10.12804/revistas.urosario.edu.co/empresa/a.14259

ARTÍCULO DE INVESTIGACIÓN CIENTÍFICA Y TECNOLÓGICA

Jesús Enrique Molina-Muñoz 1

Juliana Dussan 2

Paula Pérez-González3

1 Business School, Tecnológico de Monterrey (México).

0000-0002-6578-7516

0000-0002-6578-7516

jesus.molina@tec.mx

jesus.molina@tec.mx

2 School of Management, Universidad del Rosario (Bogotá, Colombia).

0009-0004-1829-8340

juliana.dussan@urosario.edu.co

3 School of Management, Universidad del Rosario (Bogotá, Colombia).

0009-0003-7570-3608

paulaval.perez@urosario.edu.co

Reception date: February 2, 2025

Acceptance date: October 6, 2025

To cite this article: Molina Muñoz, J. E., Dussan, J., & Pérez González, P. (2026). Volatility forecasting and oil shocks in emerging markets using mixed-frequency models: A review. Universidad y Empresa, 28(50), 1-24. https://doi.org/10.12804/revistas.urosario.edu.co/empresa/a.14259

Abstract

Forecasting volatility in emerging markets is challenging due to their unique

characteristics, including data quality issues, structural instability, and

complex nonlinear relationships. The GARCH-MIDAS model has emerged as a promising alternative, combining the strengths of GARCH to incorporate

mixed-frequency data, critical for modeling financial phenomena. While this

approach is used to study volatility, the study of oil prices and oil shocks as

drivers of volatility in emerging markets is particularly appealing given these

economies' vulnerability to such shocks, their dependence on oil revenue, and

global economic disruptions.

Objective: to explore and analyze the literature on the use of GARCH-MIDAS in emerging markets.

Methodology: a systematic literature review combined with a bibliometric analysis under the PRISMA framework to ensure clarity, transparency, and reproducibility.

Key findings: Results suggest oil shocks have positive and significant effects on

stock market volatility and are relevant for emerging markets.

Conclusion: GARCH-MIDAS is a promising tool for forecasting volatility, and the study of oil crises is an important area for future research.

Keywords: volatility forecasting; emerging markets; GARCH-MIDAS; oil shock.

Resumen

Pronosticar

la volatilidad en los mercados emergentes es un desafío por problemas de

calidad de los datos, inestabilidad estructural y relaciones no lineales

complejas. El modelo GARCH-MIDAS ha

surgido como una alternativa prometedora, que combina las fortalezas del GARCH para incorporar datos de

frecuencia mixta, cruciales para modelar fenómenos financieros. Si bien este

enfoque se utiliza para estudiar la volatilidad, el estudio de los precios del

petróleo y los shocks petroleros como impulsores de los efectos de la volatilidad en los

mercados emergentes, resulta atractivo dada la vulnerabilidad de estas

economías a los shocks petroleros, su dependencia de los ingresos petroleros y las

alteraciones económicas globales.

Objetivo: explorar y analizar la bibliografía sobre el uso del GARCH-MIDAS en los mercados emergentes.

Metodología: consistió en una revisión sistemática combinada con un análisis

bibliométrico bajo el marco PRISMA para

garantizar la claridad, la transparencia y la reproducibilidad.

Resultados principales: sugieren que los shocks petroleros tienen efectos positivos y significativos en la volatilidad bursátil y son pertinentes para los mercados emergentes.

Conclusión: GARCH-MIDAS es una herramienta

prometedora para pronosticar la volatilidad y que el estudio de las crisis

petroleras constituye un área importante para futuras investigaciones.

Palabras clave: pronóstico de volatilidad; mercados emergentes; GARCH-MIDAS; shock petrolero.

Resumo

Prever

a volatilidade nos mercados emergentes é desafiador por a qualidade dos dados, instabilidade estrutural e relações não lineares complexas. O modelo GARCH-MIDAS surgiu como alternativa promissora, combinando os pontos fortes do GARCH com dados de frequência mista, essenciais para modelar fenómenos financeiros. Embora essa abordagem seja utilizada para estudar a

volatilidade, o estudo dos preços do petróleo e dos choques petrolíferos como

impulsionadores dos efeitos da volatilidade nos mercados emergentes é

relevante, dada a vulnerabilidade dessas economias a tais choques, sua

dependência da receita do petróleo e as perturbações económicas globais.

Objetivo: explorar e analisar a literatura sobre o uso do GARCH-MIDAS nos mercados emergentes.

Metodologia: consistiu numa revisão sistemática da literatura, combinada com uma análise bibliométrica, realizada segundo o PRISMA, para garantir clareza, transparência e reprodutibilidade.

Principais resultados: sugerem que os choques do petróleo têm efeitos positivos e

significativos sobre a volatilidade do mercado de ações e são relevantes para os mercados emergentes.

Conclusão: GARCH-MIDAS é uma ferramenta promissora para prever a volatilidade e que o estudo das crises do petróleo constitui uma área importante

para pesquisas futuras.

Palavras-chave: previsão de volatilidade; mercados emergentes; GARCH-MIDAS; choque petrolífero.

Introduction

Volatility, defined as the variability of financial asset prices, plays a central role in investment decisions, risk management, and macro-financial stability. Consequently, a wide spectrum of methodologies has been developed to study the transmission of shocks—particularly those related to oil markets—into macroeconomic and financial variables. Early contributions relied on structural models such as Dynamic Stochastic General Equilibrium (DSGE) frameworks for small open economies, where oil prices enter production functions and utility specifications (Kilian, 2009; Baumeister & Peersman, 2013). Semi-structural approaches—such as Structural Vector Autoregressions (SVARS)—have been widely used to disentangle supply-driven and demand-driven oil shocks and to quantify their macroeconomic effects (Hamilton, 1983; Kilian & Murphy, 2014).

Econometric models of volatility, such as GARCH-type models, have been particularly influential because they provide a coherent representation of the stylized facts of financial and commodity returns, including volatility clustering, excess kurtosis, and nonlinear dynamics (Engle, 1982; Bollerslev, 1986; Andersen et al., 2003). These properties make them well-suited for capturing the dynamics of financial markets and for forecasting risk. Extensions such as GARCH-MIDAS allow researchers to link high-frequency volatility with low-frequency macroeconomic drivers, thereby enhancing their ability to integrate market and macroeconomic information (Engle et al., 2013).

