into uncharted territory and take calculated risks (Williams et al., 2021; Torres-Coronas & Vidal-Blasco, 2019). Their proactive problem-solving attitude enables them to transform potential threats into opportunities, making their willingness to work in uncertain situations a core characteristic of their pursuit of breakthroughs and advancement of their goals (Murnieks et al., 2020).

Also, innovation may accompany experimentation, and failure is treated as a learning opportunity and not a hurdle (Rhaiem & Amara, 2021). Such a mindset promotes taking risks because innovators realize that even failed results can yield insightful information for the next attempt (Giaccone & Magnusson, 2022). Driven by potential benefits, including new and competitive markets, innovative stakeholders are expected to embrace risks and bring forth profound transformation and influence (Suhada et al., 2021). This desire creates a risk-taking culture that sustains innovation and growth.

Meanwhile, innovativeness mediates risk-taking tendency and financial literacy, bridging the gap between knowledge and action. Financial literacy enables individuals to make judgments regarding available risks and incentives, and creativity enables them to use that information to assume calculated risks (Duréndez et al., 2023; Torres-Coronas & Vidal-Blasco, 2019). People with a good grasp of finances can find opportunities in volatile situations. Their creativity compels them to use their knowledge to try new things, experiment with new ideas, discover various strategies, and venture into possibilities that can result in valuable returns, giving them an optimistic and hopeful attitude (Giaccone & Magnusson, 2022).

Innovativeness enhances the effect of financial literacy on risk willingness by encouraging innovative thinking (Al-Mamary & Alshallaqi, 2022). Financially literate individuals with innovation will likely see economic risks as opportunities for growth and not threats (Klapper & Lusardi, 2020). Innovativeness motivates them to be innovative thinkers, considering all circumstances with an objective and in-depth mindset, take bold steps toward their goals, and balance potential profits against calculated risks.

Finally, innovativeness encourages the active application of economic knowledge, thus promoting a bolder risk-taking attitude (Duréndez et al., 2023). Although financial literacy may inspire prudence and innovativeness, it inspires creative risk-taking through pursuing new avenues and unconventional strategies. Such creative application of financial knowledge expands the impact of financial literacy on risk-taking orientation, promoting more deliberate and assertive decision-making that leads to development and innovation.

Conclusions

This study examined the mediating role of innovativeness in the relationship between financial literacy and risk-taking propensity among potential Filipino entrepreneurs. Results indicate a multifaceted relationship between these variables, referring to how these variables influence entrepreneurial behavior. Financial literacy is viewed as a key component in enabling creativity. Training individuals with the information and knowledge necessary to make sound financial decisions enables them to manage risks, optimize resource use, and develop an attitude that encourages opportunity recognition, strategic thinking, and long-term thinking. Financial literacy also positively impacts individuals' willingness to take risks. They generally assessed risk properly and made reasonable judgments, reducing their fear of being risk-averse and boosting their risk willingness.

Innovativeness played a mediating role that bridged financial literacy and risk willingness. Encouraging creative thinking promotes seeing challenges as opportunities and learning from failures, developing risk-taking and entrepreneurial activities through novel ideas, experimentation, and thinking outside the box. This study adds to the literature by providing empirical evidence of the interconnectedness among risk-taking attitudes, financial literacy, and innovation among young Filipino entrepreneurs. The results strongly resonate with policymakers and educational institutions, suggesting that these qualities must be nurtured to achieve economic growth and entrepreneurship.

Although this research provides interesting evidence of the mediating effect of innovativeness on the financial literacy and risk tolerance of Filipino students, the cross-sectional nature of the study limits the ability to establish absolute cause-and-effect relationships. Second, restricting the sample to students from a single Philippine university constrains the external validity of the results. Longitudinal designs in later studies can be used to follow up with graduates after some years, producing more robust evidence of the effect of financial literacy, innovativeness, and risk tolerance in enabling them to be successful at self-employment to counteract these limitations. Comparative research with potential entrepreneurs in other nations may also reveal more widespread cultural or educational determinants of these variables.

References

Adewumi, S. (2022). Financial literacy and business risk-taking among business start-up students in Nigeria. Problems and Perspectives in Management, 20(2), 575-587. https://doi.org/10.21511/ppm.20(2).2022.47

Ahmad, Z., Sharif, S., Ahmad, I., Abbas, S. M. W., & Shaheen, M. (2024). Does female descendent entrepreneur's self-compassion and financial literacy matter for succession success? Journal of Family Business Management, 14(3), 437-461. https://doi.org/10.1108/JFBM-07-2023-0102

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179-211. https://doi.org/10.1016/0749-5978(91)90020-T

Al-Mamary, Y. H., & Alshallaqi, M. (2022). Impact of autonomy, innovativeness, risk-taking, proactiveness, and competitive aggressiveness on students' intention to start a new venture. Journal of Innovation & Knowledge, 7(4), 100239. https://doi.org/10.1016/]'.jik.2022.100239