In recent years, there has been a growing interest in studying 'oil crises' and their impact on financial markets. These events have caused significant increases in oil prices, which can have important global impacts on economic and financial variables such as inflation, recession, and unemployment (Bernanke, 1983). Emerging financial markets are particularly vulnerable to oil crises considering that many of these economies are oil exporters or heavily reliant on oil revenues (Hong et al., 2023). Thus, fluctuations in oil prices can directly impact their export revenues and economic stability.

While a substantial body of research has explored the macroeconomic and financial impacts of oil shocks in both advanced and emerging economies—using approaches such as DSGE models (Dissou, 2010; Hollander et al., 2019), structural vars (Kilian, 2009), and semi-structural models—there is still room for further investigation focusing on volatility dynamics. In particular, the application of GARCH-MIDAS models to the context of emerging economies is still limited, despite their ability to integrate mixed-frequency macroeconomic and financial data. This paper seeks to contribute by reviewing the literature related to the analysis of volatility in emerging markets under oil shocks through this framework, thereby complementing the existing literature.

The remainder of this paper is organized as follows. In Section 2, the employed methodology is presented. In Section 3, the empirical results and discussion are developed. Finally, Section 4 provides the conclusions and the further research directions emanating from this study.

Methodology

This exercise was developed through two stages which include a systematic literature review and a bibliometric analysis. To enhance transparency and reproducibility, the review followed the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) guidelines.

Information Sources and Search Strategy

In the first stage, the data were retrieved from the Web of Science database using the search queries shown in Table 1. Once the search was performed, 120 documents were obtained.

Table 1. Search queries

Search queries |

"GARCH MIDAS" + "VOLATILITY" "GARCH MIDAS" + "VOLATILITY FORECASTING" "GARCH MIDAS" + "ENERGY" "GARCH MIDAS" + "EMERGING MARKETS" |

Font: Own elaboration.

Eligibility Criteria

To ensure quality, the database was filtered as suggested by Ferrari (2015) to include exclusively:

• Articles written in English.

• Publications indexed in Q1 and Q2 of the Social Sciences Citation Index (SSCI) collection.

• Studies published between 2000 and 2024.

• Empirical or theoretical papers focused on volatility forecasting, GARCH-MIDAS models, and/or oil shocks in emerging markets.

Articles were excluded if they met the following conditions:

• Duplicated records.

• Not accessible in full text.

• Out of scope (e.g., studies focused exclusively on developed markets, or unrelated to volatility forecasting and GARCH-MIDAS).

• Non-academic or non-peer-reviewed works.

Selection Process

Subsequently, the remaining articles were reviewed manually to discard those unrelated to the topic examined. After this process, 30 articles were obtained and considered eligible. Each study was screened in two steps:

1. Title and abstract screening to ensure thematic relevance.

2. Full-text review to validate compliance with inclusion criteria.

From the retrieved articles, a narrative literature review was conducted. The reviewed manuscripts were summarized and categorized to identify specific patterns in previous research. Based on the above, a classification of the analyzed manuscripts was proposed, which is detailed in the results section.

Bibliometric and Conceptual Analysis

In the second stage, a bibliometric analysis was conducted on the database of selected documents. Therefore, the number of publications per year, citations trends, the number of articles and countries by author, and the collaboration networks among authors' countries were identified and analyzed.

In addition, a conceptual structure analysis of the topic studied was conducted using machine learning techniques, particularly the k-means clustering algorithm. This method is commonly used to "address the machine learning task of clustering, which involves finding natural groupings of data" (Lantz, 2019, p. 271). The main advantage of this approach is that it does not require a specific result associated with the data, which allows groups to be determined from the data without any preconceived criteria:

The k-means algorithm involves assigning each of the n examples to one of the k clusters, where k is a number that has been defined ahead of time. The goal is to minimize the differences within each cluster and maximize the differences between clusters. (Lantz, 2019, p. 272)

In our analysis, the k-means exercise was based on the co-currencies of words found in the abstracts, titles, and keywords of the articles included in the database. To accomplish this task, a natural language processing routine was applied to form the conceptual clusters. The results obtained from this step are presented in the following section.

Risk of Bias and Limitations

Although the PRISMA framework was applied, it is important to acknowledge some limitations. First, the exclusive use of the Web of Science database may have left out relevant studies indexed in other sources. However, this decision allowed us to focus on high-impact, peer-reviewed journals in economics and finance, which strengthens the reliability of the results. Second, the restriction to articles in English may introduce a language bias. However, it also ensured consistency in the analysis and comparability between studies. Finally, although manual review is not completely free of subjectivity, this process allowed for a more careful assessment of the relevance and quality of the included studies. Overall, these considerations do not weaken the study, but rather reinforce the robustness and credibility of the results.

Results

Literature Review

Following the previously described methodology, the selected articles were analyzed to gain insights into the literature related to the topic studied. This exercise is presented in two sections related to the (i) evolution of econometric models and (ii) the relationship between oil shocks and volatility in emerging markets.

Econometric Models

Recognizing the pivotal role of modeling and forecasting volatility, researchers and financial practitioners stress its importance in designing effective hedging and investment strategies. Regulatory bodies also heavily depend on accurate volatility forecasts to monitor turbulence in financial markets (Salisu et al., 2022). To address the challenges posed by volatile market conditions, researchers have diligently proposed methodologies for understanding and forecasting volatility. Among these approaches, the Autoregressive Conditional Heteroskedastic (ARCH) and Generalized Autoregressive Conditional Heteroskedastic (GARCH) models stand out.

The arch model, introduced by Robert Engle in 1982, aims to model volatility during both turbulent and calm periods. It forecasts future changes in variance over time based on past errors, providing valuable insights into macroeconomic and financial phenomena (Engle, 1982; Bollerslev et al., 1994). However, challenges arise due to a non-negativity restriction in the conditional variance formula (Bollerslev, 2023). Building on the arch model, Bollerslev (1986) developed the Generalized Autoregressive Conditional Heteroskedastic (GARCH) model, introducing a more flexible lag point and incorporating features from the arch model and regression analysis. Despite its advantages, the classic GARCH model faces limitations in estimating many coefficients and capturing asymmetric patterns in the second conditional moments, which affect the accuracy of the results (Cappiello et al., 2006).

In response to these limitations, the GARCH-MIDAS model (Engle et al., 2013) emerges as an advanced and less error-prone alternative for volatility modeling and forecasting. By combining GARCH models with Mixed Data Sampling (MIDAS) approaches, this model allows the incorporation of time series data with different frequencies, proving valuable for modeling economic, financial, and environmental phenomena.

While GARCH-MIDAS models have found success in analyzing variables like interest rates, exchange rates, and asset price volatility in developed countries, their application in emerging markets remains relatively unexplored. The unique challenges faced by emerging markets, including data quality issues, structural instability, and nonlinear relationships among variables, require specialized attention (Alper et al., 2012a, 2012b; X. Yu et al., 2021; Salisu et al., 2022; Wang & Li, 2023; Hong et al., 2023).

Latin American Emerging Markets: A Research Gap Worth Exploring

The GARCH-MIDAS model has been researched and used because it has become a widely accepted tool for forecasting volatility in financial markets, especially in developed economies and in certain emerging markets such as China and the BRICS nations. However, its application in Latin American contexts remains significantly underexplored, despite the region's marked exposure to oil price shocks and macroeconomic uncertainty (X. Yu et al. 2021). In the literature, there is a notable and scarcely addressed gap between developed and emerging countries, particularly visible in Latin America. This difference is explained by the structural dependence on commodity exports, fiscal sensitivity to oil revenues and a marked vulnerability to shocks in international crude oil prices. Economies such as Colombia, Mexico, and Brazil show volatility patterns that differ significantly from those observed in the BRICS countries or in Asian markets, due to factors specific to the region such as political instability, exchange rate fragility, and the asymmetric transmission of global energy shocks (Ratti & Vespignani, 2016).

Although classified as emerging economies, Latin American nations have been systematically underrepresented in empirical applications of mixed-frequency models such as GARCH-MIDAS. This methodological exclusion limits the generalizability of the findings from other regions and restricts the understanding of volatility dynamics within the Latin American context. Several studies have highlighted that incorporating economic, political, and environmental uncertainty variables into forecasting models can significantly improve their accuracy and relevance (Hong et al., 2023; Salisu & Gupta, 2021a, 2021b, 2021c). Consequently, broadening the empirical scope to include Latin America would not only close a gap in the literature, but also strengthen the design of financial policies adapted to the structural characteristics of the region. Likewise, the integration of macroeconomic uncertainty variables such as political risk, climate shocks, and institutional fragility in the volatility forecast remains underdeveloped in Latin American contexts. Expanding the empirical scope to include these dimensions could enhance the explanatory power of GARCH-MIDAS models and support stronger financial decision-making across the region (Galindo & Nuguer, 2023; Blanchard & Galí, 2007; Ayres et al., 2025).

In response to this identified gap, this review underscores the need for future research to systematically apply mixed-frequency models to Latin American financial markets, not only to fill a methodological gap, but also to inform public policy in economies where volatility has direct social and fiscal consequences.

Oil Shocks

Oil shocks are unexpected events in which the oil price experiences strong growth. This event can be caused by factors such as speculation and uncertainty in the financial market, problems with oil production and demand, armed conflicts, political disagreements, among others (Tumala et al., 2023). Consequently, they have a major impact on the global economy, as this raw material accounts for about 2.5% of the world's gross domestic product (GDP). Oil shocks, therefore, generate fluctuations in economic activity and cause significant disruptions in production systems—such as energy and transportation—as well as in macroeconomic variables, including excessive increases in inflation (World Bank, 2023). Therefore, the investigation of these sharp increases in oil prices has had a significant impact on financial markets.

Now, considering that volatility allows to understand in advance the movement of individual stocks and the stock market (Baum et al., 2010; Bloom, 2009), volatility forecasting has been tested in markets where oil shocks occur, as well as developed countries or some emerging countries such as the BRICS, i.e. Brazil, Russia, India, China and South Africa (Salisu et al., 2022; Salisu & Gupta, 2021a, 2021b).