Almeda, A., Balisi, L. M., Concepcion, R. A., Lofamia, J. C., Tapec, J. A., & Padayao, P. M. T. (2020). "Calculated risk-taking": The success factors of entrepreneurial accountants. New Trends in Qualitative Research, 1, 8-29. https://doi.org/10.36367/ntqr.1.2020.8-29

Alshebami, A. S., & Al Marri, S. H. (2022). The impact of financial literacy on entrepreneurial intention: The mediating role of saving behavior. Frontiers in Psychology, 13, 911605. https://doi.org/10.3389/fpsyg.2022.911605

Anwar, I., & Saleem, I. (2019). Exploring entrepreneurial characteristics among university students: An evidence from India. Asia Pacific Journal of Innovation and Entrepreneurship, 13(3), 282-295. https://doi.org/10.1108/APJIE-07-2018-0044

Becker, G. S. (1964). Human capital: A theoretical and empirical analysis, with special reference to education (Vol. 3). University of Chicago Press.

Burchi, A., Wlodarczyk, B., Szturo, M., & Martelli, D. (2021). The effects of financial literacy on sustainable entrepreneurship. Sustainability, 13(9), 5070. https://doi.org/10.3390/su13095070

Damoah, O. B. O. (2020). Strategic factors predicting the likelihood of youth entrepre-neurship in Ghana: A logistic regression analysis. World Journal of Entrepreneurship, Management and Sustainable Development, 16(4), 389-401. https://doi.org/10.1108/WJEMSD-06-2018-0057

Duréndez, A., Dieguez-Soto, J., & Madrid-Guijarro, A. (2023). The influence of CEO'S financial literacy on smes technological innovation: The mediating effects of MCS and risk-taking. Financial Innovation, 9(1), 15. https://doi.org/10.1186/s40854-022-00414-w

Fong, J. H., Koh, B. S., Mitchell, O. S., & Rohwedder, S. (2021). Financial literacy and financial decision-making at older ages. Pacific-Basin Finance Journal, 65, 101481. https://doi.org/10.1016/j.pacfin.2020.101481

García-Lopera, F., Santos-Jaén, J. M., Palacios-Manzano, M., & Ruiz-Palomo, D. (2022). Exploring the effect of professionalization, risk-taking and technological innovation on business performance. PloS ONE, 17(2), e0263694. https://doi.org/10.1371/journal.pone.0263694

Giaccone, S. C., & Magnusson, M. (2022). Unveiling the role of risk-taking in innovation: Antecedents and effects. R&D Management, 52(1), 93-107. https://doi.org/10.1111/radm.12477

Guliman, D. O. (2020). The role of entrepreneur's financial sophistication on the nexus of business strategy and sustainability indicators of Philippine microenterprises. Asia-Pacific Social Science Review, 20(3), 11. https://doi.org/10.59588/2350-8329.1321

Hamdan, S. (2023). The entrepreneurial mindset: How to think like an innovator: Entrepreneurial mindset. Partridge Publishing Singapore.

Hermansson, C., & Jonsson, S. (2021). The impact of financial literacy and financial interest on risk tolerance. Journal of Behavioral and Experimental Finance, 29, 100450. https://doi.org/10.1016/j.jbef.2020.100450

Khursanaliyev, B., & Solidjonov, D. (2024). Foresight, innovation strategies, and technological guideline for turning a small business into a corporation. In E3S Web of Conferences (Vol. 538, p. 02015). EDP Sciences. https://doi.org/10.1051/e3sconf/202453802015

Klapper, L., & Lusardi, A. (2020). Financial literacy and financial resilience: Evidence from around the world. Financial Management, 49(3), 589-614. https://doi.org/10.1111/fima.12283

Kulathunga, K. M. M. C. B., Ye, J., Sharma, S., & Weerathunga, P. R. (2020). How does technological and financial literacy influence SME performance: Mediating role of erm practices. Information, 11(6), Article 297. https://doi.org/10.3390/INFO11060297

Kumar, P., Pillai, R., Kumar, N., & Tabash, M. I. (2023). The interplay of skills, digital financial literacy, capability, and autonomy in financial decision making and well-being. Borsa Istanbul Review, 23(1), 169-183. https://doi.org/10.1016/j.bir.2022.09.012

Liu, B., Wang, J., Chan, K. C., & Fung, A. (2021). The impact of entrepreneurs' financial literacy on innovation within small and medium-sized enterprises. International Small Business Journal, 39(3), 228-246. https://doi.org/10.1177/0266242620959073

Llanos-Contreras, O., Alonso-Dos-Santos, M., & Ribeiro-Soriano, D. (2020). Entrepreneurship and risk-taking in a post-disaster scenario. International Entrepreneurship and Management Journal, 16, 221-237. https://doi.org/10.1007/s11365-019-00590-9