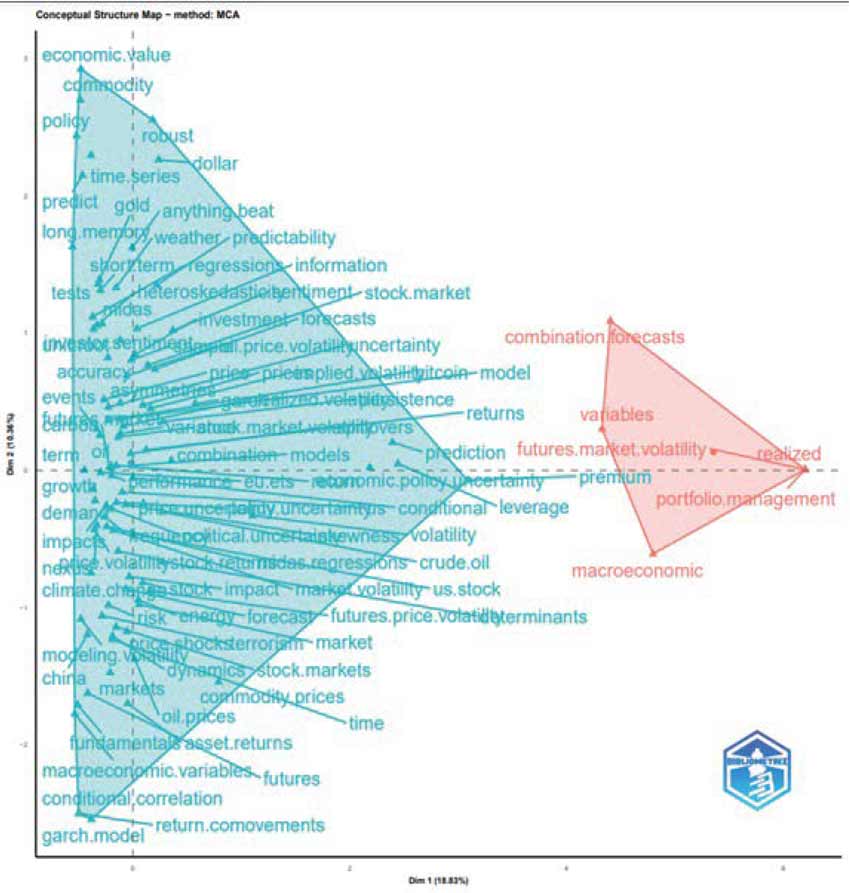

When analyzing the conceptual structure of the reviewed manuscripts, two clusters were identified (Figure 1). The blue cluster, which groups most of the analyzed documents, refers to concepts such as stock markets, prediction, volatility, exchange rates, energy assets and references to econometric models which include words such as midas and GARCH suggesting that this cluster exposes volatility forecasting as its main focus. The second cluster, identified by the red color, is related to other financial applications different from volatility forecasting including concepts such as variables, portfolio management, macro-economic, among others. In consequence, this cluster is classified as "other applications". This result is expected, considering that the main application of the GARCH-MIDAS model is related to volatility forecasting. However, it is worth noting that there are not specific countries within the clusters.

Figure 1. Conceptual Structure Map - Method: MOA

Font: Own elaboration.

Bibliometric Analysis

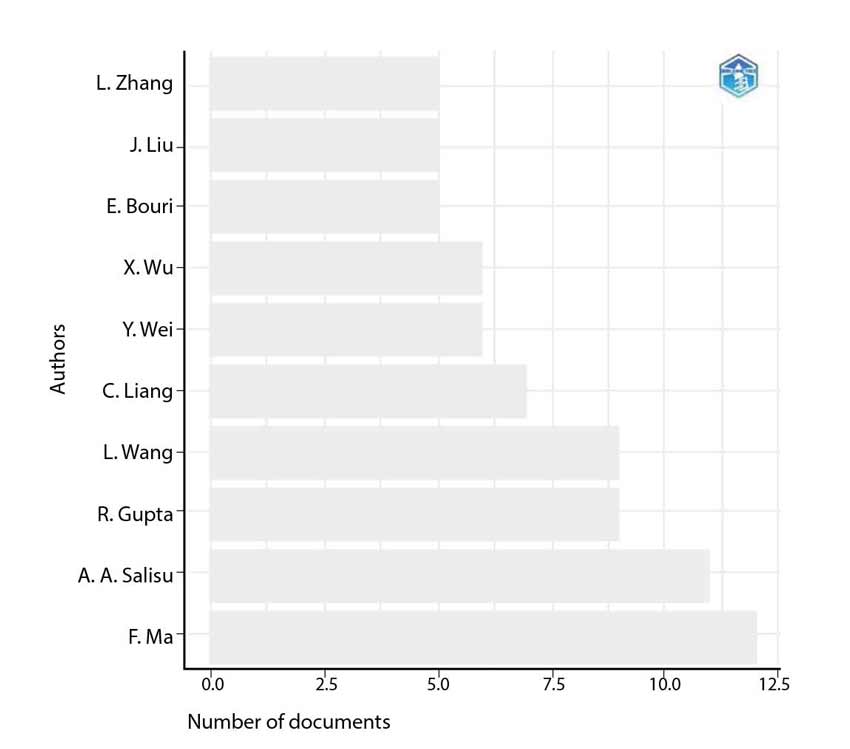

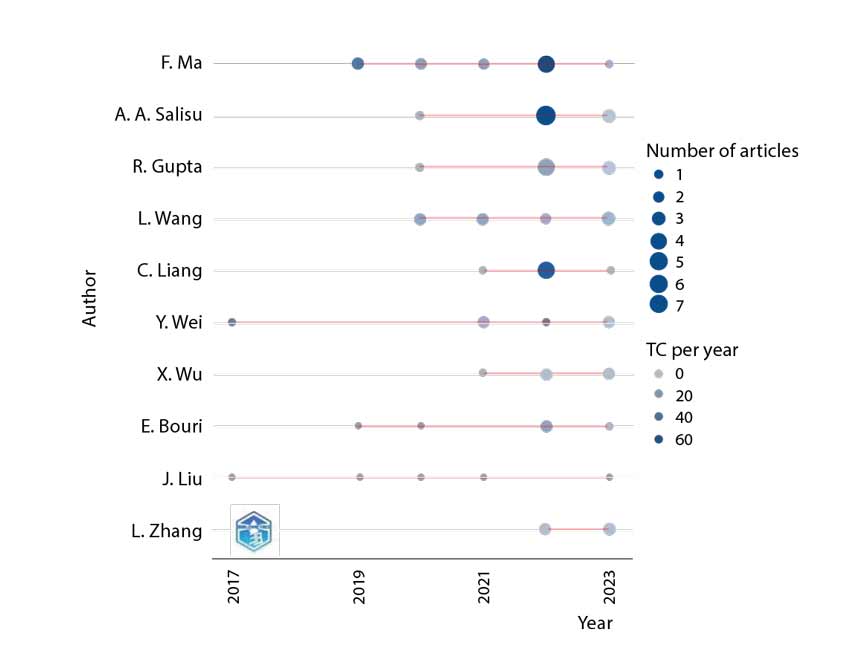

The bibliometric analysis was performed to gain insights into the trends and concentration of academic production, as well as the authors, collaborations, and countries related to the reviewed documents. Figure 2 shows the number of articles per author within the analyzed period. It can be observed that "F. Ma" is the most productive author, with a total of 12 articles published over a five-year period (2019-2023), placing him first in terms of productivity in this category. In second place, we find the author "A. A. Salisu" with 11 published articles, which demonstrates a high level of productivity. In third place, both authors "R. Gupta" and "L. Wang" are founded with 9 published articles. "C. Liang" has contributed a total of 7 published articles, making him the fourth most productive author on the list. On the other hand, authors "Y. Wei" and "X. Wu" share fifth place in terms of productivity, both with 6 articles published during the analyzed period.

Figure 2. Most Productive Authors

Font: Own elaboration.

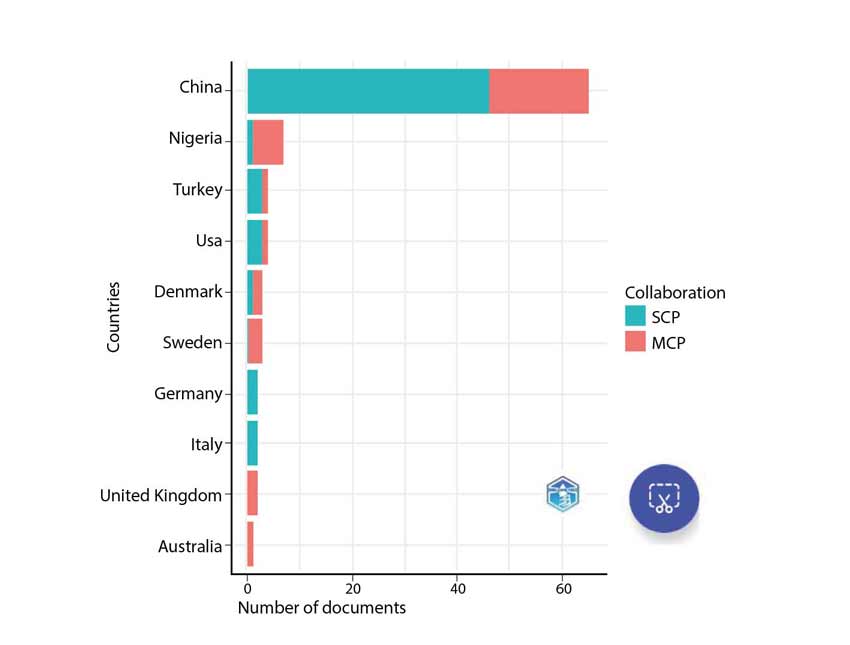

Production per country is shown in Figure 3, which provides an interesting view of the scientific production of articles in several countries. As can be observed, China leads academic production in terms of quantity, with 65 articles and a considerable proportion of them produced in collaboration with other countries. It is worth noting that the following country in terms of articles production is Nigeria, with only 7 articles, which are developed in collaboration with other countries in most of the cases. Turkey and the United States have similar results.

Figure 3. Most Productive Countries

SCP: Single Country Publications; MCP: Multiple

Font: Own elaboration.

While the number of articles produced is valuable information, so is the period in which the articles were produced (Figure 4). As can be seen, the most productive author has been C. Liang with 7 articles, one in 2021, five in the following year, and one in 2023. The second most productive is X. Wu, with 6 articles produced in the same number of years as the previous one. In third place is L. Zhang, with 5 articles.

Figure 4. Authors' Production over Time

Font: Own elaboration.

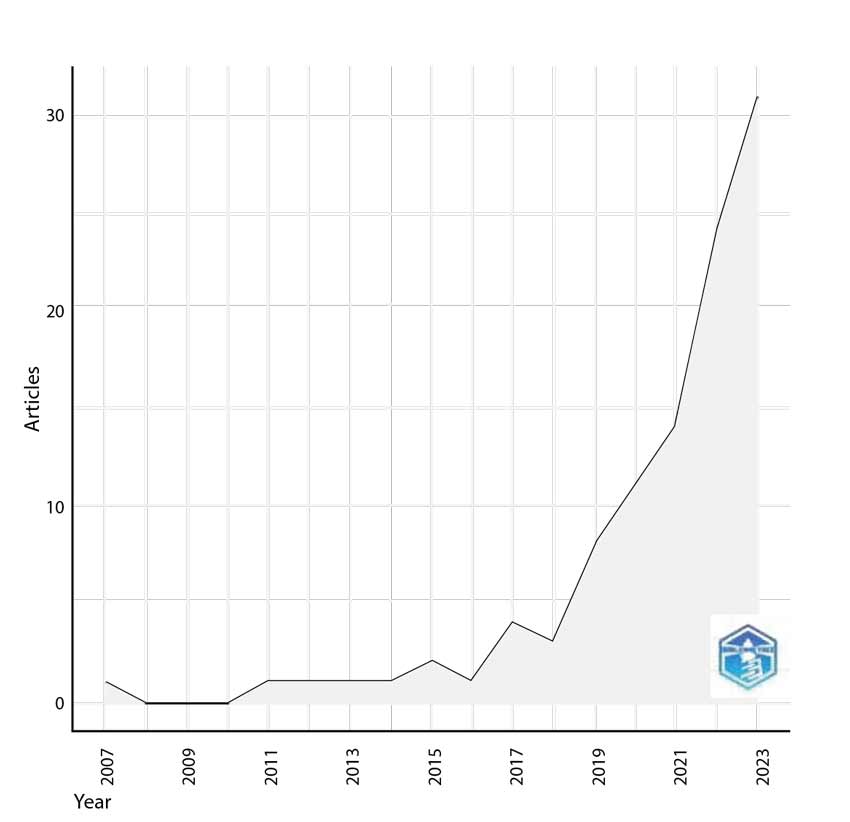

Regarding the annual scientific production, it can be observed in Figure 5 that it has evolved significantly over the years. From a modest beginning in 2007 with a single article, the number of publications remained at low levels until 2014. However, since 2015 there has been a marked and constant increase in scientific production. In 2023, 31 articles were reached, which reflects a substantial increase compared to previous years.

Figure 5. Annual Scientific Production

Font: Own elaboration.