Lumpkin, G. T., & Dess, G. G. (1996). Clarifying the entrepreneurial orientation construct and linking it to performance. Academy of management Review, 21(1), 135-172. https://doi.org/10.5465/amr.1996.9602161568

Lusardi, A., & Messy, F. A. (2023). The importance of financial literacy and its impact on financial wellbeing. Journal of Financial Literacy and Wellbeing, 1(1), 1-11. https://doi.org/10.1017/flw.2023.8

Molina-García, A., Cisneros-Ruiz, A. J., López-Subires, M. D., & Diéguez-Soto, J. (2023). How does financial literacy influence undergraduates' risk-taking propensity? The International Journal of Management Education, 21(3), Article 100840. https://doi.org/10.1016/j.ij-me.2023.100840

Morales, R. P. (2023). Financial literacy of micro entrepreneurs in Daet, Camarines Norte. Iconic Research and Engineering Journals, 6(12), 114-141.

Murnieks, C. Y., Klotz, A. C., & Shepherd, D. A. (2020). Entrepreneurial motivation: A review of the literature and an agenda for future research. Journal of Organizational Behavior, 41(2), 115-143. https://doi.org/10.1002/job.2374

Ogbari, M. E. (2023). Exploring the influence of entrepreneurial abilities on graduates' risk-taking readiness. Journal of Entrepreneurial and Business Diversity, 1(1), 59-71. https://doi.org/10.38142/jebd.v1i1.56

Omoniyi, I. B., & Bongani, G. T. (2022). Entrepreneurship education's impact on South Africa's economic growth and development. Academy of Entrepreneurship Journal, 28, 1-9.

Quezon, M. S., & Vergara, S. I. O. (2022). Entrepreneurial competencies and business performance of millennial entrepreneurs. Res Militaris, 12(6), 967-984.

Ranalan, R. L., Sajetarios, J. M., Plaza, S. B. M., & Ochida, H. J. (2022). The financial literacy and entrepreneurial intention among young professionals. The Pendulum, 17(1), 204-231.

Razafimahasolo, M., Borromeo, R., Sausa, L., Carpizo, R., & Sabado, J. (2016). Impact of financial literacy on level of stress and academic achievement among college students. AUP Research Journal, 19(2), 22-36.

Rhaiem, K., & Amara, N. (2021). Learning from innovation failures: A systematic review of the literature and research agenda. Review of Managerial Science, 15, 189-234. https://doi.org/10.1007/s11846-019-00339-2

Shahzad, M. F., Khan, K. I., Saleem, S., & Rashid, T. (2021). What factors affect the entrepreneurial intention to start-ups? The role of entrepreneurial skills, propensity to take risks, and innovativeness in open business models. Journal of Open Innovation: Technology, Market, and Complexity, 7(3), 173. https://doi.org/10.3390/joitmc7030173

Song, Z., Mellon, G., & Shen, Z. (2020). Relationship between racial bias exposure, financial literacy, and entrepreneurial intention: An empirical investigation. Journal of Artificial Intelligence and Machine Learning in Management, 4(1), 42-55.

Suhada, T. A., Ford, J. A., Verreynne, M. L., & Indulska, M. (2021). Motivating individuals to contribute to firms' non-pecuniary open innovation goals. Technovation, 102, 102233. https://doi.org/10.1016/j.technovation.2021.102233

Tipu, S. A. A., & Fantazy, K. (2023). Linking knowledge development with sustainable supply chain performance: Mediating effects of innovativeness, proactiveness and risk taking. International Journal of Productivity and Performance Management, 72(2), 491-515. https://doi.org/10.1108/IJPPM-01-2021-0034

Torres-Coronas, T., & Vidal-Blasco, M.A. (2019). The importance of perceived behavioral control as a determining element of entrepreneurial intention among university students. Universidad & Empresa, 21(37), 108-135. https://doi.org/10.12804/revistas.urosario.edu.co/empresa/a.6522

Urbach, N., & Ahlemann, F. (2010). Structural equation modeling in information systems research using partial least squares. Journal of Information Technology Theory and Application, 11(2), 5-40.

Voda, A. I., Martinez, I., Tiganas, C. G., Maha, L. G., & Filipeanu, D. (2019). Examining the effects of creativity and willingness to take risk on young students' entrepreneurial intention. Transformations in Business & Economics, 18(2A), 469-489.

Wang, X., & Cheng, Z. (2020). Cross-sectional studies: Strengths, weaknesses, and recommendations. Chest, 158(1), S65-S71. https://doi.org/10.1016/jxhest.2020.03.012

Williams, A. M., Rodríguez Sánchez, I., & Skokic, V. (2021). Innovation, risk, and uncertainty: A study of tourism entrepreneurs. Journal of Travel Research, 60(2), 293-311. https://doi.org/10.1177/0047287519896012

Ye, J., & Kulathunga, K. M. M. C. B. (2019). How does financial literacy promote sustainability in SMES? A developing country perspective. Sustainability, 11(10), 2990. https://doi.org/10.3390/su11102990

![]()