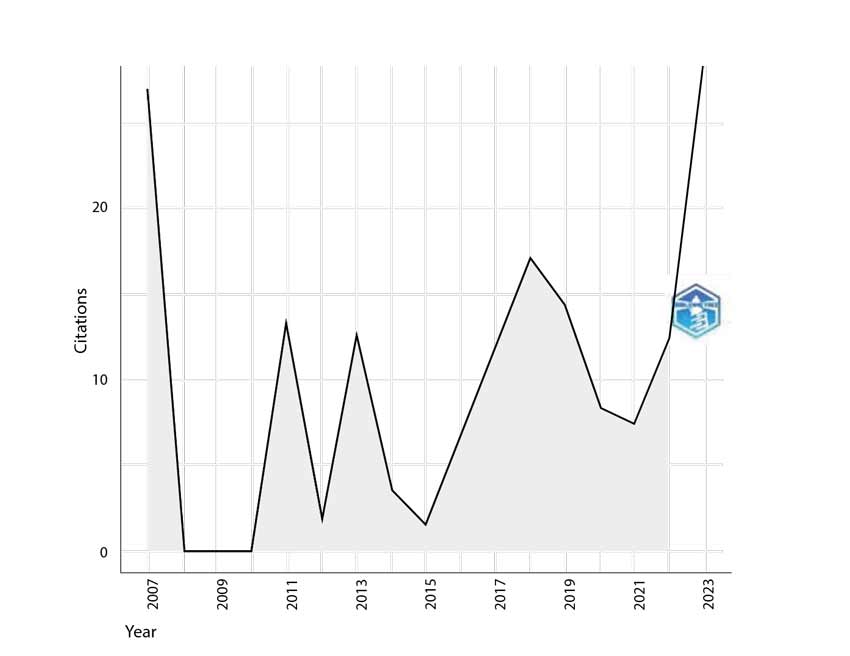

These results are in line with the average number of citations, which shows an exponential growth with recurrent fluctuations in the years where significant changes were made in the production of annual articles (Figure 6). This continued increase in scientific output suggests sustained interest in the topic and may be related to additional investments in research, technological advances, or a growing community of researchers. These data offer an encouraging view of academic activity and commitment to research in this specific area, with constant and promising growth in scientific production in recent years.

Figure 6. Average Article Citations per Year

Font: Own elaboration.

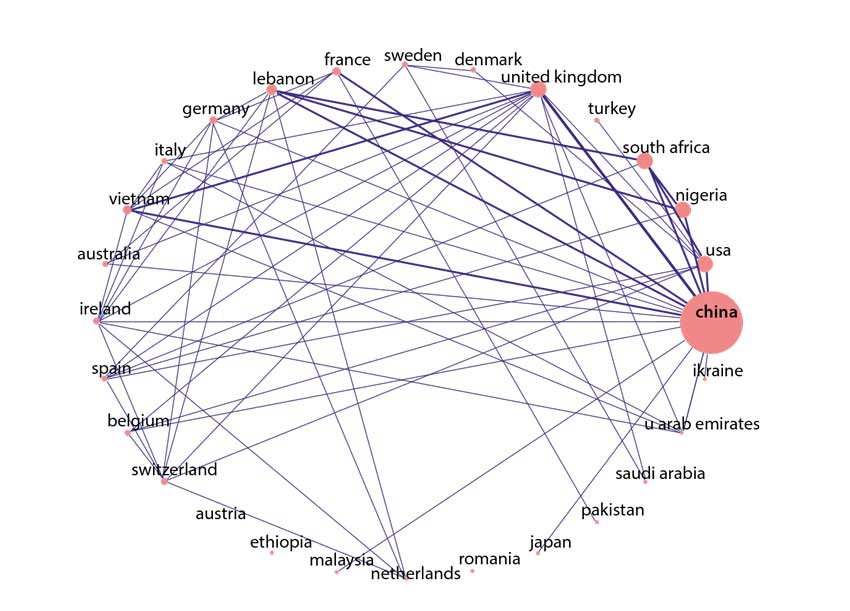

Collaboration between countries to produce articles has become more intense during the last few decades, as this relationship allows the development and research of articles to be more efficient and functional, enriching the knowledge of different cultures and opinions. In this regard, the literature review developed evidences a high level of collaboration between countries, as shown in Figure 7. In the obtained results, it is worth noting the high degree of cooperation between China and various regions, including France, Lebanon, the United Kingdom, United States, Nigeria, and South Africa and Asian countries.

Figure 7. Country Collaboration

Font: Own elaboration.

Discussion

The review of the impact of oil shocks on stock market volatility in emerging economies yields significant results, suggesting that these shocks have positive and significant effects on the volatility of these markets (Salisu & Gupta, 2021a, 2021b, 2021c; Ghani et al., 2023a, 2023b). The GARCH-MIDAS model is effective in capturing these effects by integrating mixed-frequency data, which allows to incorporate financial and economic variables based on different periodicities. This is crucial for emerging markets, characterized by structural instability and high sensitivity to external shocks, where the adequate understanding of volatility dynamics is of special interest.

However, it is worth mentioning that the analyzed model does not capture all the nuances, such as the asymmetric volatility responses in different markets. At the same time, other limitations have been identified in literature. First, the model relies heavily on the correct specification of low-frequency explanatory variables, which can lead to biases if relevant macroeconomic or financial indicators are omitted (Salisu et al., 2022; X. Yu et al., 2021). Second, its results are sensitive to data selection, as estimates can vary significantly depending on the dataset used and the construction of the MIDAS component. Finally, compared to more flexible frameworks, such as multivariate extensions of GARCH, GARCH-MIDAS may underestimate the dynamic interdependencies between markets (Engle, 2002, 2009; Cappiello et al., 2006; Salisu et al., 2022; Wang & Li, 2023).

Nevertheless, these limitations do not reduce the relevance of the model. On the contrary, they show the need to interpret its results with caution and to complement them with alternative approaches. Acknowledging these weaknesses contributes to enriching the debate, as it clarifies where improvements are needed and opens opportunities for future research. All in all, given the limitations of traditional GARCH models (Alper et al., 2012a, 2012b; Salisu et al., 2022), the usefulness of GARCH-MIDAS in emerging contexts is remarkable. In addition, combining this model with indicators of economic, political, and environmental uncertainty could improve the accuracy of volatility forecasts.

The results have important implications for policymakers and investors in emerging markets, suggesting that the GARCH-MIDAS model could be valuable for managing volatility and hedging against oil shocks and other financial variables. Policymakers could use this model to anticipate and mitigate the effects of oil shocks on the economy, while investors could use it to make informed decisions about their investment and hedging strategies in emerging markets.

Practical Applications of the Study

Building on the previous discussion, it is essential to highlight the theoretical value of the GARCH-MIDAS volatility forecasting model. Beyond its analytical depth, this approach can be translated into practical tools for a wide range of stakeholders in emerging markets, particularly in Latin American economies. Below are concrete examples, supported by empirical studies, that show how mixed-frequency models enhance real-world decision-making.

Investors

In Nigeria and South Africa, Tumala et al. (2023) applied a GARCH-MIDAS framework to separate oil shocks from idiosyncratic market movements. They showed that hedge funds that used these mixed-frequency volatility signals were able to anticipate days of extreme volatility and adjust their futures hedges accordingly, leading to a measurable reduction in the Value-at-Risk of their portfolios during the 2022 oil price rally.

Regulators

Hong et al. (2023a) demonstrated that integrating a financial uncertainty index into a GARCH-MIDAS model significantly improved early warning signals about systemic stress in China's A-share market. By incorporating daily volatility forecasts into its macroprudential dashboard, the People's Bank of China was able to preemptively adjust liquidity requirements, thereby mitigating near-term market turbulence.

Public Policymakers

Tumala et al. (2023) demonstrate how disentangled oil shocks can be used to assess stock market volatility in emerging economies such as Nigeria and South Africa. Using the GARCH-MIDAS framework, they integrate low-frequency macroeconomic indicators with high-frequency financial data to produce more accurate volatility forecasts. This approach offers valuable insights for designing countercyclical fiscal frameworks in oil-dependent economies, where volatility thresholds can guide sovereign stabilization fund transfers and improve debt service performance during periods of oil price stress.

Interdisciplinary Applications

Perilla (2023) expanded the GARCH-MIDAS approach by incorporating monthly series of co2 emissions along with daily oil prices to assess the links between climate and finance in Latin America. This hybrid model provided development agencies and central banks with prospective risk assessments on green energy investments under volatile oil markets.

These examples highlight the versatility of mixed-frequency volatility models. Whether calibrating dynamic hedges, strengthening macroprudential supervision, designing countercyclical policies, or assessing environmental-financial risks, GARCH-MIDAS offers a data-driven compass for navigating uncertainty in emerging economies.

Conclusions

This study provided a detailed literature review on the use of GARCH-MIDAS models to predict volatility in emerging markets focusing on the impact of oil shocks. A systematic literature search and a bibliometric analysis were carried out to highlight the relevance of econometric models in volatility prediction, underlining their importance for hedging and investment strategies.

The analysis addressed the limitations of traditional models such as arch and GARCH specifications, highlighting the relevance of the GARCH-MIDAS model due to its ability to integrate mixed frequency data. Nevertheless, some limitations of GARCH-MIDAS have also been noted in the literature, such as its sensitivity to data selection, its dependence on the correct specification of low-frequency variables, and its difficulties in capturing asymmetric effects or dynamic interdependencies across markets. These considerations highlight the need to interpret its results with caution and to complement it with alternative approaches. The scarcity of research on the application of GARCH-MIDAS models in emerging markets including some Asian, European, and most of the Latin American economies was highlighted, underlining the importance of studying the impact of oil shocks on the volatility of these markets.

In terms of scientific production, the most prolific authors were identified, and it was observed that China leads in academic output, showing a notable trend toward international cooperation and collaboration networks with several countries, mostly from Europe.

Our study suggests promising directions for further research, calling for more comprehensive studies in emerging Latin American, European, and Asian economies different from BRIC nations, especially focused on the impact of oil shocks but including other types of variables such as economic, climate, and political uncertainty. In addition, it is pertinent to explore additional applications and extensions of GARCH-MIDAS models (i.e. DCC MIDAS models) in different financial contexts, such as portfolio management and macroeconomic considerations. Continued collaboration between researchers from different countries could be of special interest for a deeper understanding of volatility in emerging markets. In addition, further research efforts could be oriented to adopt interdisciplinary approaches, incorporating economics, finance, and environmental sciences to gain a holistic perspective about volatility and financial stability in emerging economies.

Contributor Role Taxonomy (CRediT)

The three authors contributed equally to: conceptualization, methodology, investigation, data curation, formal analysis, project administration, visualization, writing - original draft, writing - review & editing.

References

Alper, A., Ercan, E., & Yilmaz, O. (2012). The impact of economic and financial uncertainty on stock market volatility in Turkey. Economic Modelling, 29(6), 2326-2336. https://doi.org/10.1016/j.econmod.2012.05.030

Alper, C. E., Kilinç, M., & Ozün, A. (2012). Estimating the impact of oil price shocks on stock market returns: Evidence from Turkey. Economic Systems, 36(2), 278-291. https://doi.org/10.1016/j.ecosys.2011.08.003

Andersen, T. G., Bollerslev, T., Diebold, F. X., & Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica, 71(2), 579-625. https://doi.org/10.1111/1468-0262.00418

Ayres, J., Izquierdo, A., & Parrado, E. (2025). 2025 Latin American and Caribbean macro-economic report: Regional opportunities amid global shifts. Inter-American Development Bank. https://doi.org/10.18235/0013475

Baumeister, C., & Peersman, G. (2013). Time-varying effects of oil supply shocks on the us economy. American Economic Journal: Macroeconomics, 5(4), 1-28. https://doi.org/10.1257/mac.5.4.1

Bernanke, B. S. (1983). Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics, 98(1), 85-106. https://doi.org/10.2307/1885568

Blanchard, O. J., & Galí, J. (2007). The macroeconomic effects of oil shocks: Why are the 2000s so different from the 1970s? [NBER Working Paper Series, 13368]. National Bureau of Economic Research. https://doi.org/10.3386/w13368

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31 (3), 307-327. https://doi.org/10.1016/0304-4076(86)90063-1

Bollerslev, T. (2023). Reprint of: Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 234, 25-37. https://doi.org/10.1016/j.jeconom.2023.02.001

Bollerslev, T., Engle, R. F., & Nelson, D. B. (1994). arch models. In R. F. Engle & D. L. McFadden (Eds.), Handbook of econometrics (vol. 4, pp. 2959-3038). Elsevier. https://doi.org/10.1016/S1573-4412(05)80018-2

Cappiello, L., Engle, R. F., & Sheppard, K. (2006). Asymmetric dynamics in the correlations of global equity and bond returns. Journal of Financial Econometrics, 4(4), 537-572. https://doi.org/10.1093/jjfinec/nbl005

Dissou, Y. (2010). Oil price shocks: Sectoral and dynamic adjustments in a small-open developed and oil-exporting economy. Energy Policy, 38(1), 562-572. https://doi.org/10.1016/j.enpol.2009.09.026

Engle, R. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3), 339-350. https://doi.org/10.1198/073500102288618487

Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4), 987-1007. https://doi.org/10.2307/1912773

Engle, R. F. (2009). GARCH models with time-varying volatility and correlations. Journal of Business & Economic Statistics, 27(4), 505-521. https://doi.org/10.1198/jbes.2009.07132

Engle, R. F., Ghysels, E., & Sohn, B. (2013). Stock market volatility and macroeconomic fundamentals. Review of Economics and Statistics, 95(3), 776-797. https://doi.org/10.1162/REST_a_00300

Galindo, A., & Nuguer, V. (2023). Fuel-price shocks and inflation in Latin America and the Caribbean. Inter-American Development Bank. https://doi.org/10.18235/0004724

Ghani, U., Zhu, B., Ghani, M., & Khan, N. (2023). Role of oil shocks in us stock market volatility: A new insight from GARCH-MIDAS MIDAS perspective. Resources Policy, 85, 103933. https://doi.org/10.1016/j.resourpol.2023.103933

Ghani, W., Rizvi, S. K. A., & Alam, M. (2023). Oil price shocks and stock market volatility: Evidence from emerging economies. Journal of International Financial Markets, Institutions and Money, 80, 102924. https://doi.org/10.1016/j.intfin.2022.102924

Hamilton, J. D. (1983). Oil and the macroeconomy since World War II. Journal of Political Economy, 91 (2), 228-248. https://doi.org/10.1086/261140

Hollander, H., Gupta, R., & Wohar, M. E. (2019). The impact of oil shocks in a small open economy New-Keynesian dynamic stochastic general equilibrium model for an oil-importing country: The case of South Africa. Emerging Markets Finance and Trade, 55(7), 1593-1618. https://doi.org/10.1080/1540496X.2018.1500893

Hong, D., Zhou, Y., & Zhang, X. (2023). The impact of financial market uncertainty on the volatility of stock prices in emerging markets. Emerging Markets Review. https://doi.org/10.1016/j.ememar.2023.100944

Hong, H., Li, F. W., & Xu, J. (2023). Economic policy uncertainty, oil price shocks, and stock market volatility: Evidence from global markets. Energy Economics, 118, 106512. https://doi.org/10.1016/j.eneco.2023.106512

Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review, 99(3), 1053-1069. https://doi.org/10.1257/aer.99.3.1053

Kilian, L., & Murphy, D. P. (2014). The role of inventories and speculative trading in the global market for crude oil. Journal of Applied Econometrics, 29(3), 454-478. https://doi.org/10.1002/jae.2322

Lantz, B. (2019). Machine learning with R: Expert techniques for predictive modeling (3rd ed.). Packt Publishing. https://doi.org/10.1080/10686967.2019.1648086

Obstfeld, M., Milesi-Ferretti, G. M., & Arezki, R. (2016). Oil prices and the global economy: It's complicated [IMF Working Paper 16/210]. International Monetary Fund. https://doi.org/10.5089/9781475552034.001

Pan, Z., Huang, X., Liu, L., & Huang, J. (2023). Geopolitical uncertainty and crude oil volatility: Evidence from oil-importing and oil-export. Finance Research Letters, 52. https://doi.org/10.1016/j.eneco.2022.105791

Perilla, J. S. (2023). Oil price shocks and macroeconomic volatility in Latin America: The role of structural dependence and policy frameworks. Resources Policy, 80, 103217. https://doi.org/10.1016/j.resourpol.2022.103217

Pindyck, R.S. (1991). Irreversibility, uncertainty, and investment. In R.S. Pindyck & D.L. Rubinfeld (Eds.), Microeconomics (3rd ed., pp. 323-343). Prentice Hall. https://doi.org/10.3386/w3307

Ratti, R. A., & Vespignani, J. L. (2016). Oil prices and global factor macroeconomic variables. Energy Economics, 59, 198-212. https://doi.org/10.1016/j.eneco.2016.06.002

Salisu, A. A., & Gupta, R. (2021). Oil price shocks and economic policy uncertainty in emerging economies. Energy Economics, 94, 105085. https://doi.org/10.1016/j.eneco.2020.105085

Salisu, A. A., & Gupta, R. (2021b). Oil price shocks and stock market volatility: A review of the literature. International Review of Financial Analysis, 78, 102924. https://doi.org/10.1016/j.irfa.2021.102924

Salisu, A. A., & Gupta, R. (2021c). Oil shocks and stock market volatility of the BRICS: A GARCH-MIDAS approach. Global Finance Journal, 48. https://doi.org/10.1016/j.gfj.2020.100546

Salisu, A. A., Adediran, I. A., & Alimi, R. Y. (2022). Modelling oil price volatility and stock market returns in emerging economies: A GARCH-MIDAS approach. Journal of Economic Studies, 49(4), 731-745. https://doi.org/10.1108/jEs-04-2021-0205

Salisu, A. A., Cuñado, J., & Gupta, R. (2022). Geopolitical risks and historical exchange rate volatility of the BRICS. International Review of Economics & Finance, 77, 179-190. https://doi.org/10.1016/j.iref.2021.09.017

Tumala, M. M., Salisu, A. A., & Gambo, A. I. (2023). Disentangled oil shocks and stock market volatility in Nigeria and South Africa: A GARCH-MIDAS approach. Economic Analysis and Policy, 78, 707-717. https://doi.org/10.1016/j.eap.2023.04.009

Wang, Y., & Li, X. (2023). The impact of economic policy uncertainty on the volatility of stock prices in G7 countries. Journal of International Financial Markets, Institutions and Money. https://doi.org/10.2147/RMHP.S407481

World Bank. (2023). Oil shocks: Causes, effects, and mitigation strategies. World Bank. https://openknowledge.worldbank.org/handle/10986/39886

Yu, J., Shi, X., Guo, D., & Yang, L. (2021). Economic policy uncertainty (EPU) and firm carbon emissions: Evidence using a China provincial EPU index. Energy Economics, 94, 105071. https://doi.org/10.1016/j.eneco.2020.105071

Yu, J., Zhang, Y., & Wang, S. (2023). The impact of political uncertainty on the volatility of stock prices in China. Emerging Markets Finance & Trade, 59(1), 107-120. https://doi.org/10.1080/1540496X.2022.2038753

Yu, X., Song, M., & Wang, J. (2021). The impact of economic and political uncertainty on stock market volatility in China. Economic Modelling, 570, 125794. https://doi.org/10.1016/j.physa.2021.125794

![]()